Chief Global Strategist

Last week, as a frothy stock market continued to zigzag across a high plateau, two events occurred with significant implications for the macroeconomic outlook. First, the President signed a Memorandum of Understanding with Iran, potentially bringing the Iran war to a close. Second, Kevin Warsh presided over his first meeting as Fed Chairman, resulting in a slightly more hawkish tilt to monetary policy in the short run and the promise of significant reform in the long run.

In the rush of market-moving news that has characterized 2026 so far, it is worth pausing to assess the implications of both of these events.

The Memorandum of Understanding

On Sunday, June 14th, both the U.S. President and the Pakistani Prime Minister announced that a Memorandum of Understanding (MOU) had been agreed to by the United States and Iran. Some of the contents of the agreement were leaked in subsequent days and the full details1 of the memorandum were released to the press on Wednesday, June 17th. In the 14-point document, and in simple language, the U.S. and Iran agreed to:

- The immediate termination of military operations on all fronts, including Lebanon.

- A respect for each other’s sovereignty and a promise not to interfere in the other’s internal affairs.

- A plan to negotiate a final deal within 60 days.

- An end to the U.S. blockade of Iranian ports and the removal of U.S. forces from proximity to Iran within 30 days of a final deal.

- The restoration of safe passage for commercial vessels with no charge through the Strait of Hormuz for 60 days with subsequent rules being negotiated between Iran and Oman.

- The U.S. and regional partners developing a plan with at least $300 billion for Iranian reconstruction and development.

- The U.S. dropping all sanctions against Iran on a schedule agreed upon as part of the final deal.

- A reaffirmation by Iran that it would not procure or develop nuclear weapons and an agreement that the U.S. and Iran would resolve the disposition of stockpiled enriched material in a mechanism tied to the removal of sanctions, with both parties discussing Iran’s other nuclear needs going forward.

- The status quo being maintained on both the nuclear issue and regional forces, pending a final deal.

- The U.S. Treasury immediately issuing waivers of financial restrictions on Iran’s exports of crude oil, petroleum and derivatives.

- The U.S. unfreezing Iranian assets upon the implementation of the MOU.

- The establishment of mechanisms to monitor compliance with the terms of the MOU and the final deal.

- The commencement of negotiations on a final deal once all military operations have been terminated, the blockade has been ended, the Strait has been reopened, oil export restrictions have been removed and assets have been unfrozen.

- The endorsement of the final plan by the UN Security Council.

While others will opine on the long-term geopolitical implications of this deal, there are a narrower set of points that are relevant for investors.

First, the MOU effectively separates the reopening of the Strait of Hormuz from achieving a final agreement on reining in Iran’s nuclear ambitions. This should allow oil and other important products to leave the Persian Gulf in the weeks and months ahead. In addition, the removal of impediments to Iran producing and exporting oil should bolster global oil supplies in the months ahead and this, combined with a continued drawdown of strategic petroleum reserves in the United States and elsewhere, could well result in a normalization of global oil and product prices before a normalization of supply chains themselves.

Second, over the weekend, Iran announced that it had reclosed the Strait because of continued Israeli actions in Lebanon. However, further talks in Switzerland suggested that, if this is the case, the closure should be short-lived. Our base case is that both Iran and the United States find a way to reopen the Strait and keep it open with the U.S. putting additional pressure on Israel to cease hostilities in Lebanon.

Third, this is, at first reading, an uneven agreement in addressing the causes of the war in the first place. There has been no change in Iran’s oppressive regime, except in the youth of its leaders. There are no limitations on Iran’s ability to rebuild its conventional military capabilities or support regional proxies and Iran will presumably pursue both of these goals, given the unfreezing of assets, a promised fund for reconstruction and the removal of sanctions on its energy industry. Moreover, while Iran will, no doubt, agree to limit its ambitions to develop nuclear weapons, (or rather, as in the MOU, deny that it ever had such ambitions), the U.S./Israeli attack may well convince the regime that its long-run security would be enhanced by having nuclear capabilities, and that the U.S. will be less interested in preventing Iran from acquiring them going forward, given its experience in the recent conflict.

An uneven peace is a dangerous thing. It is somewhat ironic that the President signed the Memorandum of Understanding last week while in Versailles. The Treaty of Versailles, signed 107 years ago this week, officially ended the Great War, as it was known then. However, it was a notoriously uneven agreement, inflicting so much pain on Germany as to hobble the German economy and ultimately lead to the rise of Nazism in Germany and World War II. Investors should recognize the risk that, unless subsequent negotiations impose far greater constraints on the Iranian regime, we may sadly, some day, look back on the conflict of the last few months as Iran War I, with Iran War II inflicting further human misery and economic disruption.

Messages from the FOMC meeting

The second major event of last week, overshadowed by Middle East negotiations, was Kevin Warsh’s first FOMC meeting as Fed Chairman. For investors, there were three key messages from the meeting:

- Warsh intends to work closely with his colleagues at the Fed and is as committed as his predecessors to maintaining Fed independence.

- The committee is now slightly more hawkish than it was at its last few meetings under Chair Powell, and,

- Warsh hopes to reform many aspects of the Fed’s monetary policy, analysis and communications but he is committed to doing so in a thoughtful and deliberate way having consulted with experts and with the cooperation of his colleagues.

The first point was made clear from the opening line of the now shorter FOMC statement which noted that the statement was approved by a 12-0 vote. The unity of the committee at the start of Chairman Warsh’s tenure was an important signal, as was the fact that, despite the administration’s hope that Warsh would be more dovish than his predecessor, he didn’t vote for immediate rate cuts or even give the slightest indication that he had considered doing so.

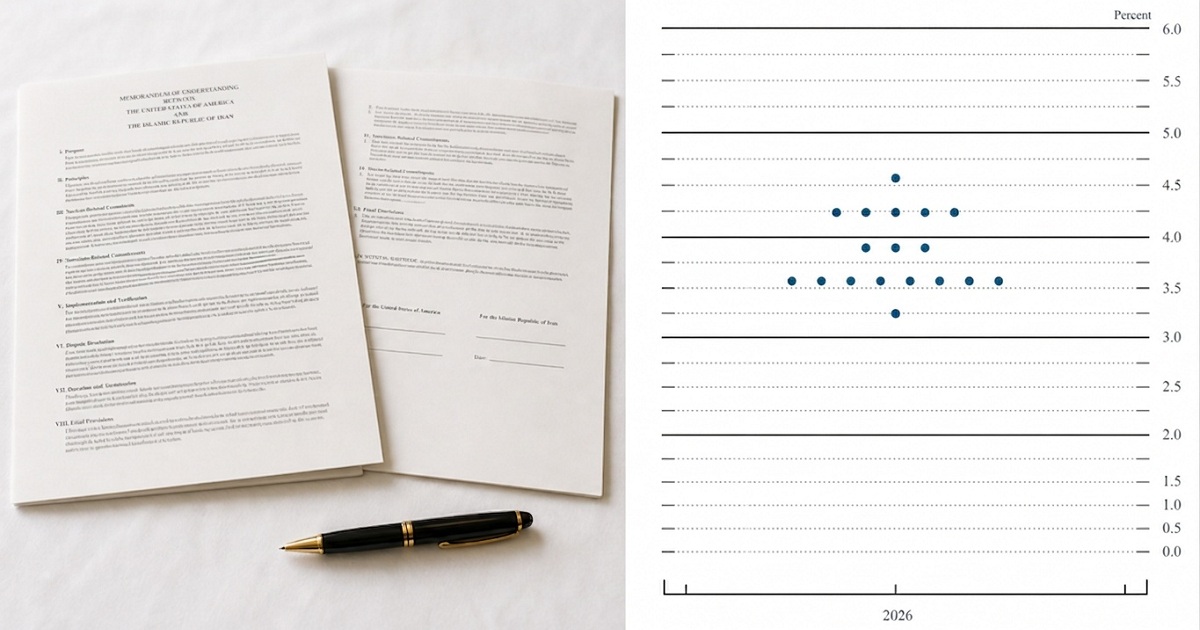

Second, the dot plot was more hawkish than that published in March, with the median projection now including one rate hike by the end of 2026 compared to the projected cut from the March meeting. As of this morning, partly in response to the FOMC meeting communications, the fed funds futures market is pricing in a 100% chance of a rate hike by October and a 72% shot of a second rate hike by the end of this year.

It should be noted that futures markets are now more hawkish than the Fed’s own projections. While Warsh himself did not provide economic or interest rate projections, the other 18 of the 19 FOMC participants did. Of those 18, 9 projected that the fed funds rate would be at its current level or lower by the end of this year and 9 projected that it would be higher. The median dot now shows an increase because only one participant projected a cut while those proposing increases ranged from one to three increases.

However, it is important to remember that rate decisions are made, not by the 19 members of the FOMC committee but by the 12 current voting members, comprised of the 7 members of the Board of Governors and 5 of the 12 Federal Reserve Bank presidents. We estimate that, of the 11 voting members submitting projections, 8 forecast no change or a cut while 3 forecast a hike. In other words, if the dot plot had been of those who actually get to make the decision this year, it would have forecast no change in the federal funds rate for 2026.

All of this, of course, rests on the knife edge of trends in growth, unemployment and inflation over the rest of the year. However, with energy prices now falling, rents barely rising, lower tariffs and weak wage gains, it still looks like May was the peak in the latest bout of inflation and falling inflation for the rest of the year could be just enough to keep the Fed on hold.

Finally, Chairman Warsh announced the formation of five task forces to examine:

- Fed communications

- The Fed balance sheet

- The use of and reliance on existing data sources

- Productivity and jobs in an era of transformation, and,

- Inflation frameworks.

He noted that he was in the process of recruiting experts for each of these task forces and was hoping that they could begin work in the next few weeks and complete it by the end of the year.

All of these are very important and complicated issues and the new chairman himself appears to hold opinions on them that are at variance with many officials at the Fed as well as outside economists. However, while task forces have a certain whiff of bureaucracy about them, in this case, it seems very wise to enlist experts to report on these issues and then thoroughly discuss them before making changes. The first rule of monetary policy, as with medicine, should be to do no evil and this approach reduces the risk of a monetary policy mistake. And from my own perspective, it will give me five instant topics for these notes for weeks to come when, unlike last week, market-moving events provide little to discuss.