Chief Global Strategist

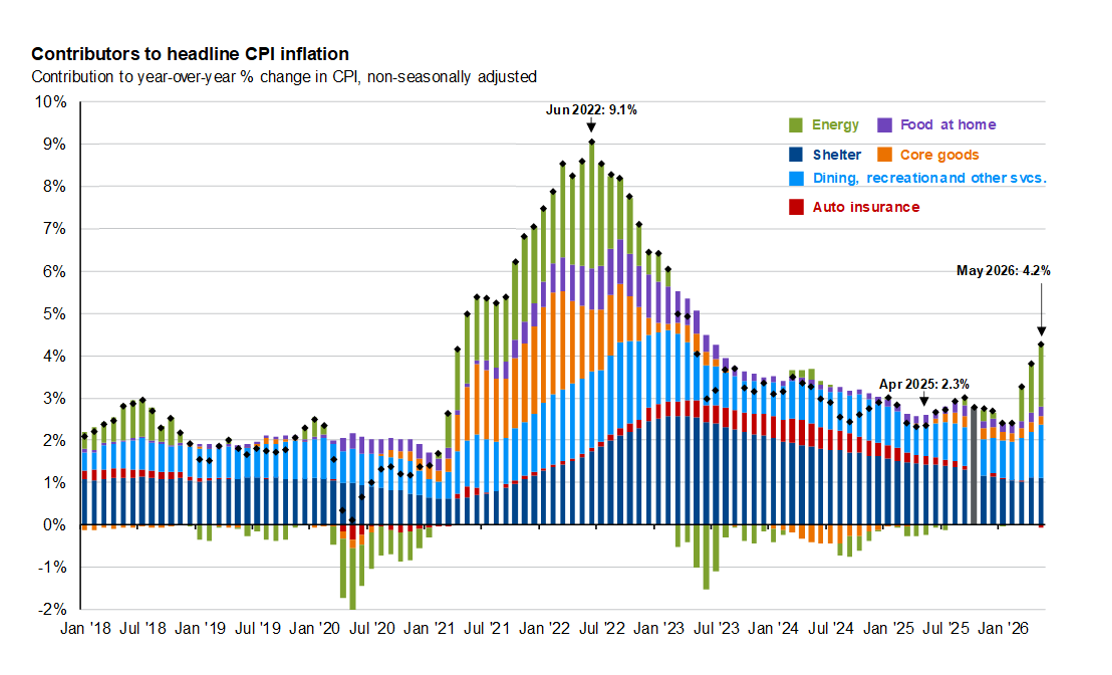

Last Wednesday’s CPI report, while not a surprise, still showed a year-over-year inflation rate of 4.2% - higher than in any month since April, 2023. For investors, this raises a number of questions. First, is this the peak for U.S. inflation and, if it is, how fast will inflation fall from here? Second, are we looking at the right inflation rate, anyway, given differences between CPI and PCE deflators, headline and core measures and the new Fed Chairman’s preference for trimmed mean and median readings? Finally, what does the inflation outlook imply for this week’s Fed decision and the direction of monetary policy and interest rates?

May CPI: Back Above 4% but not for long

Consumer prices rose by 0.47% in May, resulting in a year-over-year increase of 4.17%. Most of this gain, (0.28% to be exact), was due to a 7.0% jump in gasoline prices. However, the inflation story was more mixed elsewhere, boosted by gains in electricity prices, tobacco prices and airline fares, but restrained by reported declines in the prices of new vehicles, medical commodities and auto and health insurance.

All of that being said, it’s possible that May was the high water mark for the current inflation surge.

First, taking a look at June, the average price of a gallon of regular gasoline peaked at $4.56 on May 21st and has fallen back to $4.07 since. Even if it rose by a penny a day for the rest of the month, the June average would be $4.17, down 7.2% from May and taking 0.26% out of month-to-month CPI inflation. Since monthly inflation in June 2025 was 0.25%, year-over-year CPI inflation will fall between May and June unless all other prices rise by more than 0.52% for the month, which is well above the current trend inflation rate.

Thereafter, inflation could drift down further – under some key assumptions.

The most important of these is that the interim peace deal announced by the United States and Iran on Sunday results in a resumption of a free flow of traffic through the Strait of Hormuz. Difficulties remain, including still-to-be-conducted negotiations on Iran’s nuclear capabilities and the willingness of Israel and Hezbollah to refrain from hostilities in Lebanon. However, both the United States and Iran have strong reasons to try to reopen the Strait and keep it open. On the U.S. side, the free flow of oil and other key exports from the region will should reduce inflation ahead of the mid-term elections. The Iranian regime also clearly has an incentive to sustain a solution that allows it to export oil more freely and eliminates the risk of U.S. attacks. Of course, even when the Strait is reopened, it will take some time to restore normality to global energy supplies. However, a continued rapid release of oil from the U.S. strategic petroleum reserve, combined with similar actions overseas, could result in a normalization of gasoline prices that proceeds more quickly than any normalization in energy supply chains.

A second assumption is a continued gradual decline in tariffs. Average gross tariff revenue in the fourth quarter of 2025 equaled 11.5% of goods imports. However, in the aftermath of the February Supreme Court ruling against the IEEPA tariffs, we estimate that this average tariff rate has fallen to just 7.8% over the past three months.

The administration initially tried to replace some of the IEEPA tariff revenue with temporary 10% tariffs under Section 122 of the Trade Act of 1974. This was also ruled to be illegal in a May 7th ruling by the Court of International Trade, although the government is still collecting revenue from these tariffs, pending appeal. As a more permanent solution, the administration has now invoked Section 301 of the Trade Act of 1974 to propose tariffs of 10% on six countries and 12.5% on 54 more, based on alleged unfair trade practices due to “forced labor”. These new tariffs, which exclude goods covered under the USMCA, will also likely be challenged in court.

It may be that the administration finally finds some tariffs that the President can impose unilaterally or that Congress actually approves. However, given both legal challenges and the general unpopularity of tariffs, we assume that the average tariff rate in the fourth quarter of this year and going into next year, will be 7.5% of imports, far below the 11.5% of imports seen in the fourth quarter of last year, reducing pressure on consumer inflation. The eagerness of importers to pass these tariffs onto consumers may also be somewhat mitigated by now substantial refunds of IEEPA tariff revenue.

A third assumption is that shelter costs continue to back off. The CPI measures of rent and owners’ equivalent rent, which together comprise 33.5% of the index, were distorted by the government shutdown last October. However, by May, these distortions had worked their way through the system, giving a clean reading for these measures and showing 2.9% and 3.3% year-over-year growth in rent and owners’ equivalent rent, respectively.

These readings were down from 3.8% and 4.2%, respectively, a year earlier. However, they both still overstate current reality in the housing market. The latest available data from Zillow, CoStar, Apartment List and Realtor.com show year-over-year rent changes on new leases ranging between -1.7% and +1.8%. According to the Census Bureau, the rental vacancy rate in the first quarter was 7.3% - its highest level since 2017, as a falling working age population dampens demand by more than a pullback in multi-family unit construction over the past two years has limited supply. This should result in a slow and steady decline in shelter inflation into 2027.

Finally, there is just no evidence that higher inflation is feeding through to higher wages. Despite a relatively tight labor market and a surge in inflation, average hourly earnings for all workers rose just 3.45% in May, their second smallest gain in five years, resulting in a year-over-year decline in real wage rates for a second consecutive month. Fewer than 6% of U.S. private sector workers are members of a union, there are very few strikes demanding higher pay and workers appear either to be unwilling to demand or unable to achieve significant real wage gains, even in the face of rising productivity.

This last factor is really key to a lack of “stickiness” in U.S. inflation and our baseline forecast is that CPI inflation drifts down to 3.3% year-over-year by December and then tumbles to 1.8% year-over-year by next May (reflecting last month’s very high reading). Thereafter, for the rest of 2027, it stabilizes at roughly 2.0% year-over-year.

Which Inflation Measure?

With CPI inflation running at 4.2% and projected to remain above 3% through the end of the year, it’s hard to argue that inflation is even close to the Fed’s target. However, there is some question about which inflation measure to focus on, particularly given Chairman Warsh’s preference for “trimmed” averages which he alluded to in his April 21st confirmation hearing.

So, at the risk of being a bit pedantic, here is the situation.

The best known inflation measure is the consumer price index. However, the Federal Reserve, in its annual statement on longer-run goals and monetary policy strategy, explicitly sets a target of 2.0% for the personal consumption deflator. The consumption deflator, unlike the consumer price index, is a chain-weighted index that takes into account quantity changes over time in consumers’ consumption of goods and services. As such, it is, at least theoretically, a better measure of inflation from the perspective of consumer welfare.

While the Fed’s official target is the headline consumption deflator, many economists both inside and outside the Fed, prefer to focus on the core consumption deflator, which excludes price changes in the food and energy categories. The argument is that food and energy prices are unusually volatile and therefore, if you want to get a sense of where inflation is headed, you are better off looking at the core consumption deflator.

In his April 21st testimony, Chairman Warsh took this a step further, arguing that trimmed mean measures can do a better job at deducing the underlying inflation trend by ignoring the biggest price increases either up or down, regardless of whether they are part of the food and energy categories. He also asserted that, looking at these measures, inflation has improved somewhat over the past year.

He has a point, but not one that justifies a cut in interest rates anytime soon.

First, May year-over-year-inflation (including our forecasts for yet-to-be-released numbers) was:

4.2% as measured by headline CPI,

4.0% as measured by the headline consumption deflator,

3.3% as measured by the core consumption deflator, and,

2.4% as measured by the Dallas Fed trimmed mean consumption deflator.

All of these numbers are above the Fed’s 2% target. Moreover, the Dallas Fed measure is likely the most stable of the four and may not fall below 2% even in 2027.

Second, if an inflation index is being used to assess the impact of increases in the cost of living on ordinary households then the Fed should focus on headline, rather than core, inflation. The average family cannot exclude food and energy from their budget. Conversely, if the reason for looking at core measures or trimmed measures is to forecast future inflation, it makes more sense to apply deeper analysis, looking at current inflation trends but also considering the impact of policies elsewhere in Washington including tariffs, global supply chains and any potential future fiscal stimulus.

Finally, even if inflation was headed quickly below 2%, the Fed should not ignore broader economic and financial conditions. There is no evidence that the economy is on the brink of recession. Consumer spending growth appears steady, AI-related capital spending is booming and labor market indicators, such as job openings and unemployment claims look relatively strong.

However, turning to financial conditions, the U.S. equity market is currently on track to achieve strong gains for a fourth consecutive year, fueling consumer and investment spending but also increasing the risk of financial bubbles. It is not at all clear that a cut in interest rates at this time would boost real economic growth. It would, however, provide further cheap funding for speculation across financial markets which would increase the danger of a bubble bursting in the next few years, potentially doing considerable damage to both the economy and financial markets.

Implications for Monetary Policy and Interest Rates

This Wednesday, Chairman Warsh and his colleagues at the Federal Reserve will publish new economic projections as part of their post-FOMC communications. We expect them to modestly increase their estimates of economic growth and inflation for both this year and next and to project a slightly lower unemployment rate. This being the case, we also believe they will remove their expectation of any rate cut for 2026.

The new Fed chair, despite relatively dovish comments in his confirmation hearings, will very likely go along with the majority in this decision. No Fed chair has ever publicly voted against the majority of the FOMC and, since a crucial part of Chairman Warsh’s job will to be form a consensus on the committee, it would be very odd if he started his tenure by voting against the majority view.

He will, however, likely argue strongly against the rate hike that futures markets have priced in for later this year and, in this debate, he is likely to prevail. While neither the economy nor financial markets need a rate cut at this time, we expect both growth and inflation to slow entering 2027 and, so long as they are trending down, there will be little reason for the Fed to try to micromanage the pace of their decline. While the Fed Chair may have to abandon his short-term aspirations for easier monetary policy, he may well have more success in convincing his colleagues to be less active in general in an environment where it’s not clear that Fed activism would do any long-term good.

For investors, this likely means that the direction of long-term interest rates will be dictated by fiscal policy more than monetary policy in the years ahead. This should imply a slow drift up in long rates due to accumulating government debt – not giving investors a reason to abandon bonds but rather to recognize that, over the next few years, high-quality fixed income should be owned for income and diversification rather than capital gains.