Chief Global Strategist

In the pantheon of running injuries, there is a well-established hierarchy. A recreational runner, finishing any marathon, or exerting themselves at half that distance, can expect to come down with delayed onset muscle soreness, otherwise known as DOMS. Starting from barely a twinge at the finish line, the pain rises in intensity over the next few days, with your quads telling you firmly that your running days are over. But then it fades and a week later you should be running like a spring lamb again.

At the other extreme, a ruptured Achilles tendon can require surgery and it will be, at a minimum, many months before you can contemplate donning your running shoes again. And there is simply no point in trying to rush it – returning to the roads too early can easily re-injure it, setting back recovery.

Problems in asset valuations heal over a similarly wide range of time scales. A problem with stock market valuations can be fixed quickly – as we saw most dramatically on October 19th, 1987 when the S&P500 dropped over 20% in one day. However, a problem of over-priced housing takes much longer to fix – and trying to rush a cure can often cause further problems.

The Affordability Crisis

Over-priced housing, otherwise known as the housing affordability crisis, emerged in two strands in the wake of the pandemic.

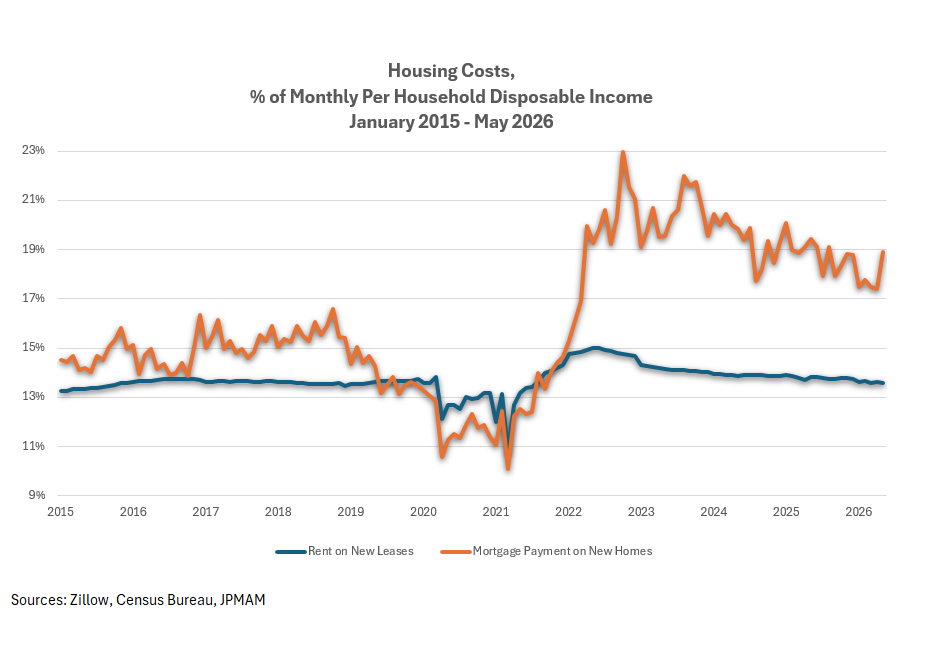

For those buying a home, prices grew at a moderate pace in the second half of the last decade and then fell as the pandemic took hold. Thereafter, however, prices soared as prospective home-buyers with stimulus cash tried to buy while mortgage rates remained low. Between January 2015 and January 2020, the price of a new single-family home rose at a modest 2.0% annual rate, from $348,000 to $384,000. Between January 2020 and April 2022, it surged by a further $154,000, or at a more than 16% annual rate, to reach a level of $538,000. Meanwhile, the Federal Reserve was raising interest rates to combat inflation and the average rate on a 30-year fixed-rate mortgage climbed from 3.67% in January 2015 to 7.65% by October 2023. As a result, the monthly mortgage payment on the average new home more than doubled over the same period, jumping from $1,278 to $2,832, or from 14.5% of average per household disposable income to 21.7%.

Apartment rents also saw a sharp increase, although the timing was a little different. Rents were relatively subdued in the latter half of the last decade and then briefly collapsed as the pandemic caused many renters to move, temporarily, back to their family homes. However, as younger people moved back out into the world, flush with stimulus cash but boxed out of the home purchase market by higher prices, landlords took advantage of the situation to boost rents. According to Zillow, the average rent on all housing units available for rent1 jumped from $1,165 in January 2015 to $1,753 by June 2022, or from 13.2% of average per household disposable income to 15.0%.

Some Healing in Affordability

By 2023, at least in terms of affordability, the U.S. housing market was broken, with many families, particularly younger and poorer families, seeing their dreams of homeownership fade and paying a very high share of their income in rent.

Moreover, it was always going to take a long time for housing to heal. Home sellers are reluctant to cut prices, in many cases because they need the home equity to buy their next place. This issue was compounded by the fact that many existing homes were purchased with super-low-rate mortgages, meaning that a seller would also face sticker shock when taking out a mortgage on their next purchase. Consequently, many homes that might have been sold were kept off the market.

On the rental side, it also takes some time for a mismatch between demand and supply to resolve itself. A landlord in the middle of a lease doesn’t have to adjust the rent downwards and, even when new leases are signed, there is a reluctance to lease out property at less than the old rent.

Despite these forces, however, affordability has improved somewhat in recent years, both with respect to buying and with respect to renting.

Since April 2022, average new home prices have barely increased, edging up from $538,000 in April 2022 to just $541,000 in May of 2026. Mortgage rates have also fallen since late 2023 and this, combined with continuing gains in personal income, means that average mortgage payments have fallen back from 21.7% of per capita disposable income in October 2023 to 18.9% in May of this year.

Rents have also grown more slowly, seeing average annualized growth of 3.0% since June 2022 and just 1.9% growth over the past 12 months, according to Zillow. The average rent in May of this year was $1,951, or 13.6% of per household disposable income – nearly as low as at the start of 2015 and slightly below the 13.7% average since then.

So why the improvement?

One part of the answer, at least with respect to the purchase market, has been Fed easing. After hiking the federal funds rate from a range of 0-0.25% in March of 2022 to 5.25%-5.50% fifteen months later, the Fed went on hold and then, over the course of 2024 and 2025, cut the funds rate to its current range of 3.50%-3.75%. This has facilitated a modest reduction in 30-year fixed rate mortgage rates, which currently stand at just below 6.5%.

A second reason is just the passage of time in a growing economy. Even if home prices and rents don’t adjust down, incomes should eventually adjust up. Between May 2023 and May 2026, per household disposable income rose by 12.5%, helping ease the affordability issue. For upper-income families, this has been supplemented by stock market gains, increasing general wealth and money for downpayments.

Increased supply can also help. While neither home prices nor rents have grown much in the past three years, their high levels from a few years ago kept supply rolling onto the market. Between June 2023 and May 2026, U.S. home builders completed almost 3 million new single-family units and over 1.5 million new multi-family units. According to the quarterly homeownership survey conducted by the Census Bureau, between the first quarter of 2023 and the first quarter of 2026, the number of housing units in the United States rose by an average of 1.6 million units, or 1.1%, per year.

This last number is worth pondering in the context of current trends in U.S. demographics. Census estimates and projections suggest that the total U.S. population rose by 1.0% in the year ended in June 2024, 0.5% in the year ended in June 2025 and just 0.2% in the year that will end this week. This sharp downturn in population growth is, of course, a reflection of a dramatic reversal of immigration trends. Moreover, if the current pace of net immigration is maintained in the years ahead, U.S. population growth will likely stay at 0.2% per year.

The Road Ahead

At this rate of population growth, both rental vacancies and unsold new homes are likely to rise. Already, in the first quarter of 2026, the rental vacancy rate rose to 7.3% - its highest level since the third quarter of 2017. Meanwhile, inventories of unsold new homes have continued to rise in recent months, even as sales have stagnated, pushing the ratio of unsold new homes to sales to 10.3 months in May – its second highest monthly reading since 2009.

This probably explains why, in the June edition of the monthly National Association of Homebuilders survey, homebuilders rated the traffic of potential homebuyers as worse than it had been over 80% of the time since 1985. But still they are building, with building permits for May indicating a roughly 1.4 million annualized pace of overall housing starts in the months ahead.

Indeed, on the road back to more normal affordability, it is the juxtaposition of continued building with very weak population growth that should ensure a continued stagnation in home prices and rents.

This has important macro-economic implications.

First, a third of the consumer price index is comprised of shelter costs which follow the rental market with a long and smoothed lag. In May, these shelter costs showed a 3.3% year-over-year growth rate, well down from 3.9% a year earlier but still much higher than implied by inflation in new leases. Further declines in shelter costs should do significant work in reducing measured inflation in the year ahead.

The weakness in home sales should also contribute to a gentle slide in home building. While residential construction accounts for less than 4.0% of GDP, it is one of the more volatile components of the economy and its weakness should reduce the risk of broader overheating.

Lower inflation and economic growth, both emanating from a mismatch between housing supply and demographic demand, could, along with other factors, dissuade the Federal Reserve from raising interest rates in 2026, despite current futures’ market pricing.

Finally, there is the political issue of what to do about affordability. Last week, the President refused to sign a bipartisan housing affordability bill in a dispute with Senate Republican leadership. However, we still think it is likely to become law in the next few weeks. The administration will also, undoubtedly, put further pressure on the Federal Reserve to cut interest rates to make mortgages more affordable.

However, mortgage rates are not unusually high relative to history – they merely seem that way because they were extraordinarily low in the fifteen years between the Great Financial Crisis and the post-pandemic inflation. Moreover, it was that long period of low rates that caused the housing affordability problem in the first place by facilitating a surge in prices to levels that would be unaffordable at a time of normal mortgage rates. In a similar vein, the stimulus checks in the wake of the pandemic left many renters with just enough extra cash to encourage landlords to jack up rents to levels that were hard to bear when the stimulus cash ran out.

The truth is that the problems that we have seen in housing affordability in recent years have actually been the result of previous misguided policies by the Federal Reserve and the federal government in trying to help home-buyers and renters. The last thing the economy needs is more help in a similar vein.

More broadly, the question of affordability has rolled through many sectors of the economy in recent decades, from the costs of prescription drugs, to college tuition, to private health care insurance, to the price of eggs, to the price of gas and, most prominently in the past few years, to the cost of renting and homeownership. But, if the affordability issue is so broad, then it isn’t an affordability issue at all. Rather it is one of steadily rising inequality across both income and wealth. That being the case, the appropriate focus for government policy shouldn’t be on why is housing unaffordable but rather on why so many poor and middle-income American families are falling behind in being able to afford everything.