1. Diversification does not guarantee investment return and does not eliminate the risk of loss.

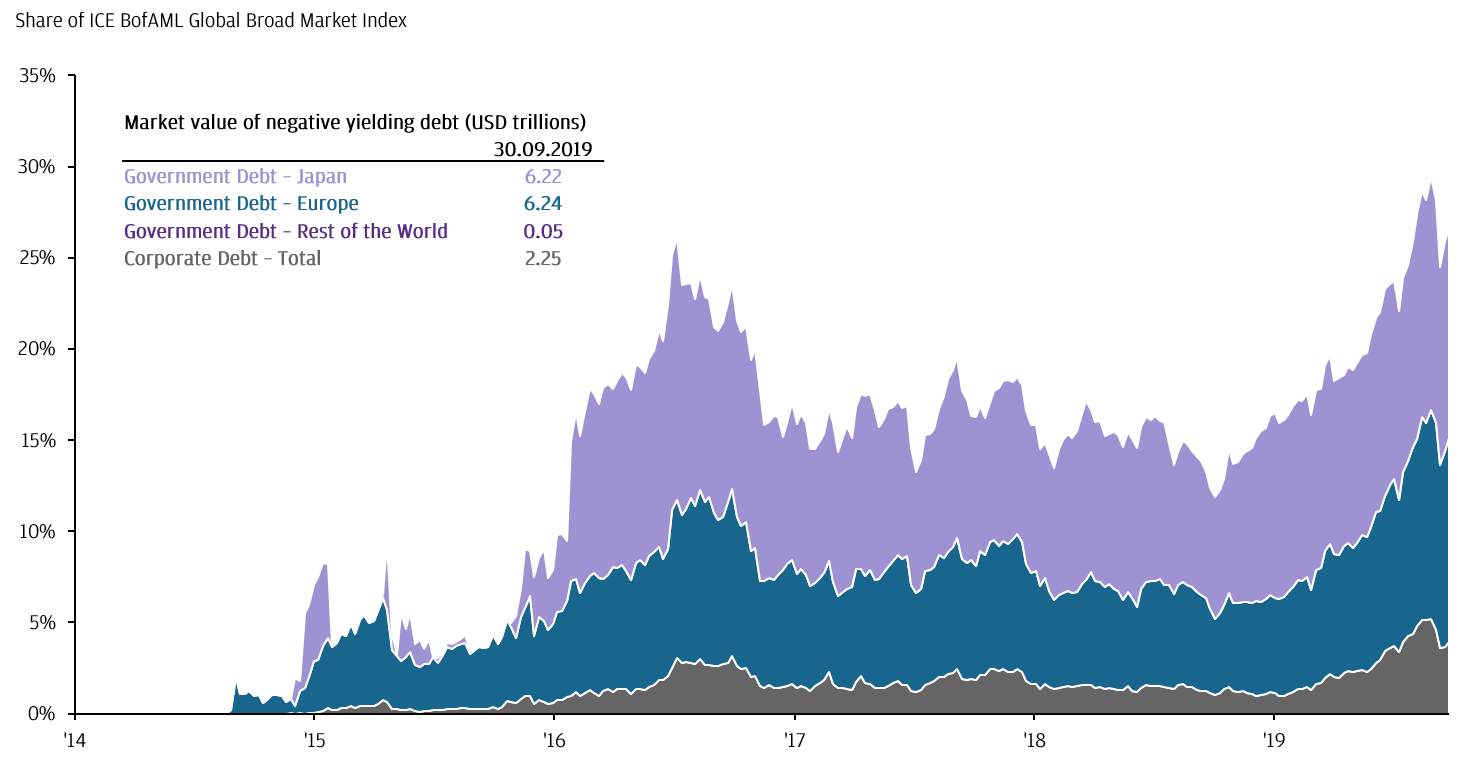

2. Source: Bloomberg, ICE BofA Merrill Lynch, J.P. Morgan Asset Management. Data reflect most recently available as of 30.09.2019.

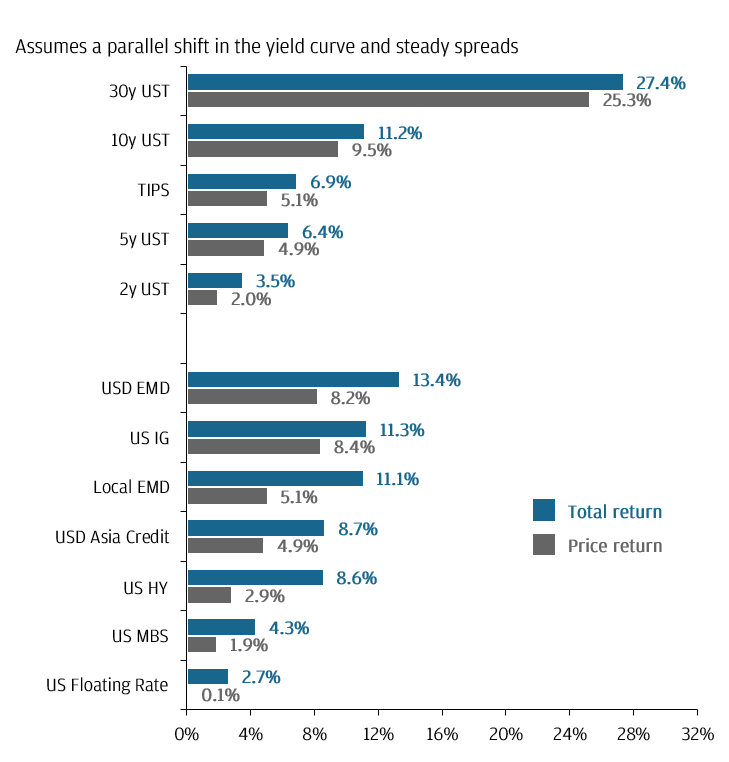

3. Source: Barclays, Bloomberg, FactSet, J.P. Morgan Economic Research, J.P. Morgan Asset Management. Based on Bloomberg Barclays US Treasury Bellwethers Index (2, 5, 10, 30y U.S. Treasuries), Bloomberg Barclays US Treasury Inflation-Protected Notes Index (TIPS), Bloomberg Barclays US Floating Rate Notes Index (US Floating Rate), Bloomberg Barclays US Aggregate Securitized – MBS Index (US MBS), Bloomberg Barclays US Aggregate Credit – Corporate – Investment Grade Index (US IG), Bloomberg Barclays US Aggregate Credit – Corporate – High Yield Index (US High Yield), J.P. Morgan Emerging Market Bond Index Global (EMBIG) (USD EMD), J.P. Morgan Asia Credit Index (USD Asia Credit), J.P. Morgan Government Bond Index – EM Global (GBI-EM) (Local EMD). Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices. Change in bond price is calculated using both duration and convexity, assuming a 1% fall in relevant local interest rate. Past performance is not a reliable indicator of current and future results. Data reflect most recently available as of 30.09.2019.

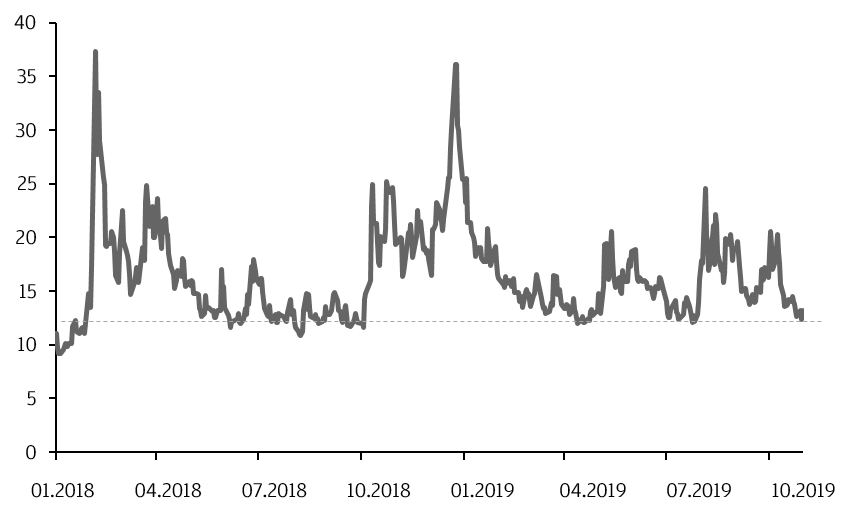

4. Source: FactSet, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Data reflect most recently available as of 31.10.2019.

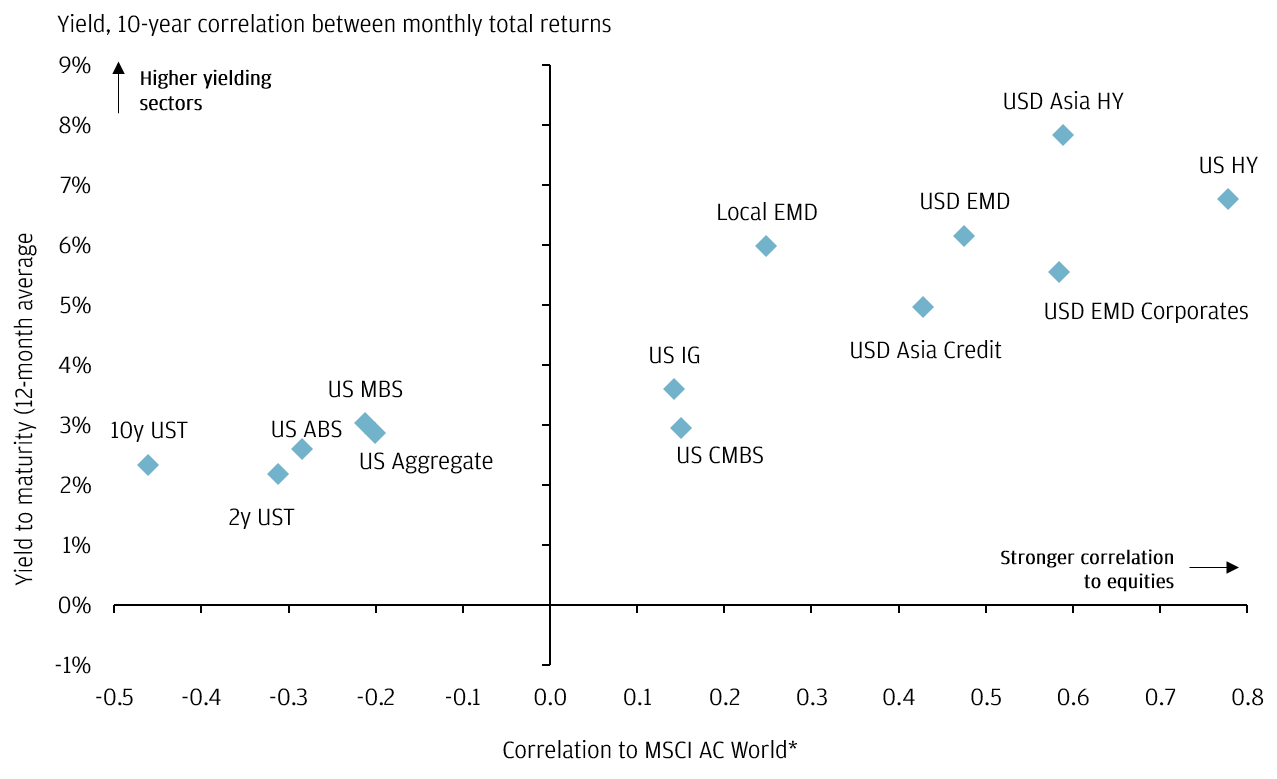

5. Source: Barclays, Bloomberg, FactSet, ICE BofAMerrill Lynch, J.P. Morgan Economics Research, MSCI, J.P. Morgan Asset Management. Based on Bloomberg Barclays US Treasury (UST) Bellwether 2y & 10y (2y & 10y UST), Bloomberg Barclays US Aggregate, Credit – Investment Grade & High Yield (US Aggregate, IG & HY), Bloomberg Barclays US Securitised – Asset-Backed Securities (US ABS), Bloomberg Barclays US Securitised – Mortgage-Backed Securities (US MBS), Bloomberg Barclays US Securitised – CMBS – ERISA-Eligible Index (US CMBS), J.P. Morgan GBI-EM Global (Local EMD), J.P. Morgan EMBI Global (USD EMD), J.P. Morgan Asia Credit (JACI) (USD Asia Credit), J.P. Morgan Asia Credit (JACI) – High Yield (USD Asia HY), J.P. Morgan CEMBI (USD EM Corporates). *Correlations are based on 10-years of monthly returns. Data reflect most recently available as of 31.10.2019. Positive distribution yield does not imply positive return.