Featured

Navigating through the trade policy fog

Discover how shifting tariffs and global supply chain dynamics are shaping U.S. trade policy, market impacts and business strategies in 2026.

What does the current midterm election landscape look like?

How might policy shift after the midterms?

How should investors approach investing in an election year?

How do markets perform in midterm election years?

What configuration of government typically performs best?

Currently, Republicans have a unified government – control of the White House and both chambers of Congress. However, their majority is slim, which means either they maintain narrow control, or cede one or both chambers of Congress to the Democrats.

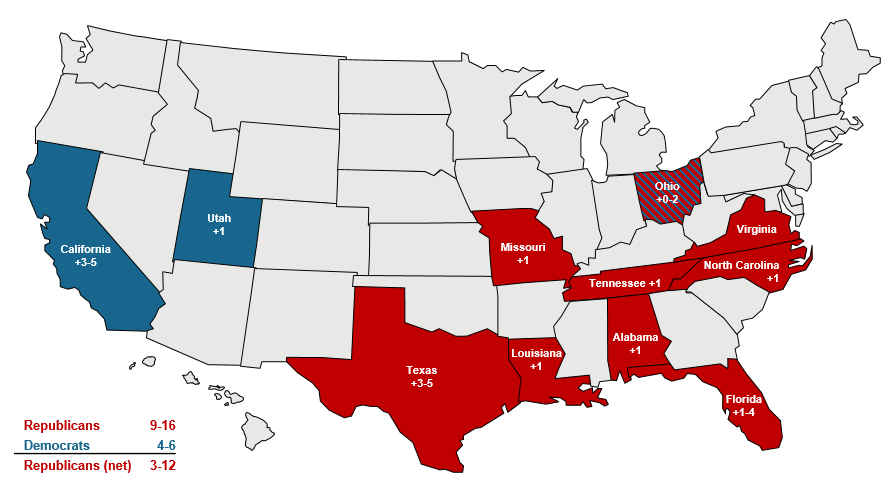

The Senate currently consists of 45 Democrats, 53 Republicans and 2 Independents that caucus with the Democrats. The Democrats would need to gain 4 additional seats to take control of the Senate. While their open seat in Michigan is considered a toss-up, four potential pick-ups would be most likely in North Carolina, Maine, Ohio and Alaska.

The House of Representatives currently consists of 219 Republicans, 212 Democrats and 4 vacant seats (1 formerly held by a Republican in Texas and 3 formerly held by Democrats in California, Florida, and Georgia). The Democrats would need maintain their vacancies and win 3 additional seats to take control of the House. One additional complication is congressional redistricting, which could favor the Republicans in Florida, Texas, North Carolina, Tennessee and Missouri, but favor Democrats in California and Utah. In total, this could net the Republicans 5-10 seats. Still, the Democrats are marginally favored to win the House.

While individual races and candidates are of course key determinants, two other factors are at play. One, midterms are often considered a referendum on the president, and the president’s approval rating has slumped to its lowest of his term thus far. Two, campaign funding has been much stronger for Republicans than Democrats, which can move the needle in select races.

Source: 270towin, J.P. Morgan Asset Management. The Senate currently consists of 45 Democrats, 53 Republicans, and 2 Independents that caucus with the Democrats. *Currently, the House of Representatives consists of 219 Republicans, 212 Democrats, and 4 vacant seats (one formerly held by a Republican in Texas, three formerly held by Democrats in California, Florida, and Georgia). “Current” includes vacant seats. Data are as of July 6, 2026.

The first two years of a president’s term are often a mad dash to check off as many campaign policy promises as possible. That is because often presidents have a unified government (control of Congress) after a general election, but Congressional control can often diminish or flip after the midterms, making it more difficult to achieve agenda items.

Below is an outlook for key policy items under continued Republican control vs. a divided Congress:

Political opinions are best expressed at the polls, not in a portfolio. One cardinal rule for investors: Don’t let how you feel about politics overrule how you think about investing.

The chart below shows a survey from the Pew Research Center asking Americans to rate economic conditions. The results show that Republicans often feel better about the economy under a Republican president, while similarly Democrats feel better about the economy under a Democratic president. Investors often make portfolio decisions based on their economic outlook.

Yet, average annual returns on the S&P 500 during the Obama administration of 16.3% and during the first Trump administration of 16.0% were almost identical and higher than the average return over the last 30 years of 10.3%. It is likely that the macro conditions, like ultra-low interest rates enjoyed during both Obama and Trump administrations, were a more influential driver of above-average returns during those periods, rather than the policy prescriptions each president espoused. Even as macro conditions have shifted, returns during the Biden administration and the second Trump administration have also easily exceeded long-term averages, owing to the strength of American companies, the aggregate health of the consumer and technological innovation.

Investors who did allow their political opinions to overrule their investing discipline may have missed out on above-average returns during political administrations they didn’t like.

Source: Pew Research Center, J.P. Morgan Asset Management. The survey was last conducted in February 2026. Pew Research Center asks the question: “Thinking about the nation’s economy, how would you rate economic conditions in this country today… as excellent, good, only fair, or poor?” S&P 500 returns are average annualized total returns between presidential inauguration dates. Returns for President Trump’s second term are not shown, as the term has not yet completed a full year.

Guide to the Markets – U.S. Data are as of July 6, 2026.

Elections are often a source of anxiety for investors because they introduce a new element of uncertainty to markets, which can result in lower returns and higher volatility. Since 1937, returns in midterm years were 9.2% on average vs. 13.3% in non-midterm years. Realized volatility was also higher.

However, simple averages don’t tell the full story. Midterm years have also coincided with particularly choppy years in the markets that have been entirely unrelated to the elections themselves. For example, 2018 and 2022 were both midterm years in which the stock market suffered negative returns. However, the pressure on the equity market came from the Federal Reserve hiking interest rates. Another notable negative midterm year: 2002, as the market bottomed out due to the tech wreck.

Still, markets may encounter some bumps along the way in midterm years, but those wrinkles tend to be smoothed out very quickly in the run-up to the election and thereafter regardless of the result. In fact, average returns were slightly negative in each of the three quarters preceding a midterm but then jumped an average of 6.6% in the fourth quarter.

If that’s the case, why not reduce equity exposure before the election and ratchet it back up once the polls close? History shows that markets begin to rally just under a month before election day, making timing the market a difficult task, and one that is clearly unrelated to the election result itself.

S&P 500 total return, 1937-2025

Investors always want to know how markets perform under different government configurations. Since 1937, markets returned 16.3% under unified Republican control, but 9.4% under a Republican president with a divided Congress.

While simple to compute, these returns tell investors very little about why markets performed the way they did and how markets are likely to perform in the future. Monetary policy, fiscal policy, economic growth, labor markets, corporate profits and valuations are much better indicators of future returns. Fiscal policy is driven by the government of course, but if we get some form of divided government, policy making has historically been much more constrained.

The economic context, not the political context, tends to be much more relevant to understanding historical market environments and returns.

S&P 500 total return, 1937-2025, (#) = occurrences

Key Policy Slides

Navigating through the trade policy fog

Discover how shifting tariffs and global supply chain dynamics are shaping U.S. trade policy, market impacts and business strategies in 2026.

Latest Insights

The information presented is not intended to be making value judgments on the preferred outcome of any government decision or political election.