One of the benefits of my marathon training is that, most weekends, I get to jog over the Newton and Wellesley hills with my running buddy, John, who happens to be a financial advisor. Over the course of three hours we solve the problems of the world, reviewing them with dour pessimism at the start of our run and assessing them with breezy optimism later on, as the running endorphins kick in.

There is never a shortage of problems to discuss. However, as we started out last Saturday, John had just one question on his mind: “How does it end?”

By which, of course, he was referring to the war with Iran, now entering its third week.

It’s a good question and a much better one than “What happens next?” which would involve a pointless speculation on the next military headline to cross the tape.

“How will it end?” is the key question that the Federal Reserve will have to consider when it meets this week to chart a path for monetary policy. It is also a question for investors, as they consider the potential ramifications of both the conflict and Fed decisions for the economy and markets.

The Stabilization Scenario

It goes without saying that a war, once started, can proceed in unforeseen directions. It’s also obvious, based on many conflicts in the Middle East over the course of recent decades, that military superiority does not guarantee easy victory.

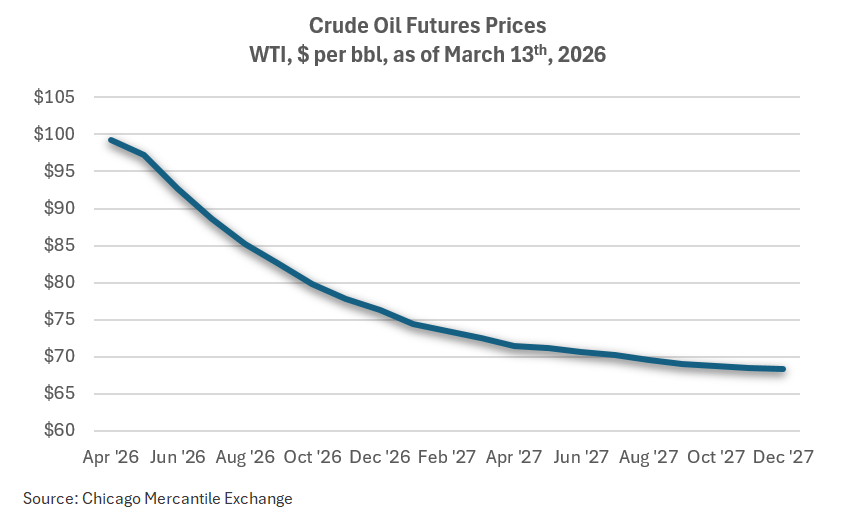

That being said, one reasonable approach to the problem is to consider what the oil futures market is telling us and then try to rationalize this pricing by looking at the pressures on both sides of the conflict. As of the close of trading last Friday, the April WTI futures contract was priced at $99.31 per barrel while the December 2026 contract was priced at just $76.37.

Since countries bordering the Persian Gulf account for over 25% of global oil production and half of the world’s proven reserves, this downwardly sloping futures curve must imply that at least a majority of traders expect some sort of stabilization to unfold in the weeks and months ahead to allow for a resumption of normal oil production and shipping. But how can we get to this stabilization?

One answer comes from considering the motivations and resilience of both sides.

From the perspective of the U.S. administration, the longer the conflict continues, the greater is the military expense, economic damage and political peril. Or, as my colleague, Derek Chollet, head of JPMorgan’s Center for Geopolitics puts it, it comes down to munitions, markets and mid-terms.

Maintaining a large fleet in the Gulf region is expensive, as ships need maintenance and crews need rest. In addition, as has been widely reported, there is a declining number of obvious bombing targets within Iran and a need to replenish stockpiles of offensive weapons. Even more important, the U.S. and Israel are using up their interceptor missiles defending Israel and U.S. military bases in nearby Gulf states. There is an important asymmetry in costs here as interceptor missiles cost millions of dollars to produce while Iranian drones and even ballistic missiles are far cheaper to produce. Nor is it an easy task to eliminate Iranian weapons production in a country that is larger than Iraq and Afghanistan combined.

A second problem for the administration is the economic toll of the war in the United States. Obviously, paying for the war will add to the 2026 budget deficit which is already being swollen by big income tax refunds and the need to refund the now-overturned IEEPA tariffs. However, of more immediate economic importance is the price of gasoline. As of this morning, the average price of regular unleaded gasoline in the United States was $3.72, up from $2.93 a month ago. This will boost inflation in the months ahead, adding to tariff impacts. Moreover, the math of global oil supplies is relatively simple – global demand for oil products is very inelastic in the short run so a prolonged lock-in of Middle East oil would lead to further sharp price increases, slowing the global economy and increasing measured inflation.

This could also have political consequences. So far, the war hasn’t further eroded the President’s popularity. However, if it were to continue indefinitely with increasing costs and diminishing perceived gains, it would likely hurt the Republicans in November. It will be very difficult for Republicans to maintain control of the House of Representatives in any event, since they only have a five seat majority and the party controlling the White House has lost an average of 21 seats over the past 10 mid-term elections. However, if an unpopular war were to drag on, there might even be a threat to the Republicans’ Senate majority.

All of these pressures add to the Administration’s need to wind down its military campaign and get to some form of stabilization.

Assessing how Iran might act has obviously been complicated by the death, at the start of the conflict, of the previous Supreme Leader, Ali Khamenei, along with key military leaders in an Israeli strike. However, President Masoud Pezeshkian, foreign minister, Abbas Araghchi and other key political leaders survived and the Islamic Assembly of Experts has chosen Ali Khamenei’s son, Mojtaba Khamenei, to replace his father.

Importantly, despite the declared hope of the U.S. administration that ordinary Iranians would rise up and overturn the regime there is little sign that they will do so. Indeed, as noted by Iran expert, Vali Nasr on Bloomberg on Friday, the widespread U.S. and Israeli bombing of Iranian cities with civilian casualties and the destruction of heritage sites, is likely increasing anger at the west rather than at the regime.

From the perspective of the Iranian regime, there is little incentive to sue for peace. Peace, with the constant threat of further Israeli and U.S. attacks, would give them no respite. Moreover, they very likely recognize the pressures on the U.S. administration and will probably want to play the long game, calculating that they can hold out longer. It is far more difficult to defend Gulf shipping than to attack it, and with nearly 1,000 miles of coastline between the northern Persian Gulf and the Gulf of Oman, there are almost unlimited opportunities to impact shipping.

That being said, the Iranian leadership would probably like to reach some stable solution eventually. From their perspective, the key preconditions to peace would likely be the cessation of U.S. and Israeli attacks and the right to ship their own oil out of the Gulf unimpeded. This might not be a deal that Israel would want to accept. However, the interests of Israel and the United States are not quite the same in the conflict and eventually the U.S. will want to move on, claiming, of course, that it has now thoroughly defanged Iran.

Fed Communications

While this may represent the most probable endgame to the Iran war, there are obviously big tail risks embedded in unforeseen events in getting there. Moreover, how long it takes to get there could have a big impact on how the conflict affects the economy.

The Federal Reserve will have to consider this when they meet this week. We don’t expect any change in interest rates at this meeting. However, it should be noted that futures markets have become significantly more hawkish since the start of the war, now pricing in just one full rate cut by the end of this year.

Looking at their communications, they will likely emphasize that the conflict in the Middle East has added further uncertainty to the outlook for both inflation and employment. However, their forecasts could look remarkably similar to three months ago.

At that time, they projected that, by the fourth quarter of 2026, the economy would see year-over-year economic growth of 2.3%, year-over-year PCE inflation of 2.4% and an unemployment rate of 4.4%.

Starting with growth, while higher gasoline prices could impede consumer spending, oil prices near $100 per barrel should boost domestic energy infrastructure spending. In addition, there will undoubtedly be supplemental appropriations to restock armaments, adding to aggregate demand. Tariff refunds to corporations along with so-called tariff rebate checks could also boost growth suggesting that, if anything, economic growth in 2026 could be a little stronger than the 2.3% the Fed projected in December.

On the inflation front, the temptation will be to boost their 2.4% projection for fourth-quarter year-over-year inflation. However, services inflation has looked very tame in recent months and, if new tariffs introduced by the administration prove to be lower than the IEEPA tariffs they are replacing, non-energy goods inflation should moderate significantly by the end of the year. Finally, if a stabilization scenario in the Gulf involves freer access to world markets for Iranian and Russian oil, oil prices could fall back very significantly by the end of the year. Of course, such additional access to foreign capital for Russia and Iran could have seriously negative geopolitical consequences. However, in the short run, it would be disinflationary. For this reason, we actually think inflation could be lower by the end of the year than the Fed projected in December, albeit with a significant mid-summer jump.

Finally, on unemployment, FOMC participants will no doubt have seen the very significant decline in year-over-year job growth that is now evident in both the household and establishment surveys. However, given very tight labor supply, stronger economic growth over the summer could result in a lower unemployment rate by the end of the year than the 4.4% seen in February and projected for the fourth quarter by the FOMC.

Most of all, however, in the Fed statement and particularly in Chairman Powell’s press conference, the emphasis will be on uncertainty, with the Fed willing to adjust policy in either direction in response to international developments or emerging trends in U.S. economic data.

Investors, too, should recognize this uncertainty. The stock market generally reacts badly to uncertainty and falling stock prices in recent weeks are hardly surprising. That being said most areas of global equity markets seem reasonably priced. Consequently, the right strategy for investors is probably to focus on “how will it end” rather than “what happens next” and make sure that they are broadly diversified across reasonably-priced assets.