Quality and yield both matter to us

We believe we can tap into relatively attractive income and risk-adjusted return potential by investing flexibly across different sectors in the bond markets. Non-traditional income sources such as securitised debt1 is one of the asset classes in our search for quality and yield opportunities in an overall bond portfolio1.

Agency mortgage-backed securities (MBS) are guaranteed by US government-related bodies, such as Ginnie Mae, Fannie Mae and Freddie Mac, and they are generally AAA-rated. MBS pooled from commercial mortgage loans are called commercial mortgage-backed securities (CMBS).

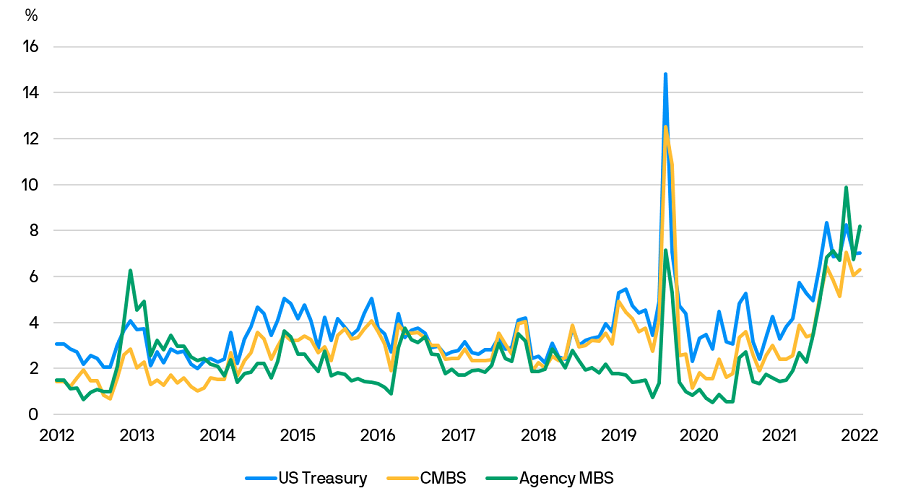

As illustrated below, agency MBS and CMBS have exhibited relatively similar trends of volatility as US Treasuries over the 10-year period between 1 September 2012 and 31 August 2022.

Volatility trends of US Treasuries, agency MBS and CMBS over the past 10 years

Source: Bloomberg, J.P. Morgan Asset Management. Data as at 31.08.2022. MBS refers to mortgage-backed securities, CMBS refers to commercial mortgage-backed securities. Indexes used are: Bloomberg US Treasury Index (US Treasury), Bloomberg US CMBS Index (CMBS), Bloomberg US MBS Index (Agency MBS). The Bloomberg US MBS Index tracks fixed-rate mortgage-backed pass-through securities issued by Ginnie Mae, Fannie Mae and Freddie Mac. Volatility refers to 30-day moving average data covering the period from 01.09.2012 to 31.08.2022. Indices do not include fees or operating expenses and are not available for actual investment. Past performance is not a reliable indicator of current and future results.

Since the beginning of 2022, we see compelling opportunities in these securitised assets. While positioning our overall fixed income portfolio currently, agency MBS and CMBS play a defensive role as they present income opportunities that are relatively higher than US Treasuries. Currently, we prefer higher coupon agency MBS because of the advantage of elevated yields, while also improving the overall quality of our securitised asset allocation. We also favour multi-family CMBS because of supportive long-term demographic trends while short-term leases can also allow these properties to increase rents and cash-flows as inflation stays elevated.

How do we strive for yield and quality opportunities in the JPMorgan Income Fund?

Under current market conditions, we believe that investing flexibly across different bond market sectors is key to enable us to seek diversified income sources and to tap into attractive risk-adjusted return opportunities.

Optimising a market revaluation in the securitised space in the first half of 2022, we added some allocation2 in the sector. We believe the defensive characteristics of agency MBS and improving fundamentals for multi-family CMBS could help build portfolio resilience as the global economy loses momentum. Our allocation in the sector, combined with a bottom-up approach in selecting high-quality corporate bonds, are among the different income sources of the Fund.

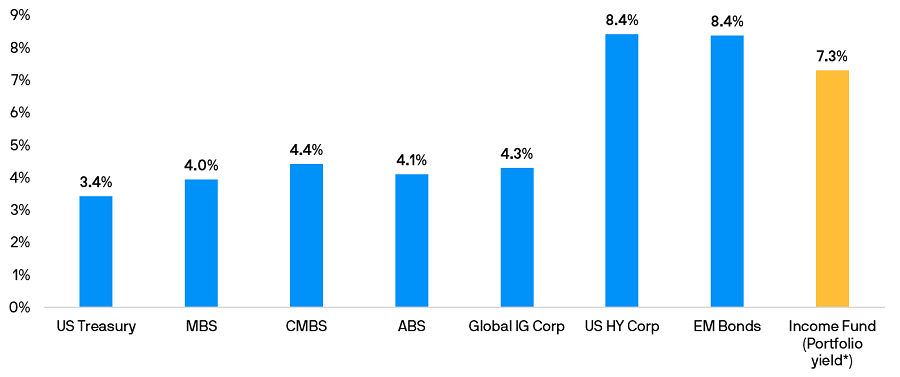

As of end-August, the Fund achieved a higher portfolio yield of 7.3% while maintaining an A- average credit rating3. The annualised distribution yield of the Fund, as of 1 September 2022, stood at 4.59%4.

5. Source: J.P. Morgan Asset Management, as of 01.09.2022. Underlying portfolio yield is an annualised percentage measure of interest and dividend income earned by the portfolio, with the Total Expense Ratio included in the netting of fees and expenses. Sales charges and net realised gain should not be included in the computation. Distribution yield refers to the annualised distribution yield of JPMorgan Income Fund. Annualised yield = [(1+distribution per unit/ex-dividend NAV)^distribution frequency]-1. The annualised dividend yield is calculated based on the latest dividend distribution with dividend reinvested, and may be higher or lower than the actual dividend yield.

Past payout yields and payments do not represent future payout yields and payments. Positive yield does not imply positive return. Dividend is not guaranteed. Distributions may be paid out of capital or distributable income or both. Any payments of distributions by the Fund are expected to result in a decrease in the net asset value per share on the ex-dividend date. Investments involve risks and are not comparable to deposits. The value of the units and the income accruing, if any, may fall or rise. Funds that invest in or where payout may be generated from financial derivatives strategies may involve higher risks. The declaration and payment of dividends is at the discretion of the manager and is subject to the dividend policy referred in the Offering Documents Please refer to the Offering Documents for details on the Fund’s investment strategy including risk factors and the dividend policy. For detailed disclosures please visit www.jpmorganam.com.au.

Yield across individual fixed income sectors and portfolio yield of JPMorgan Income Fund*

Source: Bloomberg, J.P. Morgan Asset Management. Data as at 31.08.2022. MBS refers to mortgage-backed securities, CMBS refers to commercial mortgage-backed securities. ABS refers to asset-backed securities. Global IG Corp refers to global investment-grade corporate bonds, US HY Corp refers to US high-yield corporate bonds, EM refers to emerging market, Income Fund refers to the JPMorgan Funds - Income Fund. Indexes used are: Bloomberg US Treasury Index (US Treasury), Bloomberg US MBS Index (agency MBS), Bloomberg US CMBS Index (CMBS), Bloomberg ABS Index (ABS), Bloomberg Corporate Credit Index (Global IG Corp), Bloomberg US HY Index (US HY Corp), J.P. Morgan EMBI Global Diversified Index (EM Bonds). The Fund seeks to achieve the stated objectives included in the offering documents. There can be no guarantee the objectives will be met. US HY Corp is based on Yield to Worst. US Treasuries, agency MBS, CMBS, ABS, Global IG Corp and EM bonds are based on Yield to Maturity. *Income Fund represents the annualised yield of the underlying portfolio of JPMorgan Income Fund, not the distribution yield. Past performance is not a reliable indicator of current and future results. Yield is not guaranteed. Positive yield does not imply positive return.