The bottom line is that performance in U.S. equity markets so far this year has been all about rates, a theme that should persist as earnings expectations gradually align with reality.

In brief

- 1Q23 U.S. earnings reports have been better than expected

- Profit margins remain key, and companies are defending them

- Capex is coming under pressure, employment should be next

- Focus on quality and cash flow when evaluating investment opportunities

Re-test the lows or a new bull run?

U.S. equity markets have found their footing in 2023, demonstrating an unexpected resilience against fears of recession, failures in the banking sector, elevated inflation, and tighter monetary policy. This has led many investors to wonder if we might be out of the woods and embarking on a new bull run, or whether we will re-test the lows at some point in the coming months; although a skeptical outlook among many investors has allowed us to entertain the idea that a new bull run has started, we continue to view the balance of risks as being tilted to the downside. Futures markets continue to price 75bps of interest rates cuts in the second half of the year – a phenomena we believe will fail to materialize – and earnings estimates are still in the process of re-rating. Once again, this leaves us focused on the outlook for corporate profits, as if rate cuts fail to materialize as expected, there will be limited capacity for multiple expansion.

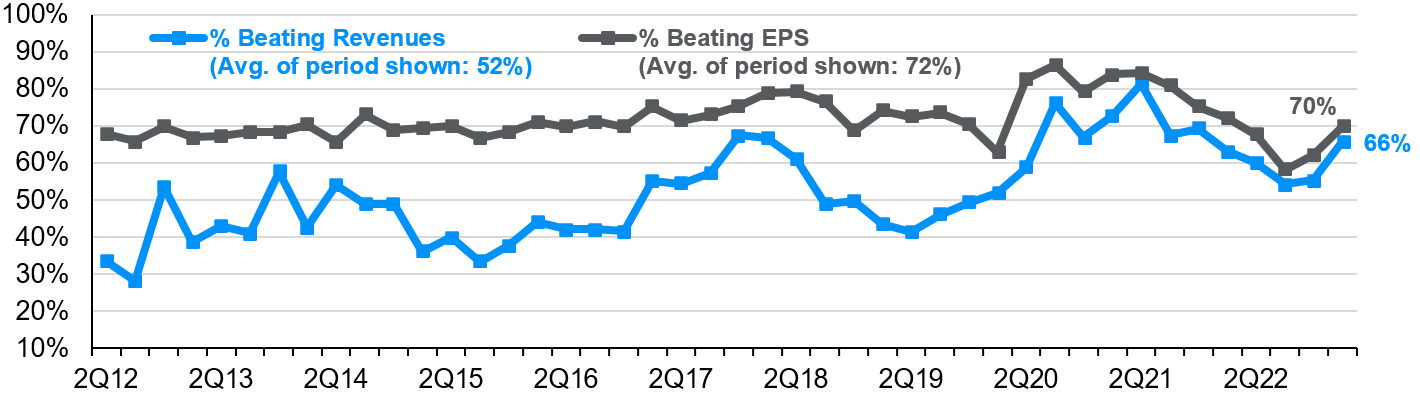

The good news is that the first quarter earnings season has delivered better than expected results. As of writing, with 424 companies reporting (86.1% of market capitalization), our current estimate for 1Q23 S&P 500 operating earnings per share is $51.26. If realized, this would represent year-over-year earnings growth of 3.9%, and quarter-over-quarter growth of 1.8%. Thus far, an impressive 70% of companies have beaten earnings estimates while 66% of companies have beaten revenue estimates, both of which are in line with or above their long-run averages. Importantly, both earnings and revenue surprises have been positive, with earnings beating by an average of 5.7%. Meanwhile, and arguably most importantly, profit margins bounced in 1Q23, with our current estimate tracking 11.5%.

Exhibit 1: % of Companies beating Revenue and EPS estimates

Source: BEA, Standard & Poor’s, J.P. Morgan Asset Management. Data reflect most recently available as of 05/05/23.

With interest rate expectations too dovish, the risk of recession rising, and profit estimates likely to remain under pressure, it is difficult to be overly bullish on equities at current levels. Furthermore, there is no clear valuation advantage for stocks or bonds at the current juncture. In other words, investors in this environment should focus on hitting singles and doubles, rather than swinging for the fences.

As was the case in 2022, the outlook for earnings will depend on the ability of companies to defend their profit margins. There are effectively two ways for them to do this – pass along higher costs via higher prices or trim expenses. The earnings season thus far has shown that companies are embracing one of the two, or sometimes both, to maintain current levels of profitability.

The anatomy of a cycle

As earnings weaken, how do firms manage costs? When do they start cutting capital expenditures and headcount? Historically, if we look at the past four recessions, year-over-year operating earnings growth tends to trough prior to the peak unemployment rate, but still during the recessionary period. Since 1989, earnings growth has troughed an average of 2.75 quarters (8-9 months) prior to the unemployment rate peaking. Excluding the COVID-19 recession, the gap between earnings and unemployment is closer to 10 months.

Similarly, capital expenditures, as measured by nominal private domestic nonresidential fixed investment, tends to bottom an average of 2 quarters (6 – 7 months) after the trough in profits, or one quarter before the unemployment rate peaks. Put simply, for firms, the order of operations when it comes to cutting costs tends to be capex first and then employment.

Looking at current commentary, firms plan on reining in investment, but cuts will not be distributed evenly. In fact, many management teams noted that investment in technology, specifically artificial intelligence, will likely increase due to potential cost savings from optimization over the long run. As such, cuts will likely occur in structures and equipment.

Turning to employment, when potential weakness in earnings does filter through into the labor market, where will layoffs be the most acute? Although the labor market has cooled in recent months, strong demand for services has driven robust payroll growth in related industries. We are seeing a notable employment decline in the information industry, as tech companies reduce headcount amid pressures on margins.

Investment implications

The past few weeks have seen elevated interest rate volatility, but stock markets have been relatively well behaved. The bottom line is that performance in U.S. equity markets so far this year has been all about rates, a theme that should persist as earnings expectations gradually align with reality. This warrants a cautious approach to equity markets focused on quality and cash flow - defensive value names and profitable growth names seem to fit the bill. However, it will be important for investors to pay attention to the price they are paying for these exposures, as elevated valuations are likely to decline as markets recognize that aggressive monetary easing is not on the near-term horizon.