Government bond yields have been on the rise since early this year. This has presented more room to manage the impact of rate hikes. To show how big this leeway could be, the breakeven point of a bond could be an indicator to look at.

A bond fund’s total return is generally determined by bond yields and the change in bond prices. Generally, when interest rates rise, bond prices would fall. Bond yields can therefore act as a buffer when bond prices decline. Different bonds react differently to changes in interest rates and the yields would also vary. A breakeven point can then be the indicator to help investors assess the magnitude of the yield level that could offset the impact of interest rate hikes. With a higher breakeven point, a bond would have more room to manage the impact of rising rates.

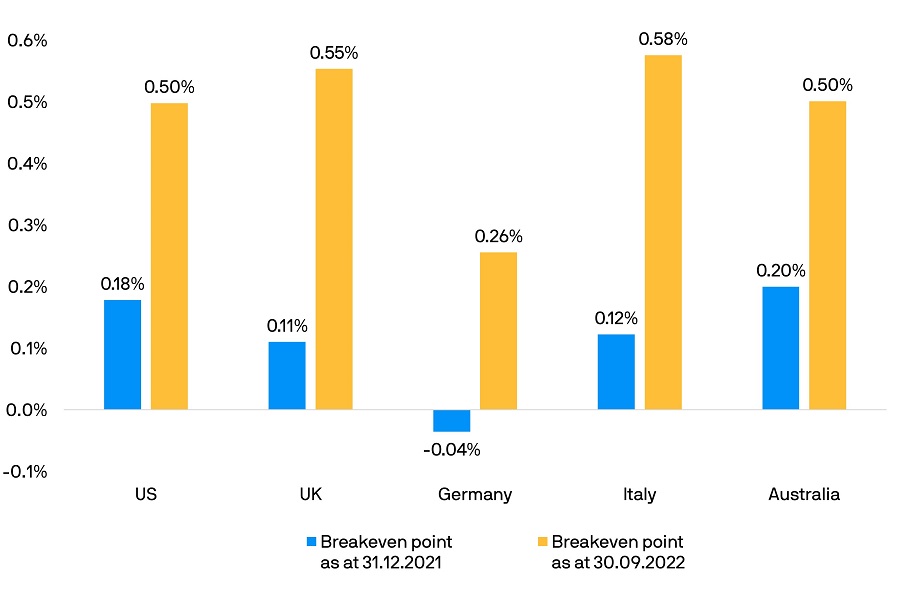

More room in global government bonds to help offset rate hikes

Some major central banks have been aggressively hiking interest rates this year, prompting government bond yields to rise in tandem with their breakeven points.

Take the UK 7-10 year gilt1 as an example, its breakeven point stood at 0.11% at the start of 2022 – which meant that it had 11 basis points to help buffer the impact of falling bond prices, as illustrated in the chart. This figure rose to 0.55%2, which indicated that prices would have to drop further to fully erode income from the bond’s coupon.

As such, government bonds currently present a bigger buffer, compared with early 2022, even with the continuous rise in interest rates.

Changing breakeven points across global government bonds

2. Source: J.P. Morgan Asset Management and Bloomberg, as of 30.09.2022. US refers to the ICE BofAML 7-10 Year US Treasury Index; UK refers to the 7-10 year UK Government Bond Index; Germany refers to the 7-10 year German Government Bond Index; Italy refers to the 7-10 year Italian Government Bond Index and Australia refers to the 7-10 year Australian Government Bond Index. Take the US as an example, its breakeven point was calculated by dividing the yield-to-maturity of the ICE BofAML 7-10 year US Treasury Index with its duration. Duration is a measure of the sensitivity of the price (the value of the principal) of a fixed income investment to a change in interest rates and is expressed as number of years. Indexes do not include fees or operating expenses and are not available for actual investment. They do not represent the fund portfolio. Yield is not guaranteed. Positive yield does not imply positive return.

Using global government bonds to help manage volatility

Market volatility will likely persist in the short term amid continuing rate adjustments to tackle inflation.

We believe that government bonds could do more, in addition to acting as a buffer against rate hikes. Historically, government bonds are relatively less volatile, and they are generally granted the higher credit quality rating. As such, they can be a tool to help manage volatility within an overall portfolio to cope with slowing economic growth economy.