Long-term investing is an essential and key component in financial planning. For some people, the process of achieving their financial goals can seem overwhelming, and this could sometimes lead to hesitation over when and how to begin investing.

In a two-part series, we share our insights on five frequently asked questions (FAQs) on long-term investing. We begin this investment journey with the first two FAQs.

1. When should I start investing?

Some people may wonder when is an optimal time to start investing. And the answer - based on your investment objectives and risk appetite, start as early as possible so that you can use time to your advantage.

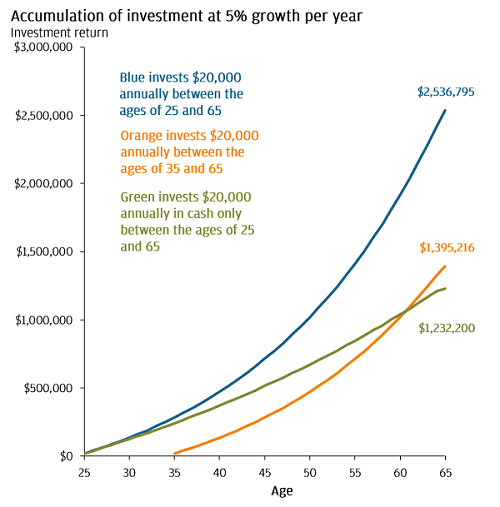

- With medical advancements, people are generally living longer, healthier lives. It is key to start investing early to optimise the benefits of compounding over a long period of time. As illustrated in the chart1, investing US$20,000 a year for 40 years, with a 5% return each year, could potentially yield US$2.54 million, compared with US$1.23 million based on just cash deposits.

- A key reason to start early is that the investment in early years can benefit most from the compounding effect over a long period of time. As a young person embarking on a career, this could be an opportune time to define your financial goals, craft a plan and get started on investing.

Harness compounding1

1. Source: J.P. Morgan Asset Management. Investment involves risks. For illustrative purposes only, assumes a 5% return on investment and a 2% return on yearly basis on cash in investors’ base currency with no indication and/or implication of actual return of investments. Actual investments may incur higher or lower growth rates and charges or even negative growth rates. Data reflect most recently available as of 30.06.2021.

2. How to take the first step in investing?

Just as you would choose a destination before you start travelling, you would need to set financial goals for your long-term investing journey.

- Our financial needs differ when we reach different stages of life. The more common financial needs could include further education, marriage, buying a home, raising a family and retirement planning. Setting clear financial objectives is like having a good global positioning system (GPS) that can guide us towards our life goals.

- Defining your financial goals and crafting a plan to achieve these objectives could help you stay on track in your long-term investing journey, even as your life, the markets and the economy change. After you have decided on how much to put towards each goal, based on your priorities, you could next create an investment strategy that allows you to take advantage of the longer investment horizons for goals with longer time frames.

- Additionally, it is optimal to have a reserve fund of liquid short-term investments and cash so that you can cover emergencies and upcoming large expenses without having to sell your investments during down markets.