At his first meeting as Federal Reserve (Fed) Chair, Kevin Warsh led the Federal Open Market Committee (FOMC) to a unanimous decision to hold the Federal Funds target rate range at 3.50-3.75% -- a disciplined debut for a chairman market had pegged as eager to cut, with inflation still running above target. That said, the statement saw a meaningful format shift from previous communications; it was cut in half. The prior April statement was a classic four-paragraph template detailing a reaction function and explicit forward guidance; both were completely stripped out. It also dropped the easing bias entirely, removing the language “the extent and timing of additional adjustment” which aligns with the recent hawkish dissents from the prior meeting.

As a result, the statement’s assessment of growth, labor and inflation were succinct. Growth was referenced as “solid” and noted that productivity growth and capital investment are strong, a clear nod to Warsh’s optimistic view on AI’s potential for productivity gains. Description of labor improved to reflect a job market better in balance, stating job gains have kept pace with the workforce. On inflation, it attributed the rise in prices to the energy supply shock, though emphasized the central bank’s commitment to deliver on price stability.

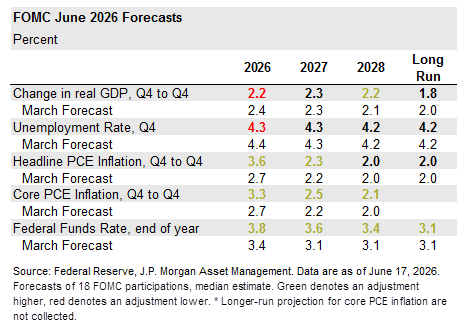

Turning to the Summary of Economic Projections:

- Growth was revised lower to 2.2% from 2.4% this year, and broadly unchanged over the next two years.

- Unemployment was lowered by 0.1% to 4.3% in 2026 and untouched over the forecast period.

- Headline and core inflation saw sizeable increases rising to 3.6% from 2.7%, and 3.3% from 2.7%, respectively, this year. Further out, inflation doesn’t reach target until 2028.

- Notably, the median interest rate forecast indicates one rate hike this year, followed by one cut in 2027 and 2028. While Chair Warsh declined to submit forecasts, the committee remains split as nine of eighteen participants foresee at least one rate hike this year.

The Chair used the press conference as an opportunity to announce five task forces whose remits entail:

- Frequency and type of Fed communication which may include revisions to how the central bank communicates views to the market.

- Fed balance sheet – assess the benefits and risks of an ample-reserves regime

- Use and reliance on source data – explore methodological changes to improve data gathering and real-time accuracy

- Productivity and jobs – during a period of transformation, survey the pace, reach and impact of new general-purpose (AI) technologies on the labor market and output

- Fed’s inflation frameworks likely leaning more on trimmed-mean measures of inflation rather than traditional CPI and PCE methodologies.

The Chair expects these task forces to begin work starting in the fall and conclude their findings by year end. Notably, Warsh was explicit that he does not foresee any change to the Fed’s long held 2% target. We continue to expect no rate adjustments from the Fed this year, as the committee appears comfortable it can remain patient given where policy rates are. Yields rose and stocks fell as the initial read may be considered hawkish. Altogether, while there will likely be changes to the Federal Reserve under this new Warsh regime, the central bank’s dual mandate of price stability, maximum employment, and its use of the Federal Funds rate as its primary policy tool appear cemented.