- What is securities lending?

Securities lending is a long-established practice that can increase returns for shareholders in our investment funds that participate in the J.P. Morgan Asset Management Securities Lending Programme.

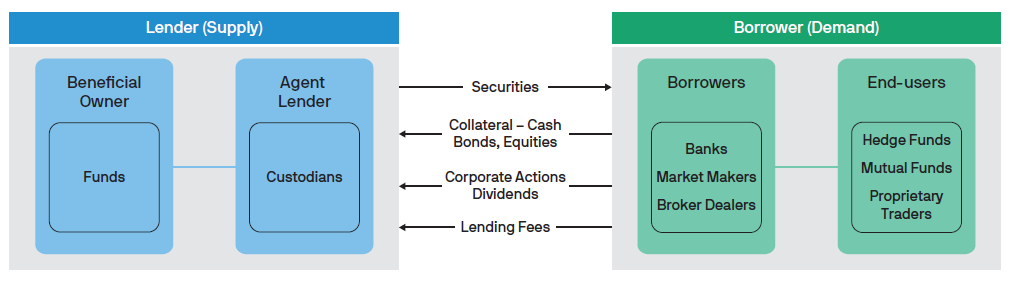

Securities lending works by allowing a fund to temporarily lend securities that it owns to an approved borrower in return for a fee. The borrower is required to provide sufficient collateral to compensate the fund if the borrower fails to return the loaned securities in the agreed timeframe, subject to certain counterparty and liquidity risks set out below.

How does the securities lending process work?

When a security is loaned, the title of the security as well as the associated rights and privileges of ownership are transferred from the fund, as lender, to an approved borrower. However, the fund remains economically exposed to the securities that have been lent and retains the key benefits of ownership, except for voting rights.

Securities lending typically has a number of important features:

- The borrower is required to return the borrowed securities on demand, i.e. an “open loan”.

- Prior to lending, collateral must be received by the lender from the borrower. The value of the securities that have been loaned (as well as the value of any securities provided as collateral) is calculated daily by the lending agent based on current market prices, and the amount of collateral backing the loan is adjusted accordingly.

- While the borrower receives all dividends/interest and corporate action rights on loaned securities, the borrower is contractually required to make substitute payments to the lender.

- The borrower also holds any voting rights attached to the loaned securities while the loan is in place, unless the lender recalls the loan. While J.P. Morgan Asset Management’s aim is for clients to benefit from the revenues generated by securities lending, our internal teams actively look to protect client interests on key voting issues. There is a process in place to identify, recall and vote on stock to ensure appropriate levels of governance.

- At the end of a loan, the securities are required to be returned to the lender.

- Revenue from lending is credited to the fund on a monthly basis.

- Securities lending is typically conducted through an agent who receives a portion of the lending fees. For JPMorgan ETFs (Ireland) ICAV (hereafter “ETFs”), J.P. Morgan SE - Luxembourg Branch is the appointed agent.

What are the benefits to investors?

Securities lending aims to generate additional income for a fund, subject to the risks outlined in the following section and in the funds’ prospectus. The revenue from securities lending is returned to the funds, net of the fees paid to the lending agents. The lending agent for the ETFs, currently receives a fee of 10% of the gross revenue for its services. The revenue received by the funds from securities lending transactions is specified in the funds’ semi-annual and annual reports. The Management Company does not receive any revenue or compensation related to the funds participating in J.P. Morgan Asset Management Securities Lending Programme.

What are the main risks and how does J.P. Morgan Asset Management control these risks?

The J.P. Morgan Asset Management Securities Lending Programme is designed to add value for clients by providing a potential additional source of incremental return while mitigating risks, and provides oversight of the lending agent appointed by the funds.

Some of the key guidelines and principles in place allowing for a low-risk programme are:

Agent obligations:

Our lending agents have obligations to compensate losses suffered by the funds where a borrower fails to return loaned securities.

Collateralisation:

To cover market fluctuations and exchange rates, borrowers are required to supply collateral with a higher market value than the securities on loan (typically, 102% to 105% for government securities or cash and 110% for equity securities). All loaned securities are valued every business day at their current market value, and collateral levels are maintained at pre-determined levels. Typically, the board of each fund decides what collateral is accepted by a particular fund. Broadly, collateral accepted is select high-quality government securities, equities or cash, for J.P. Morgan ETFs.

Counterparty monitoring:

The J.P. Morgan Asset Management Counterparty Risk Team regularly monitors borrower exposures and reviews all approved borrowers on an ongoing basis.

Lending limits:

The funds currently have limits in place to control the amount that is lent and to monitor market exposure at 20% of assets under management (“AUM”). There are also certain European Securities and Markets Authority (“ESMA”) guidelines in force regarding collateral diversification and monitoring. More information can be found in the respective fund prospectuses.

The risks below are not fund-specific and so should be read in conjunction with any specific risks in the relevant fund prospectus.

Counterparty risk

There is a risk that a borrower could fail to return the borrowed securities. The default of a counterparty, together with any fall in value of the collateral below that of the value of the securities lent, may result in a loss to the fund. The above guidelines and principles are designed to mitigate this risk.

Liquidity risk

There is a risk that settlement of a sold security may be delayed if a borrower is not able to return it in time to the lender because of poor market liquidity. By giving the lending agent sufficient notice of the sale, the fund still receives sale proceeds on settlement date regardless of whether the trade has settled. This ensures that there is little to no impact on the day-to-day trading activities within the fund.

Note: the profitability of any securities lending programme is not guaranteed, and while the mitigating factors described above aim to control losses incurred, the effectiveness of such measures can also not be guaranteed.

Next steps

For further information, please contact jpmam.etf@jpmorgan.com

0903c02a82436678

This is a marketing communication and as such the views contained herein are not to be taken as an advice or recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/ emea-privacy-policy. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.