Despite rising energy costs, equity markets are buoyed by increasing earnings forecasts, driven by the AI capex cycle and demand for more sophisticated models.

In Brief

- Equity markets rallied to new highs despite the oil shock, while bond yields rose as investors focused on inflation and interest rate risks.

- Government intervention and demand destruction have provided only temporary relief from energy supply disruptions, with oil price volatility underscoring ongoing market uncertainty.

- Central banks held policy rates in April, but rising expectations for further hikes create opportunities in shorter-dated government bonds if economic conditions deteriorate.

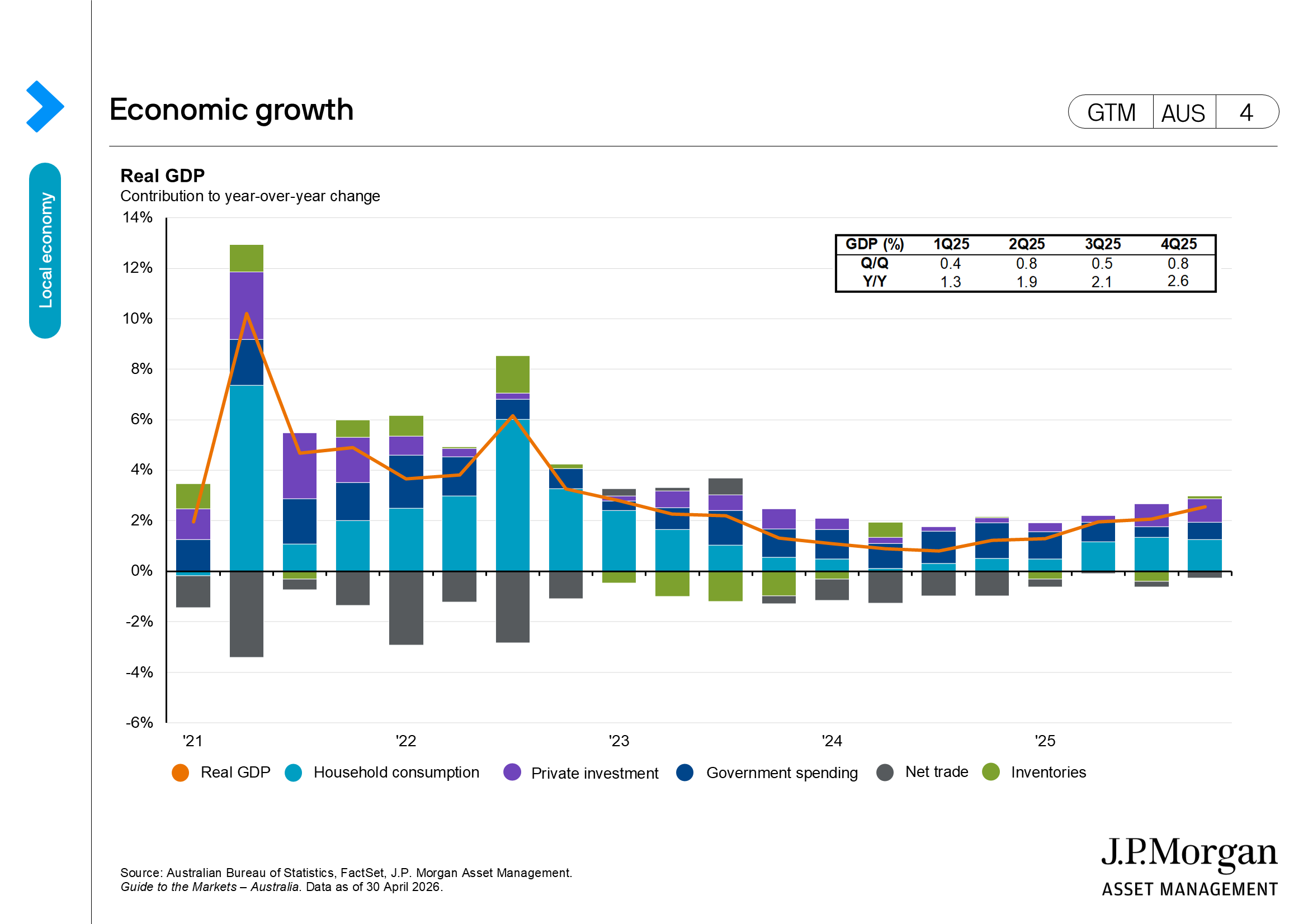

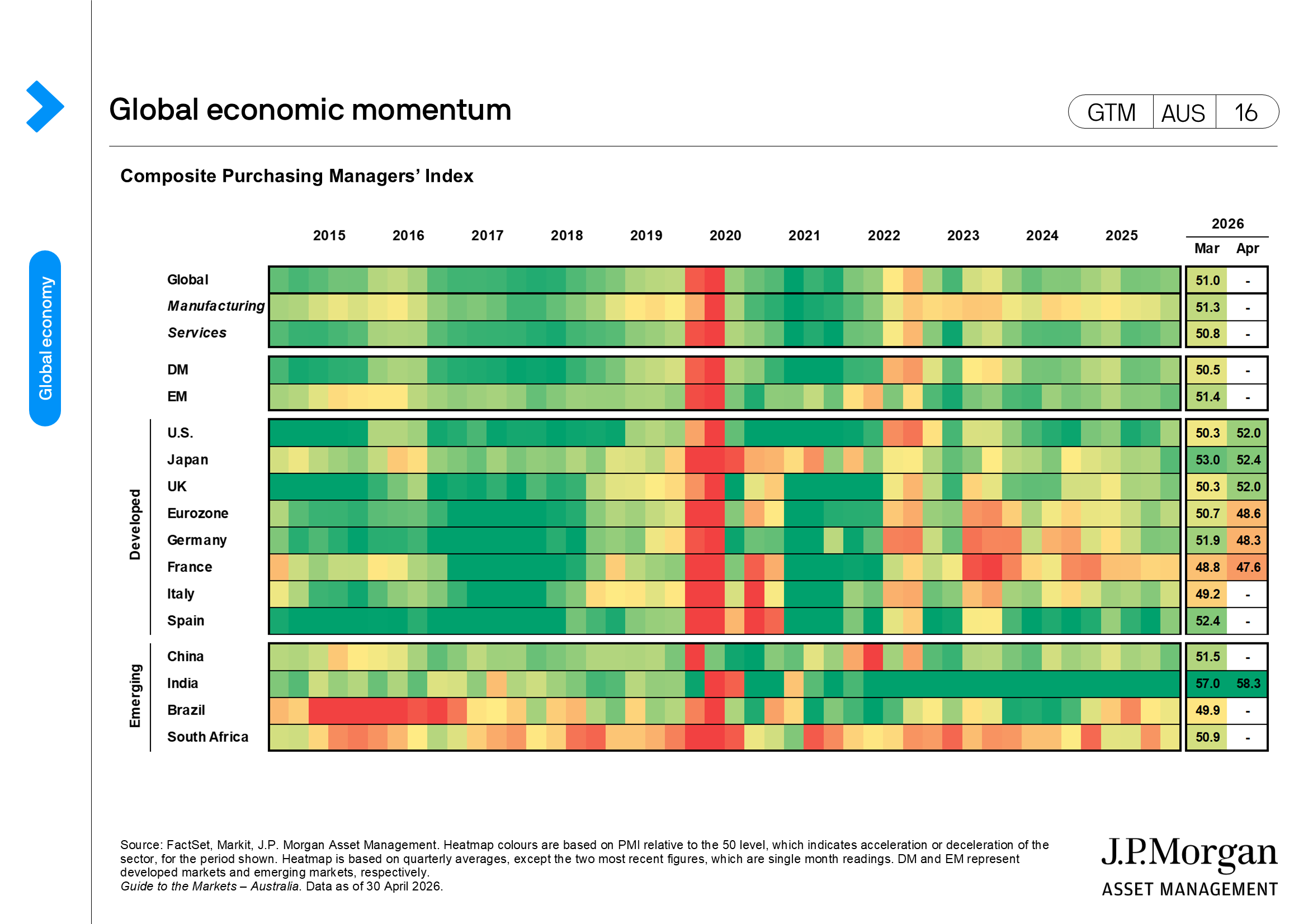

April showed a marked divergence in how assets are pricing the risk from a global energy shock. Equity markets rallied, with some reaching fresh all-time highs, as an extended ceasefire in the Middle East prompted both equity and credit markets to discount worst-case scenarios and the release of new artificial intelligence (AI) models helped to reignite investor sentiment towards this secular theme. Meanwhile, the bond market remains focused on inflation and interest rate risks, with yields reaching multi-year highs in some markets. Developed market equities gained 9.4% over the month, emerging market equities rose 13.3%, while the Bloomberg Global Aggregate Index was up 1.3%.

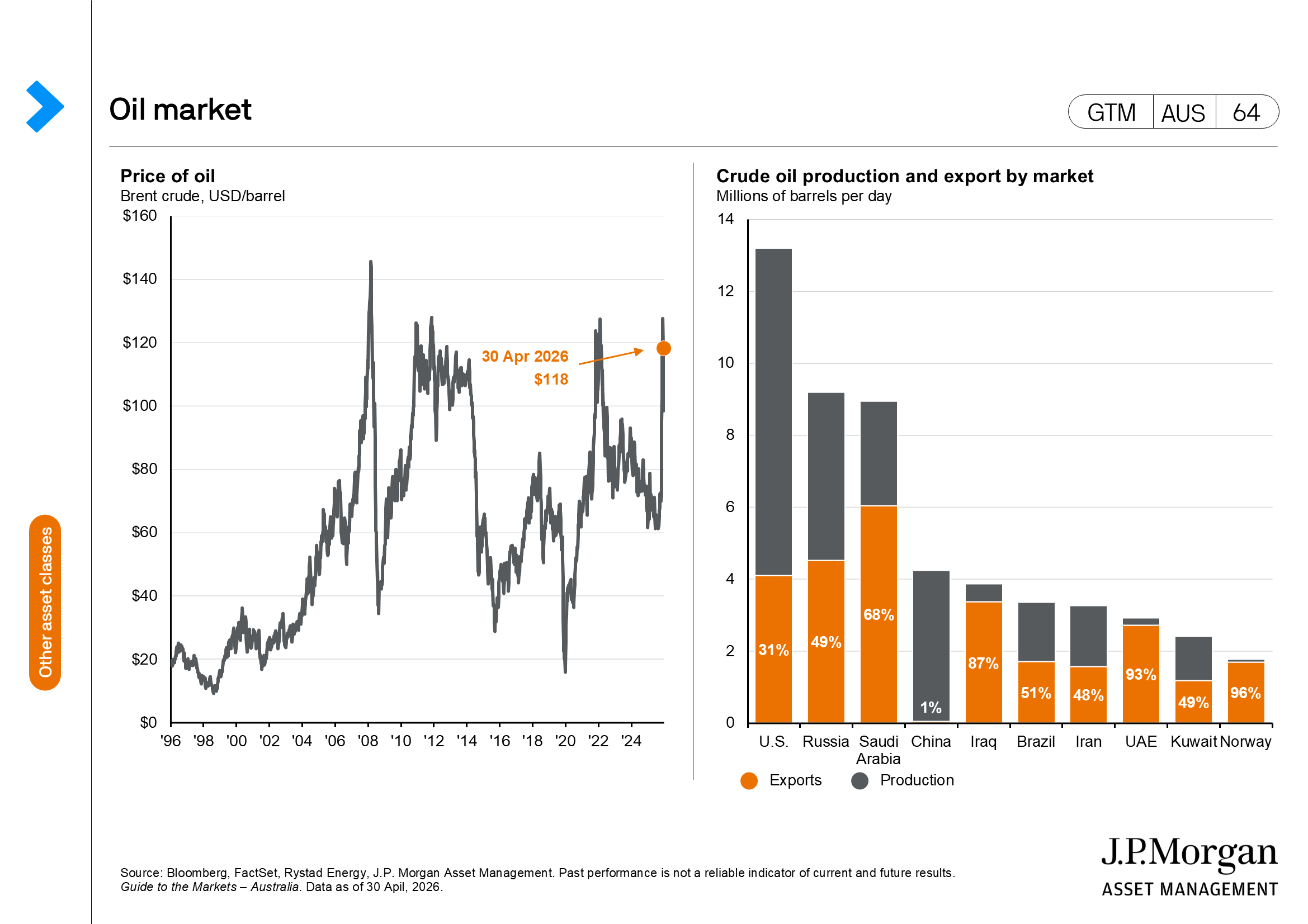

The ceasefire initially helped alleviate concerns about the duration of the conflict and the risk of renewed fighting. However, a ceasefire alone is insufficient to reverse the economic consequences of reduced oil and gas supplies. To ease supply pressures, governments have drawn down existing stockpiles, providing temporary relief to households. At the same time, there is increasing evidence of “demand destruction” as businesses and consumers adjust to higher energy prices. Nevertheless, these actions are unlikely to fully offset the magnitude of the disruption to energy supply. The oil price remains a key barometer of market risk, and the swings in Brent crude—from USD 101 to USD 90 to an intra-day high of USD 126 per barrel before falling back—highlighting the uncertainty facing markets.

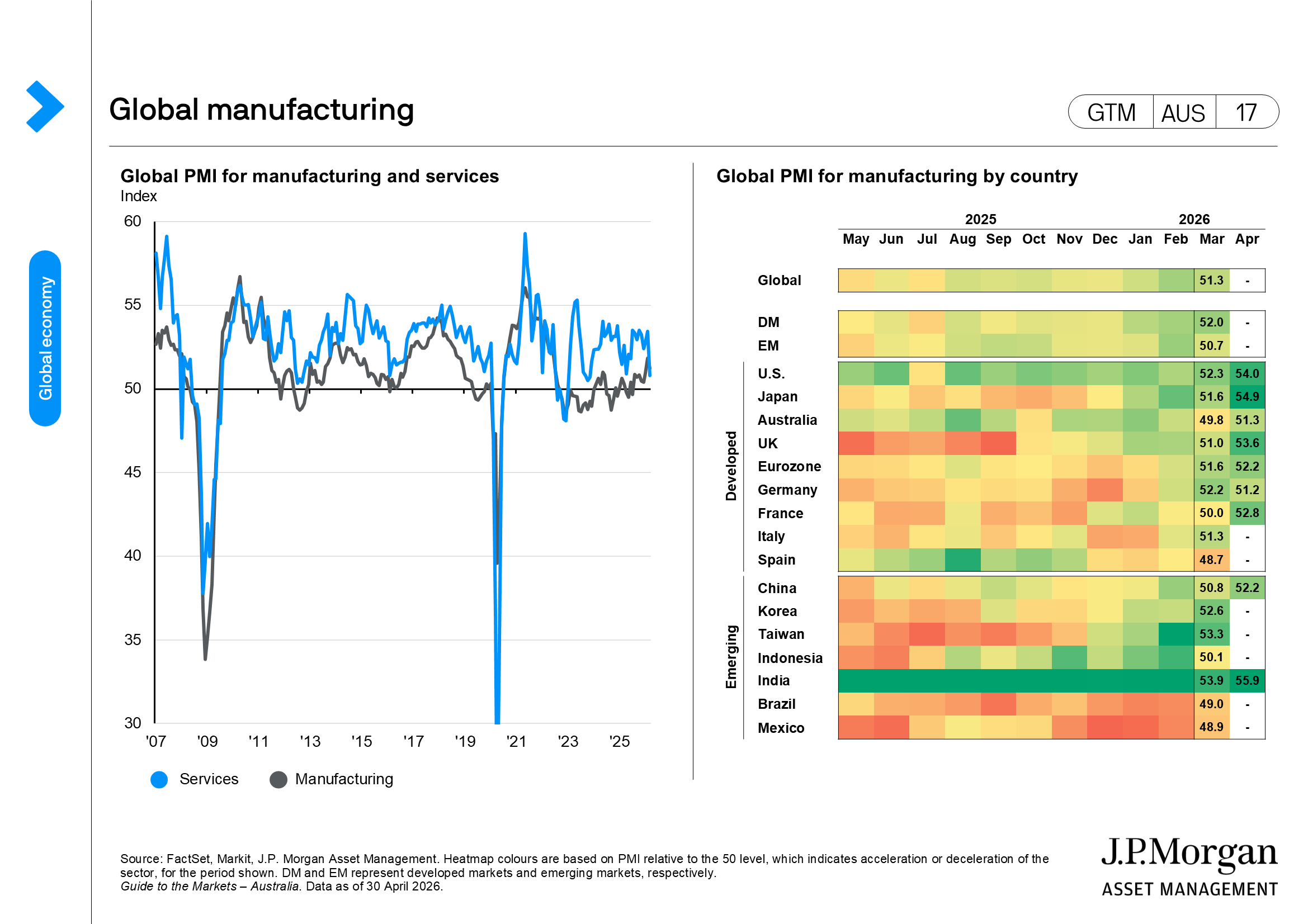

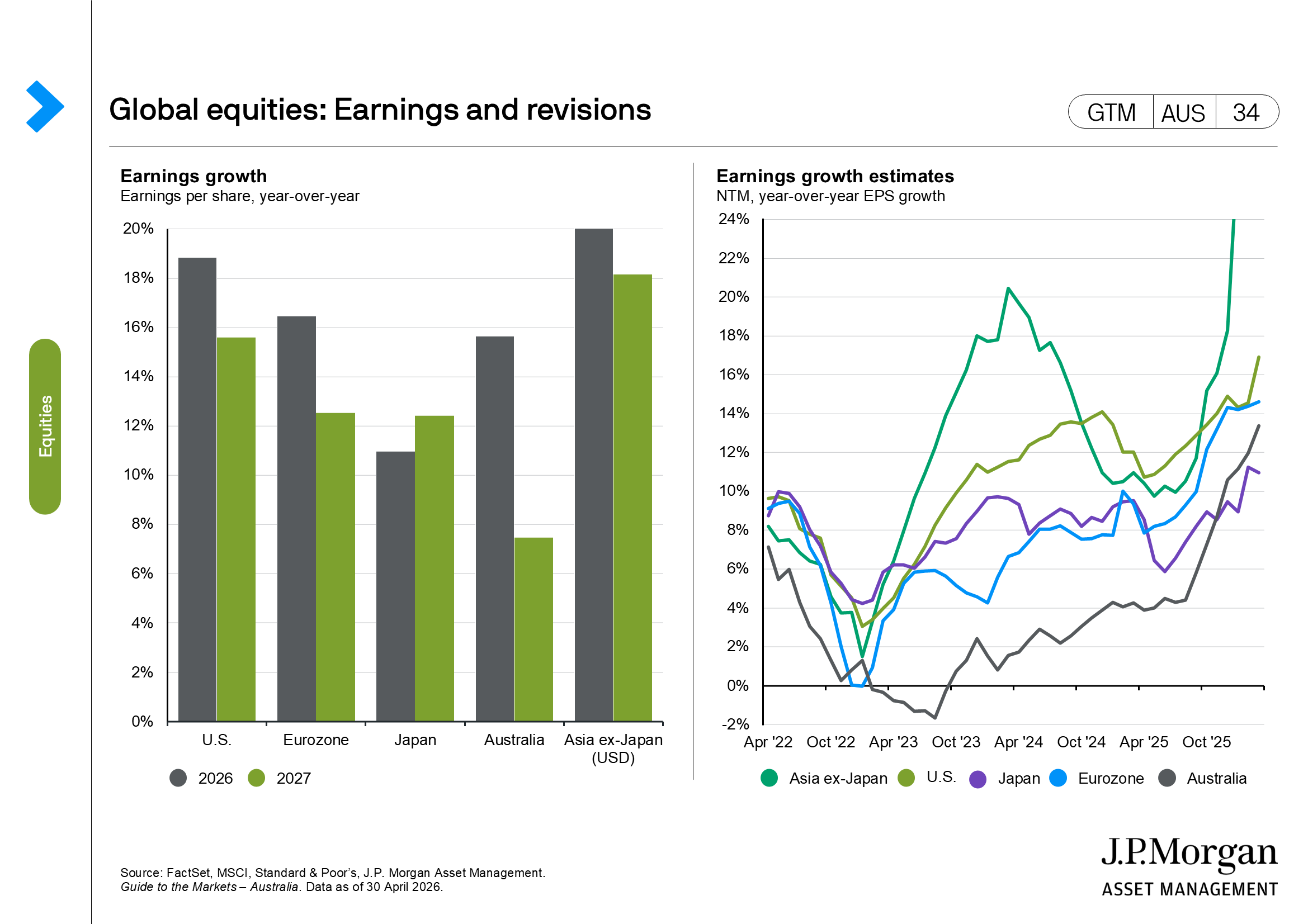

Despite rising energy costs, equity markets are buoyed by increasing earnings forecasts, driven by the AI capex cycle and demand for more sophisticated models. This has propelled U.S. equities and AI-adjacent markets (such as Japan, Korea, and Taiwan) to new all-time highs. The positive earnings outlook also helps explain the tightness in credit spreads, as investors focus on micro factors and healthy corporate fundamentals to offset looming macro headwinds.

Safe havens have been challenged as the disconnect between equity and bond markets has widened. Yields on 10-year government bonds across major developed economies are roughly 40 basis points (bps) higher than when the conflict began, reflecting adjustments for inflation risk and tighter monetary policy. Shorter-dated yields have also risen, as expectations grow that central banks will raise rates to combat inflation.

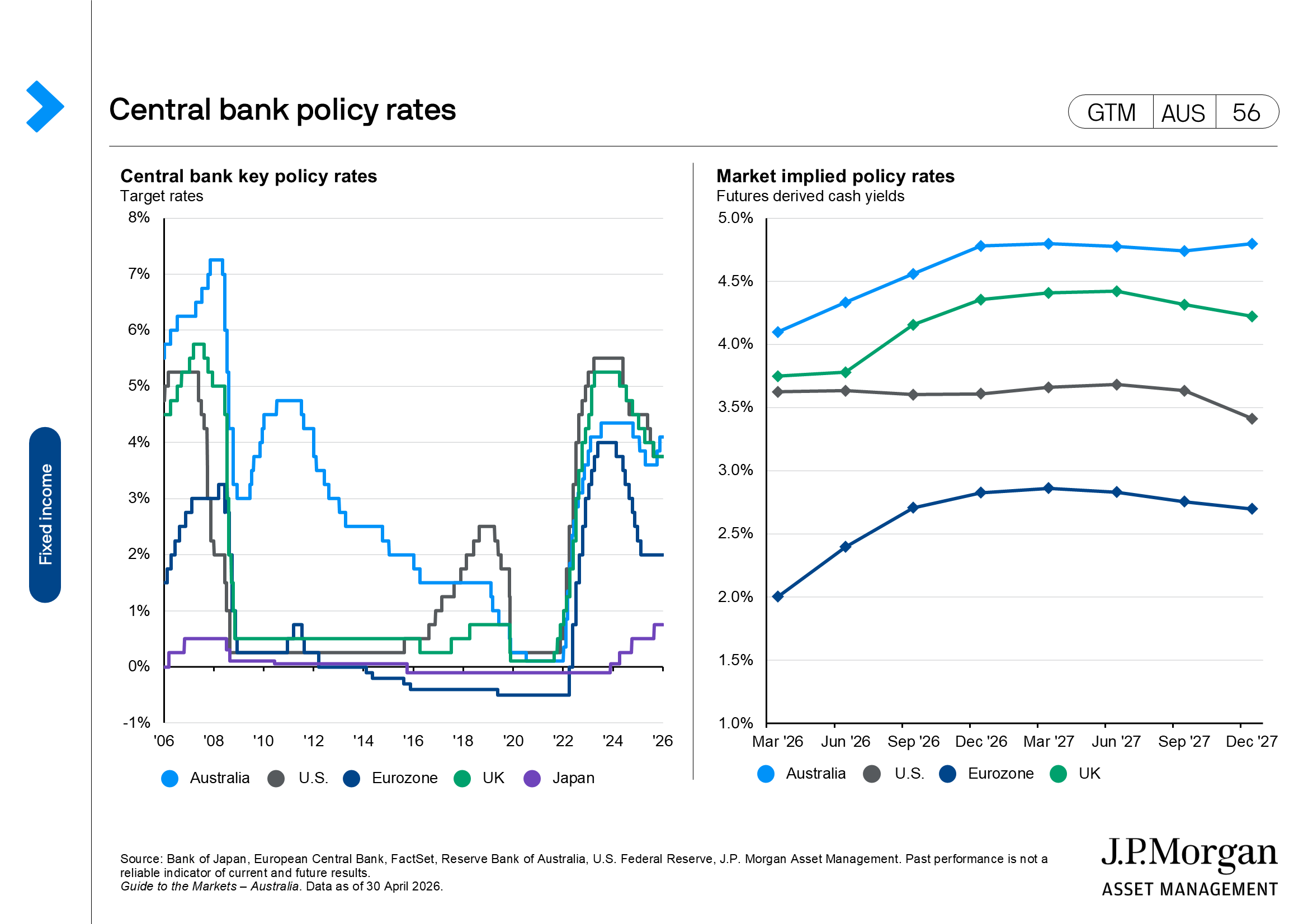

Central banks may remain patient as they assess the growth and inflation outlook. The outcomes of the April meetings by the U.S. Federal Reserve (Fed), European Central Bank, Bank of Japan, and the Bank of England were consistent: all highlighted inflation risks and kept policy rates unchanged. Expectations are rising for multiple rate hikes this year from major central banks, with no further easing anticipated from the Fed. This creates an opportunity in shorter-dated core government bonds, as these expected hikes may not materialize if the economic outlook weakens in the coming months.

Australian economy

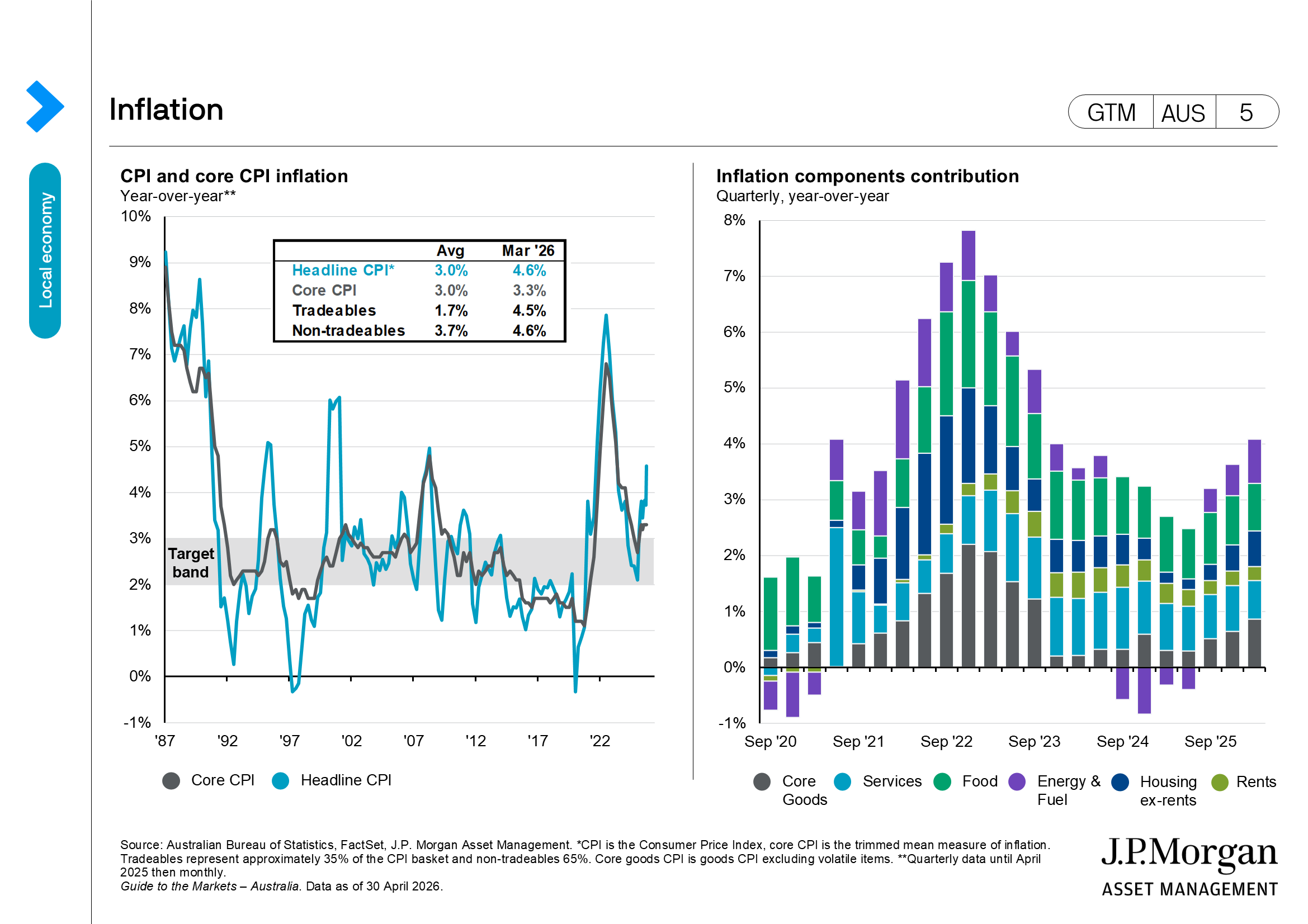

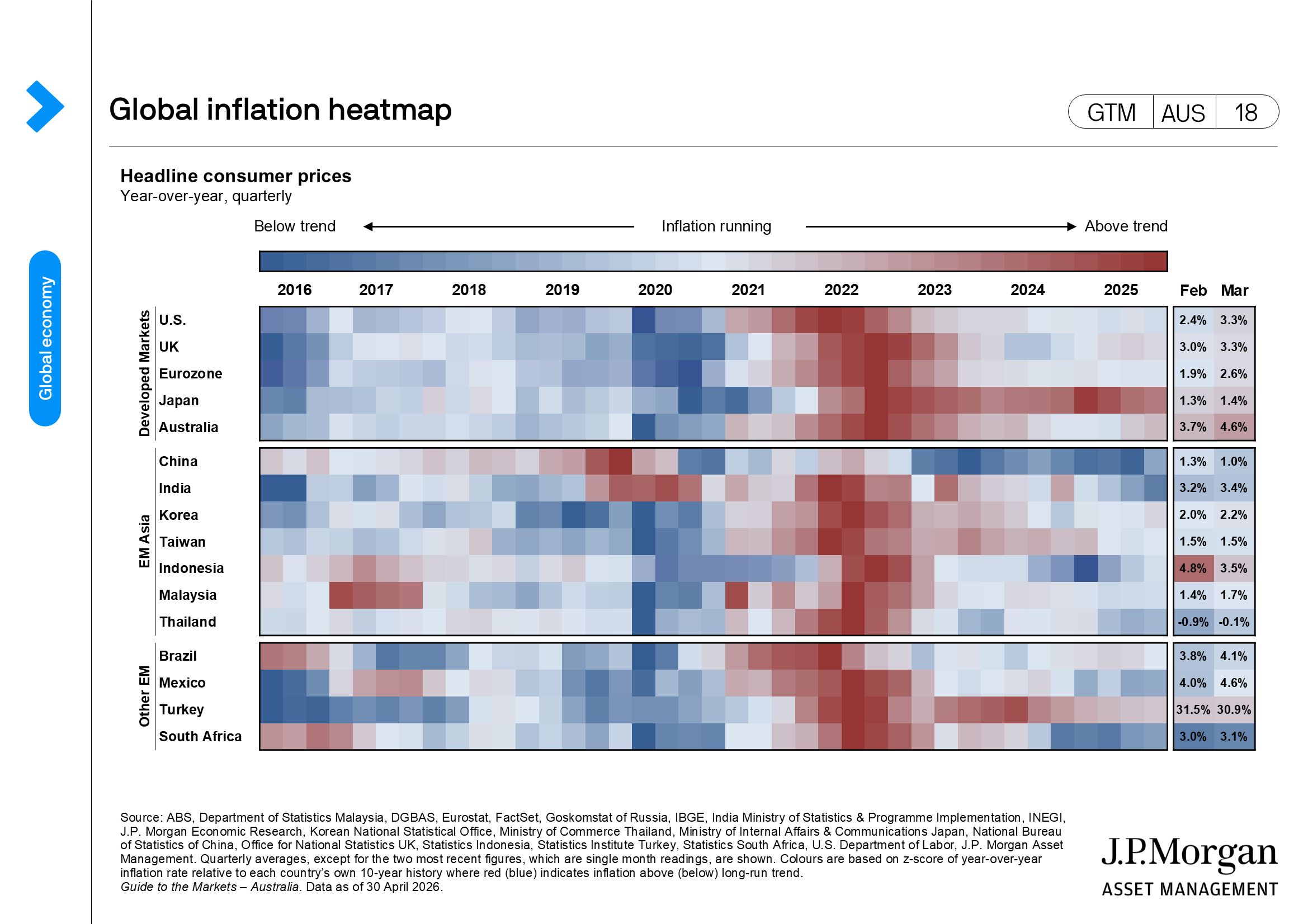

- Inflation spiked to 4.8% year-over-year (y/y) in March, but the trimmed mean inflation rate was steady at 3.3% y/y. The higher headline rate of inflation was unsurprisingly the result of higher automotive fuel costs and the end of government electricity subsidies. These two factors contributed 1.5% pts to the headline inflation rate. Underlying inflation pressures may not be as bad as feared, but remain outside the top of the Reserve Bank of Australia’s (RBA’s) target band. This is likely to see the RBA hike rates at its May meeting as it seeks to anchor inflation expectations, as well as raising its inflation forecasts for the rest of the year.

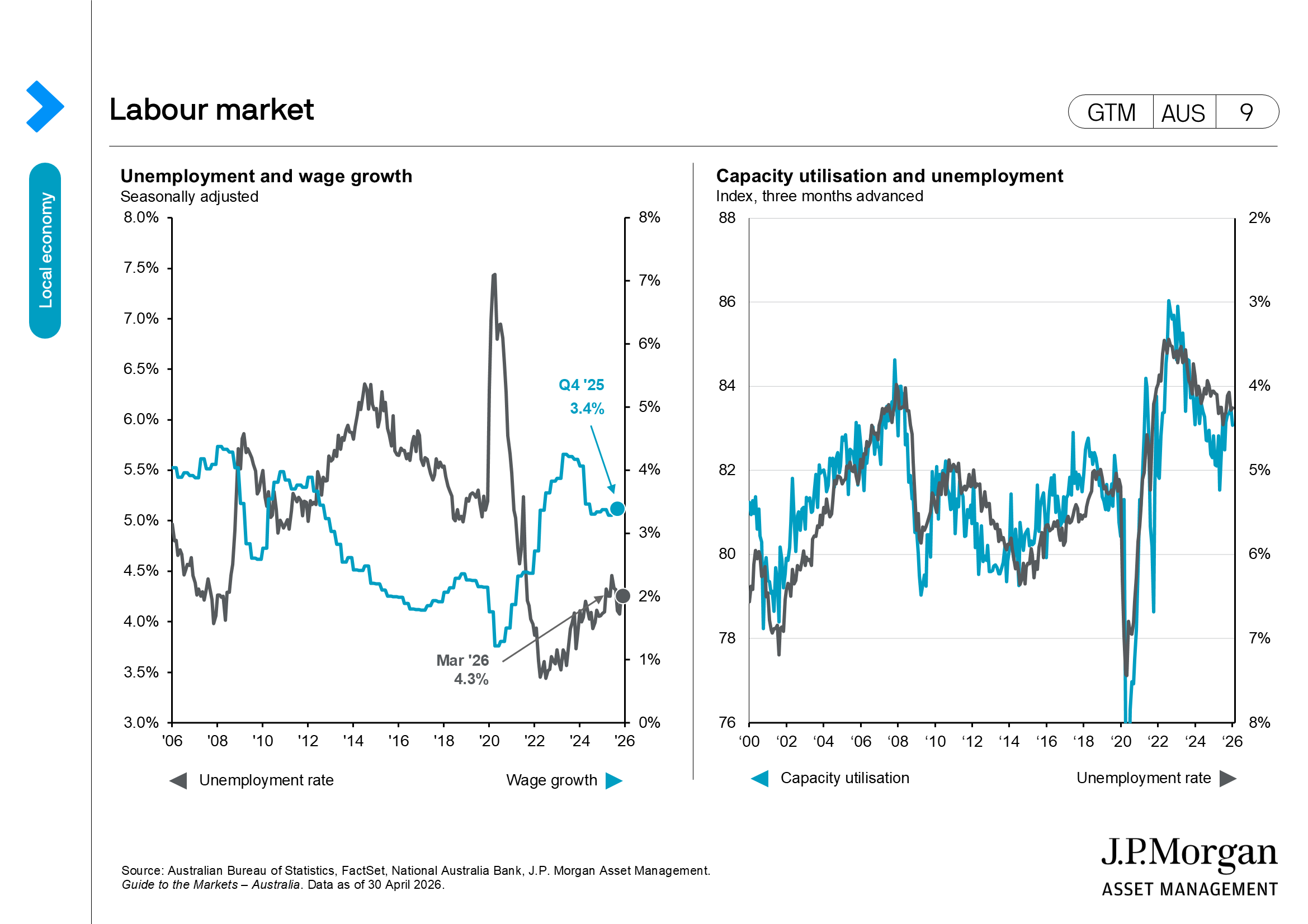

(GTM AUS page 5) - The unemployment rate was steady at 4.3% in March, and while still low by historical standards, is at the upper end of the range for the past 18 months. Even with a steady unemployment rate, jobs growth demonstrated more volatility month over month. In March, 53,000 full-time jobs were added while part-time employment fell by 35,000. This was a complete reversal from the February data.

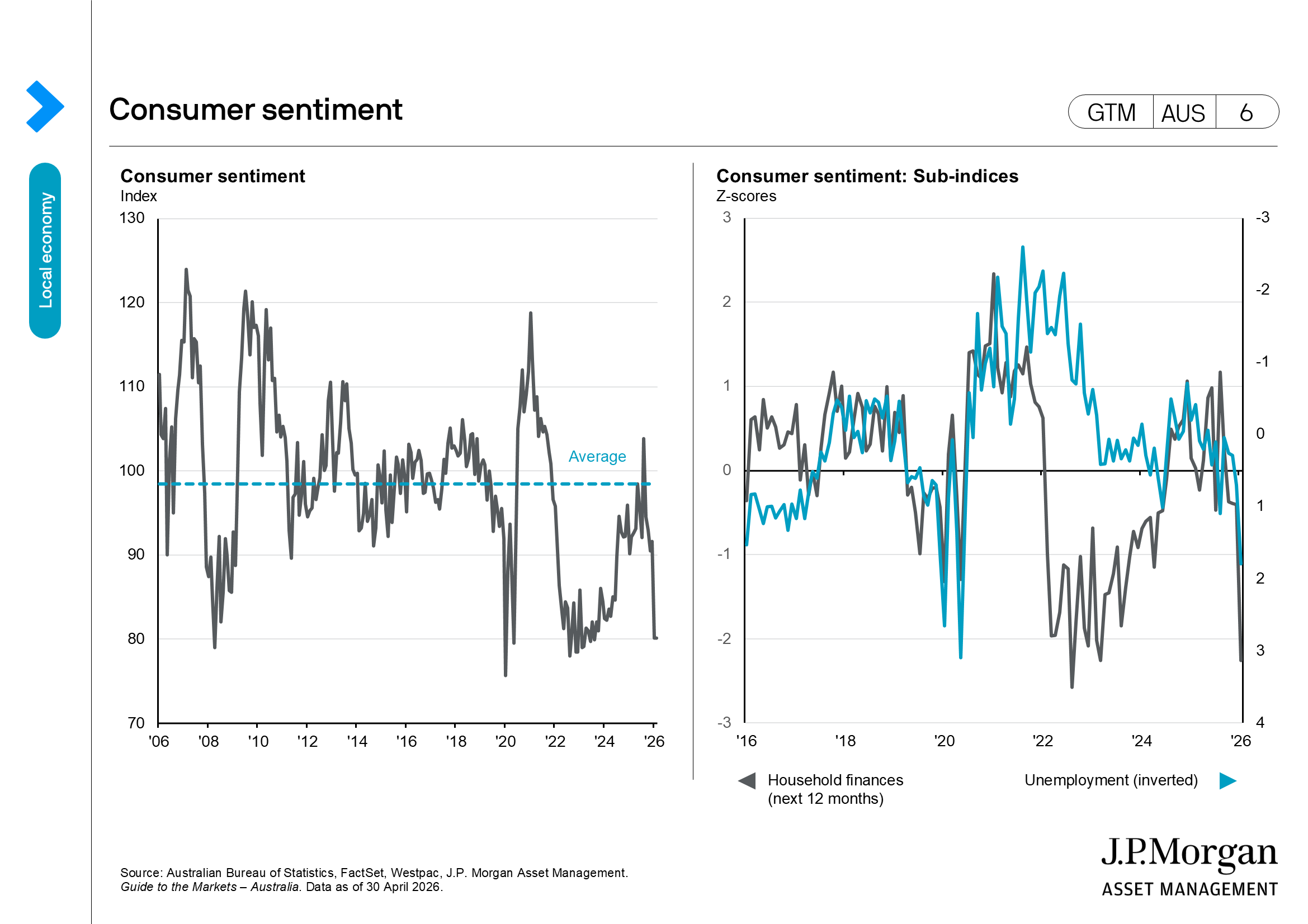

(GTM AUS page 9) - Business confidence collapsed in March, falling 29 pts, and is at one the lowest readings outside of the COVID-19 period, as companies deal with the uncertainty surrounding surging fuel prices. Consumers weren’t feeling much better as consumer inflation expectations jumped to 5.9% and consumer sentiment indicators have turned sharply lower.

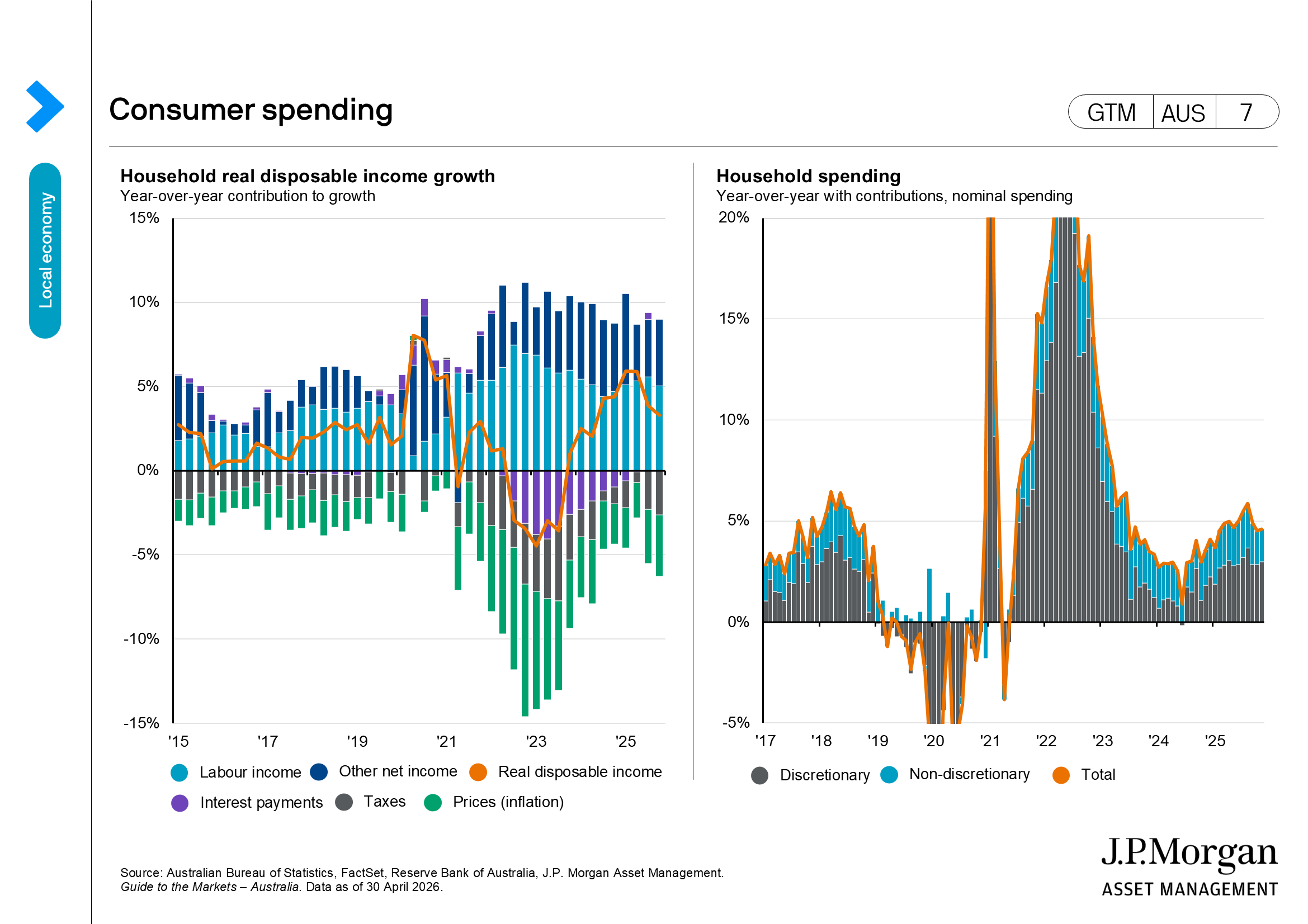

(GTM AUS page 6) - Despite the weakness in sentiment, household spending has shown some resilience, as discretionary spending rebounded early in 2026. However, this is likely to change given the impact on household budgets from higher fuel prices and interest costs.

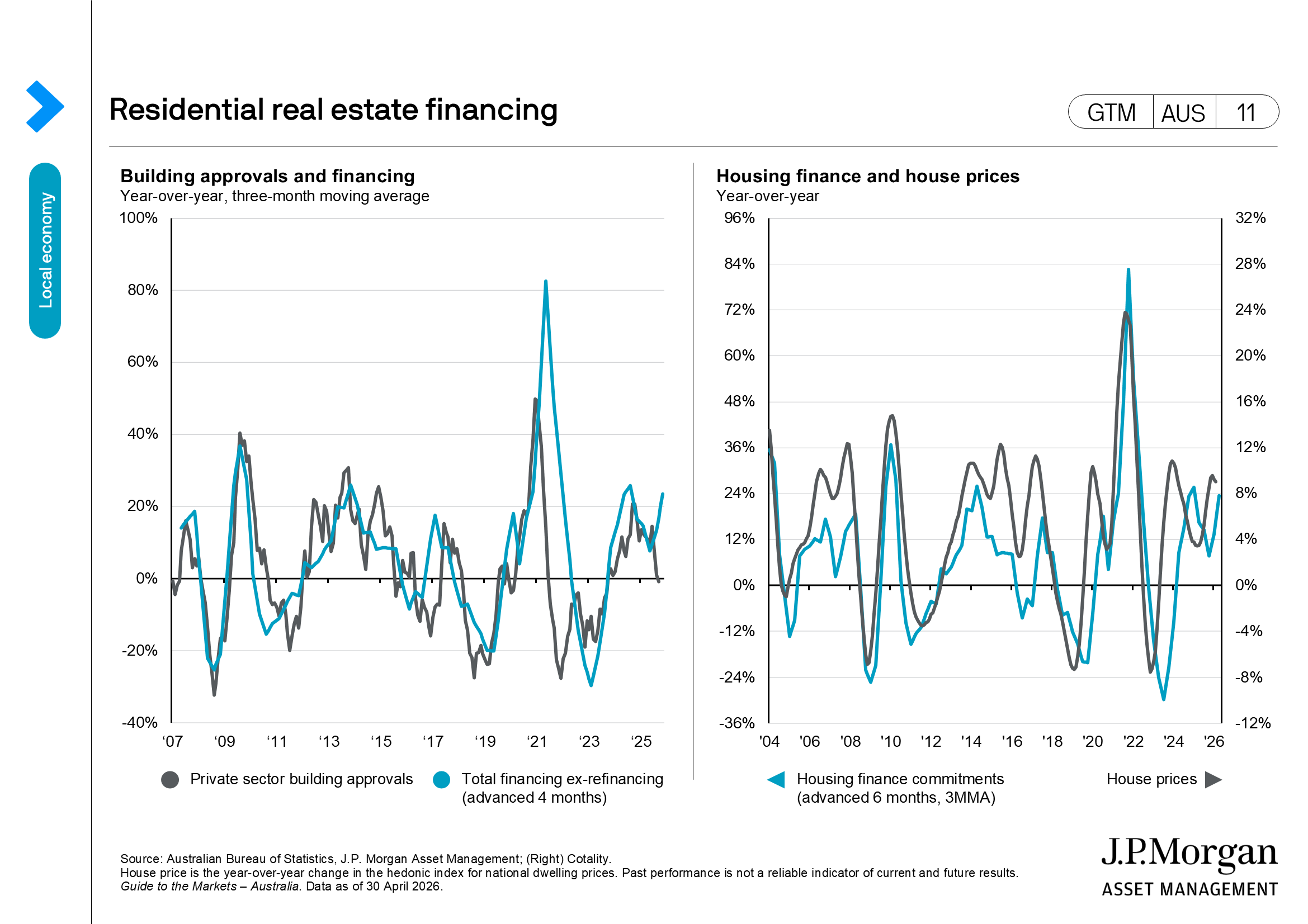

- Credit growth was strong in March and increased by 8.1% y/y, its fastest pace since 2022. All three categories of housing, business and personal were stronger. The faster pace of consumer credit suggests that some are willing to “borrow to spend”.

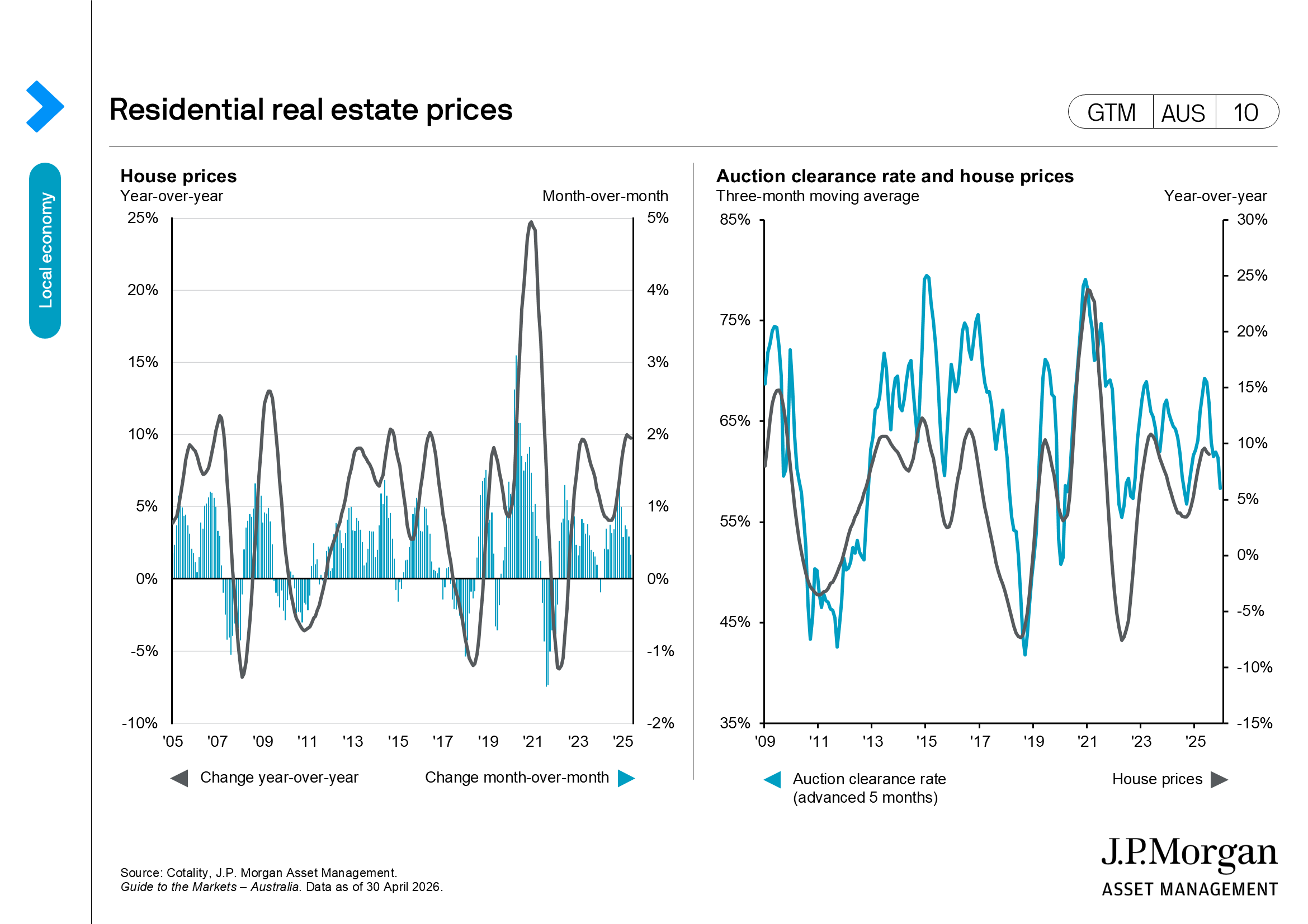

(GTM AUS page 11) - Housing prices in Australia slowed in April from the prior month, rising by 0.3% month-over-month (m/m), but still a sturdy 9.8% y/y. While the market has been resilient to higher borrowing costs, higher mortgage rates are likely to be a headwind to further activity. The decline in auction rates suggests a shift in sentiment. (GTM AUS page 10)

Equities

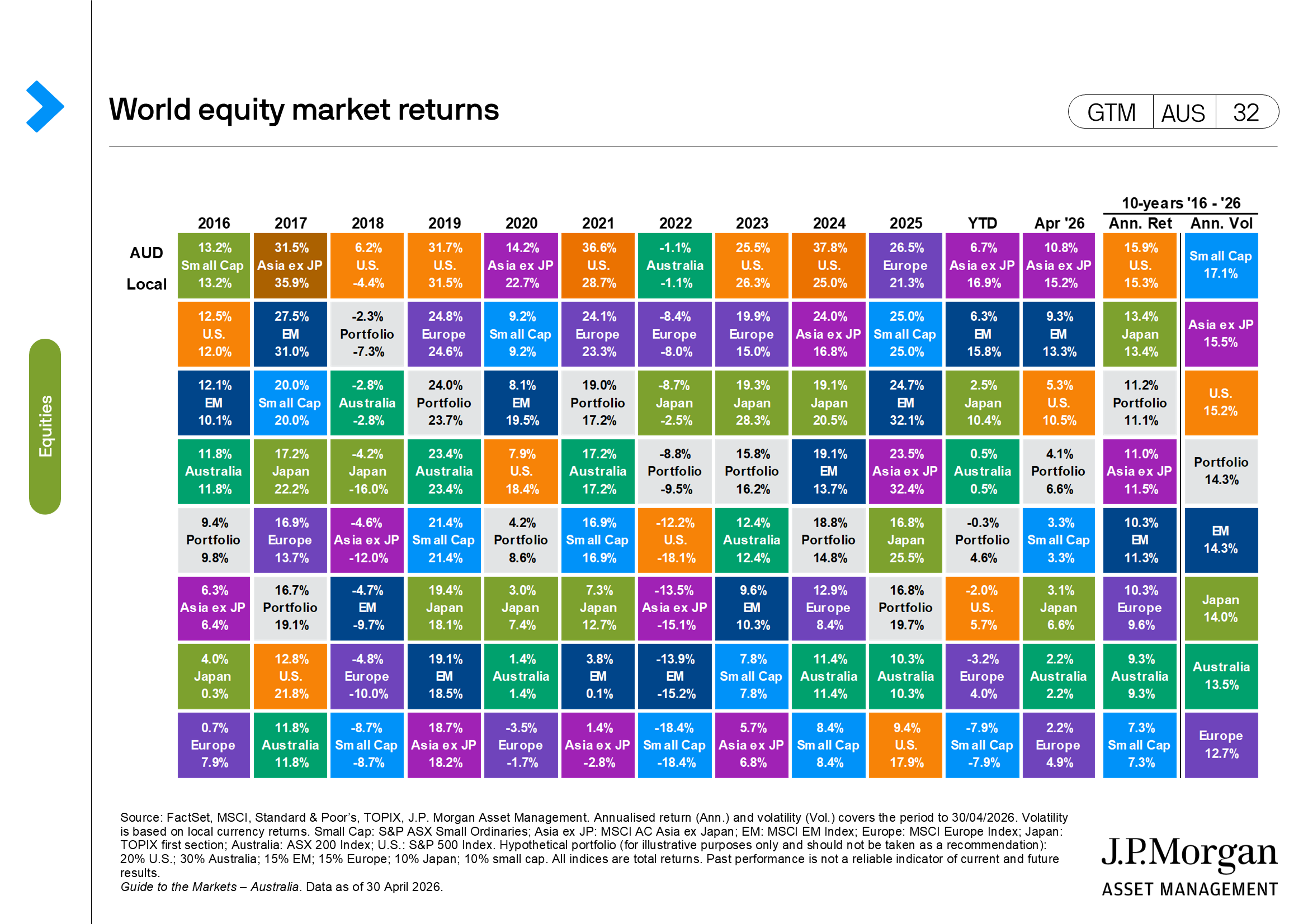

- The ASX 200 gained 2.2% in April and is now flat for the year. Seven of the 11 sectors were in the green with IT (13.2%), real estate (8.1%) and materials (4.3%) leading the returns. Meanwhile, healthcare (-8.7%), consumer staples (-4.1%) and energy (-2.7%) were the laggards. In the small cap space, the Small Ords rose by 3.3% with stronger returns in IT (14.6%) and materials (6.4%) helping to lift the index (Total returns, local currency).

- Emerging markets outperformed developed ones as Asian markets surged, driven higher by the positive outlook for the “picks and shovels” providers to the AI theme. The MSCI Asia ex-Japan rose by 15.2%, and the Korean and Taiwan equity markets leapt 33.9% and 22.7%, respectively. The U.S. (10.5%) was the best performer across developed markets given the higher weight of tech names. Concerns over the energy impact on European equities kept returns more modest (4.9%).

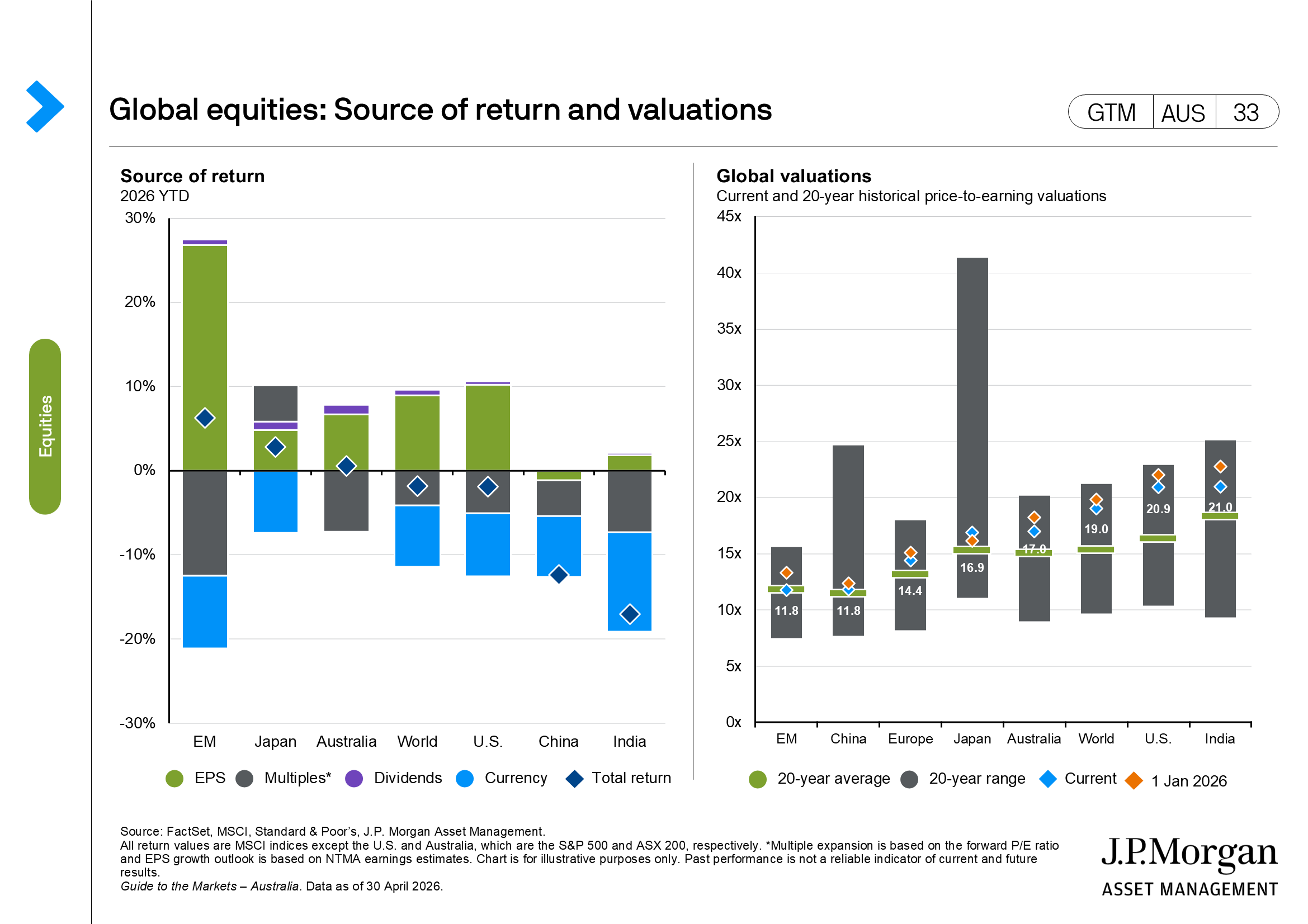

(GTM AUS page 32) - The earnings season in the U.S. has surprised to the upside, with 84% (vs. 73% average) of reported companies having beaten consensus earnings expectations, and earnings are 28.6% above expectations (vs 6.3% average). To date, 62.5% of the market cap has reported, with analysts estimating 14.5% y/y earnings growth in 1Q.

(GTM AUS page 33) - Valuations continue to creep higher. The S&P 500 ended the month trading at 21x forward price-to-earnings (P/E), but still below where it started the year. Meanwhile, the ASX 200 trades at 17.0x.

Fixed income

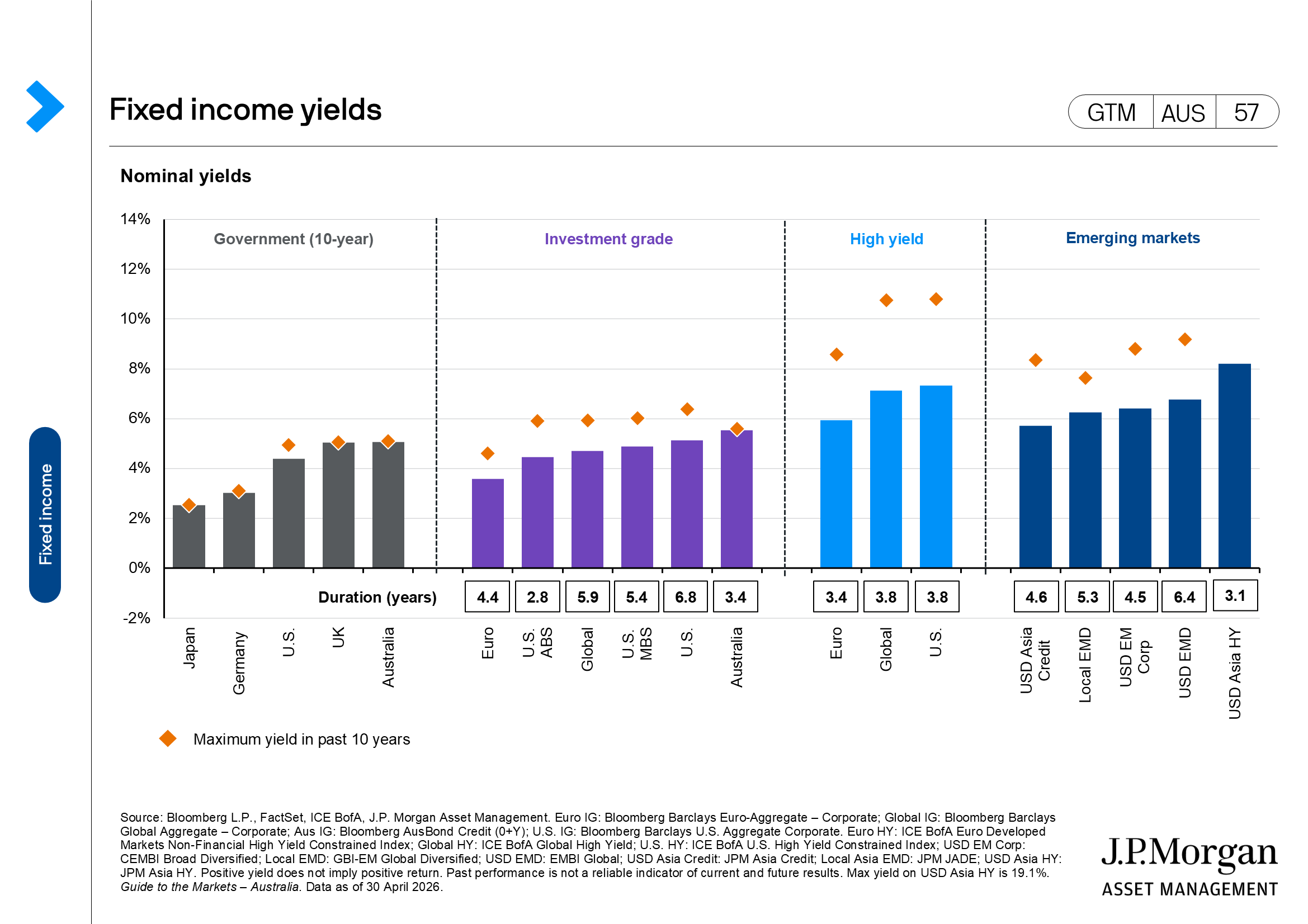

- Government borrowing costs continue to push higher. The yield on the 10-year ACGB was marginally higher over the month, up 9 bps to 5.07%. The higher inflation starting point compared to other markets as well as more hawkish policy makers, is keeping yields higher in Australia. In the U.S., the 10-year Treasury yield was 7 bps higher to 4.39%, but the shorter end of the curve moved by more, as the yield on 2-year Treasuries rose 9 bps as the market prices out rate cuts this year.

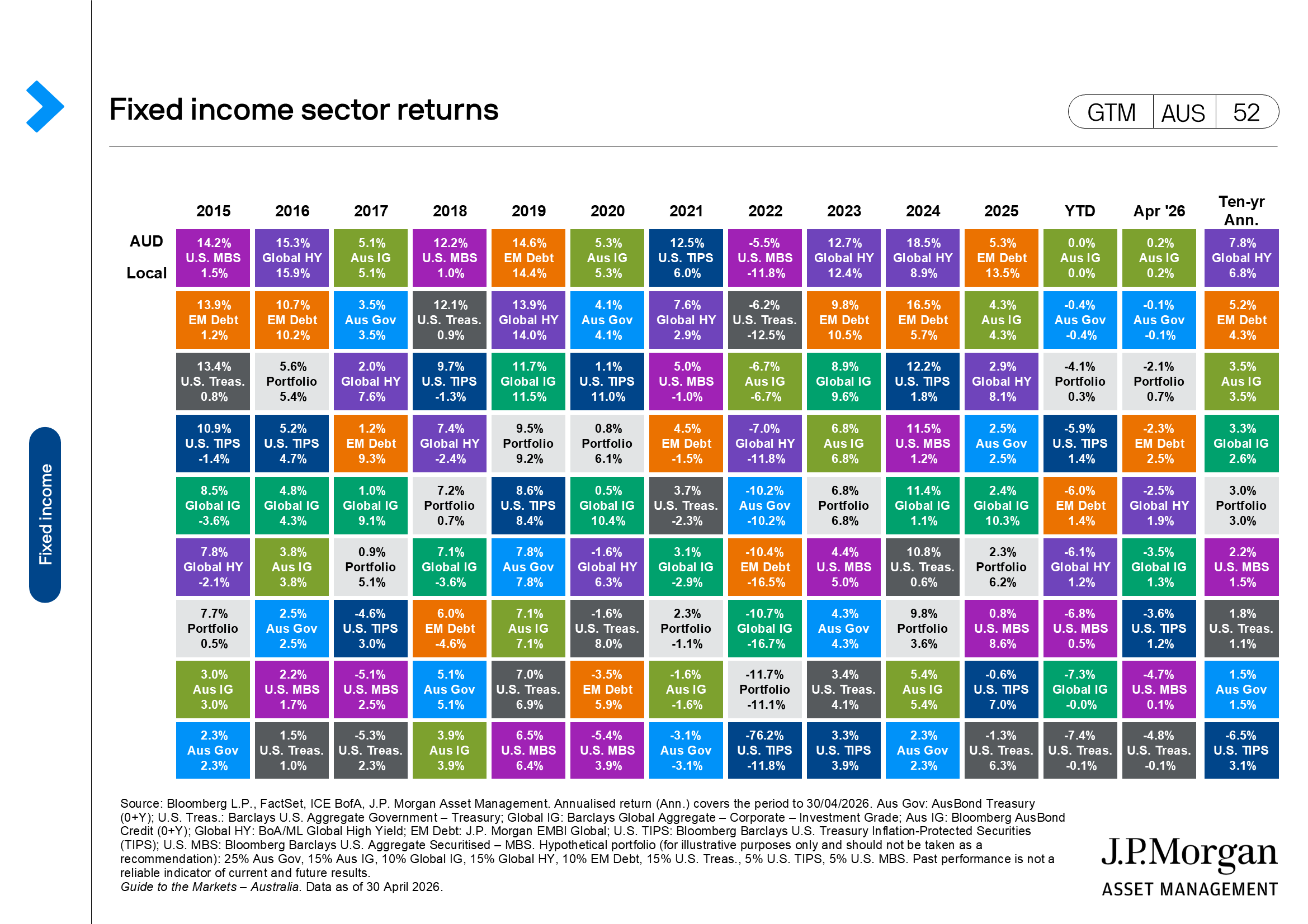

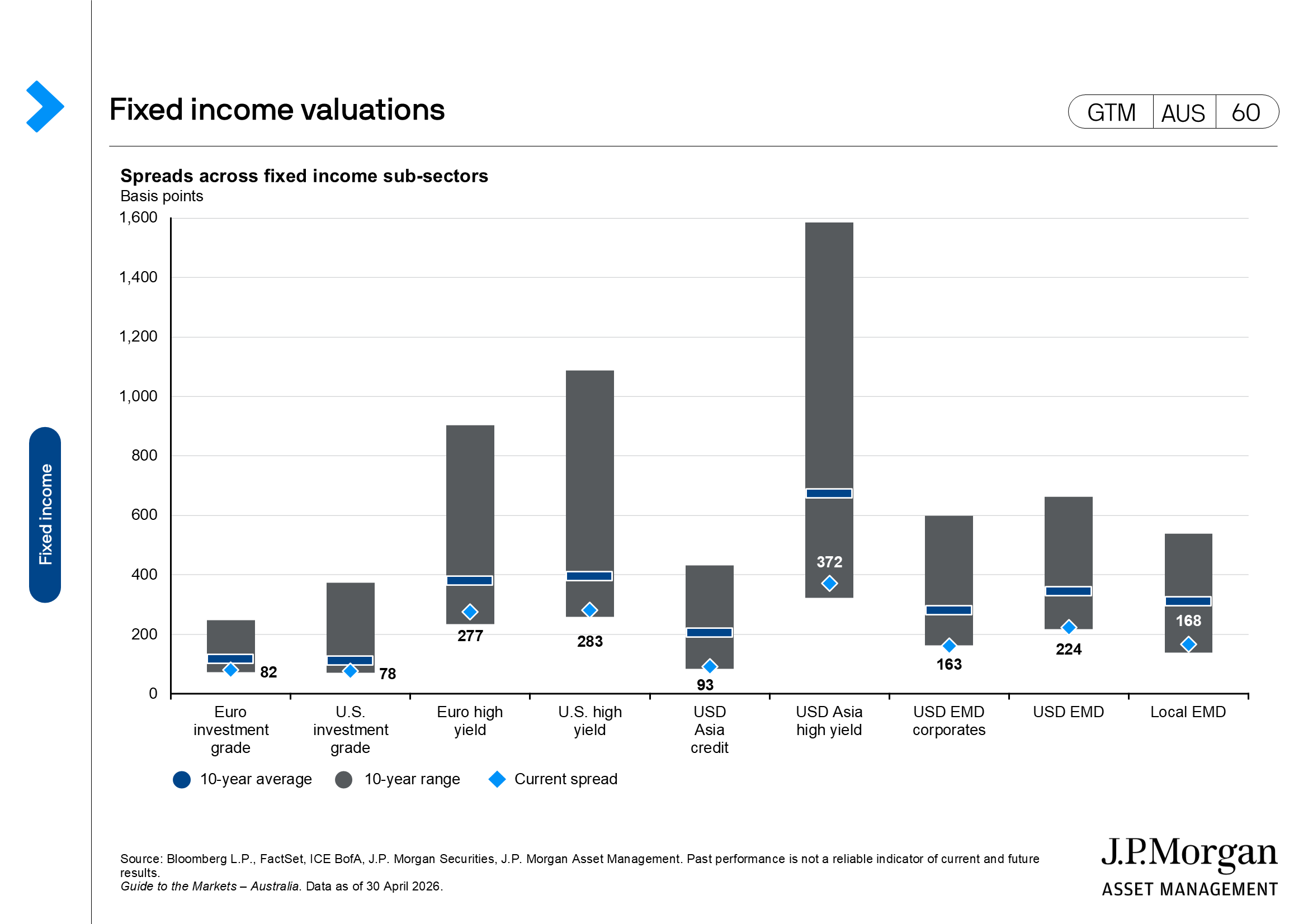

(GTM AUS page 56) - While core government bonds were down over the month, credit spreads retraced their earlier widening and are back near record tights. Global high yield returned 1.9% over the month and global investment-grade was 1.3% higher.

(GTM AUS page 52)

Other assets

- The price of a barrel of Brent crude was 13.7% higher over the month to USD 118 per bbl as the continued blockade of the Strait of Hormuz squeezes supply around the world. So far, it is not clear when the Strait may re-open, but the pressure on the economy and inflation continues to build as stockpiles are run down. Futures curves continue to point towards lower prices in the future.

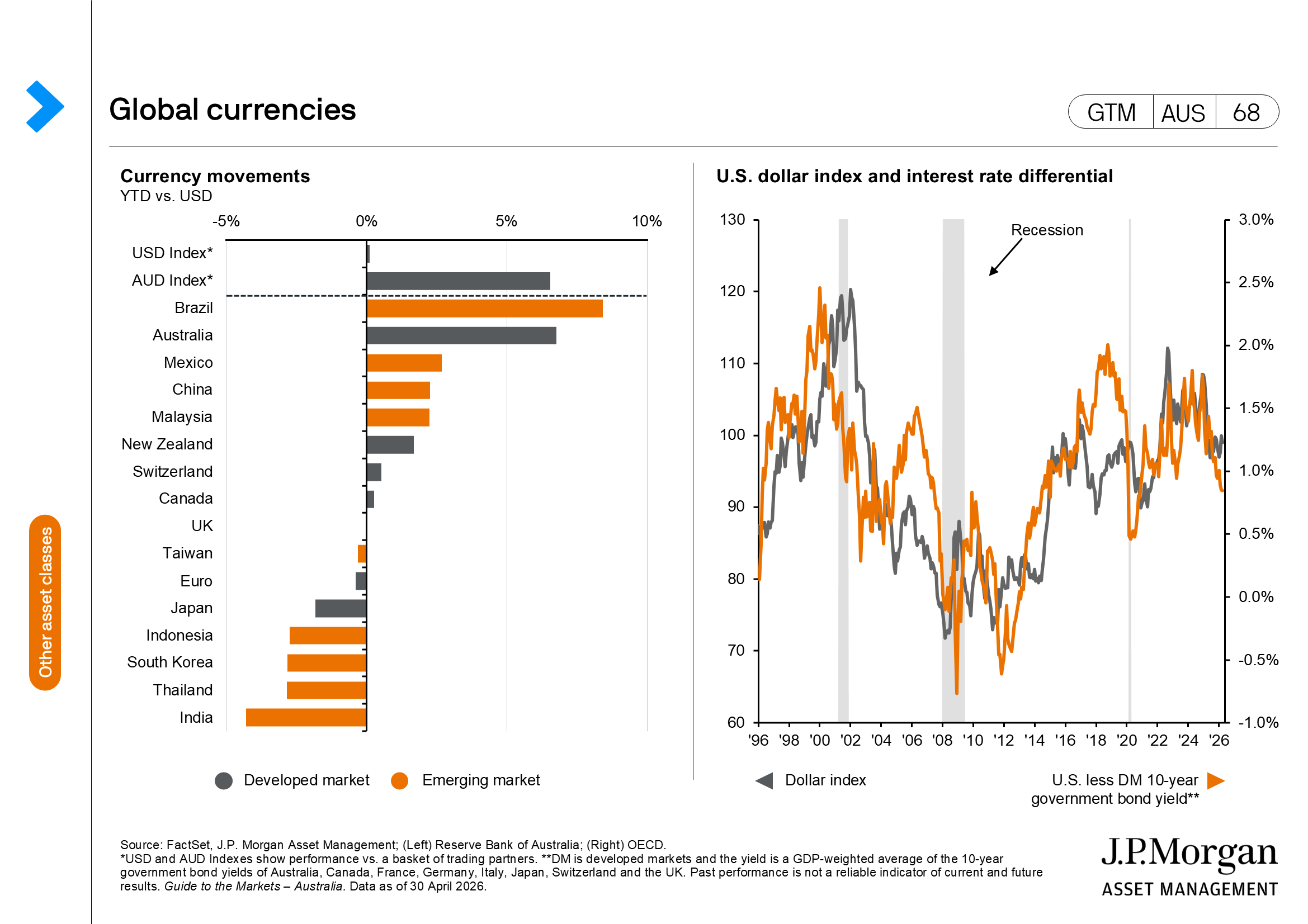

(GTM AUS page 64) - The USD is now flat for the year and gave up the minimal safe haven flows it saw earlier in the year, falling 1.9% over the month. Risk-sensitive currencies gained as investors unwound defensive positions. The Australian dollar was a major beneficiary, rising 5.0% against the greenback, as widening spreads and expectations for further rate hikes by the RBA support the currency.

(GTM AUS page 65)