Global Market Strategist

In Brief

- AI investment came under the microscope as markets questioned whether big spending by U.S. tech giants will deliver returns, even as earnings growth stayed solid.

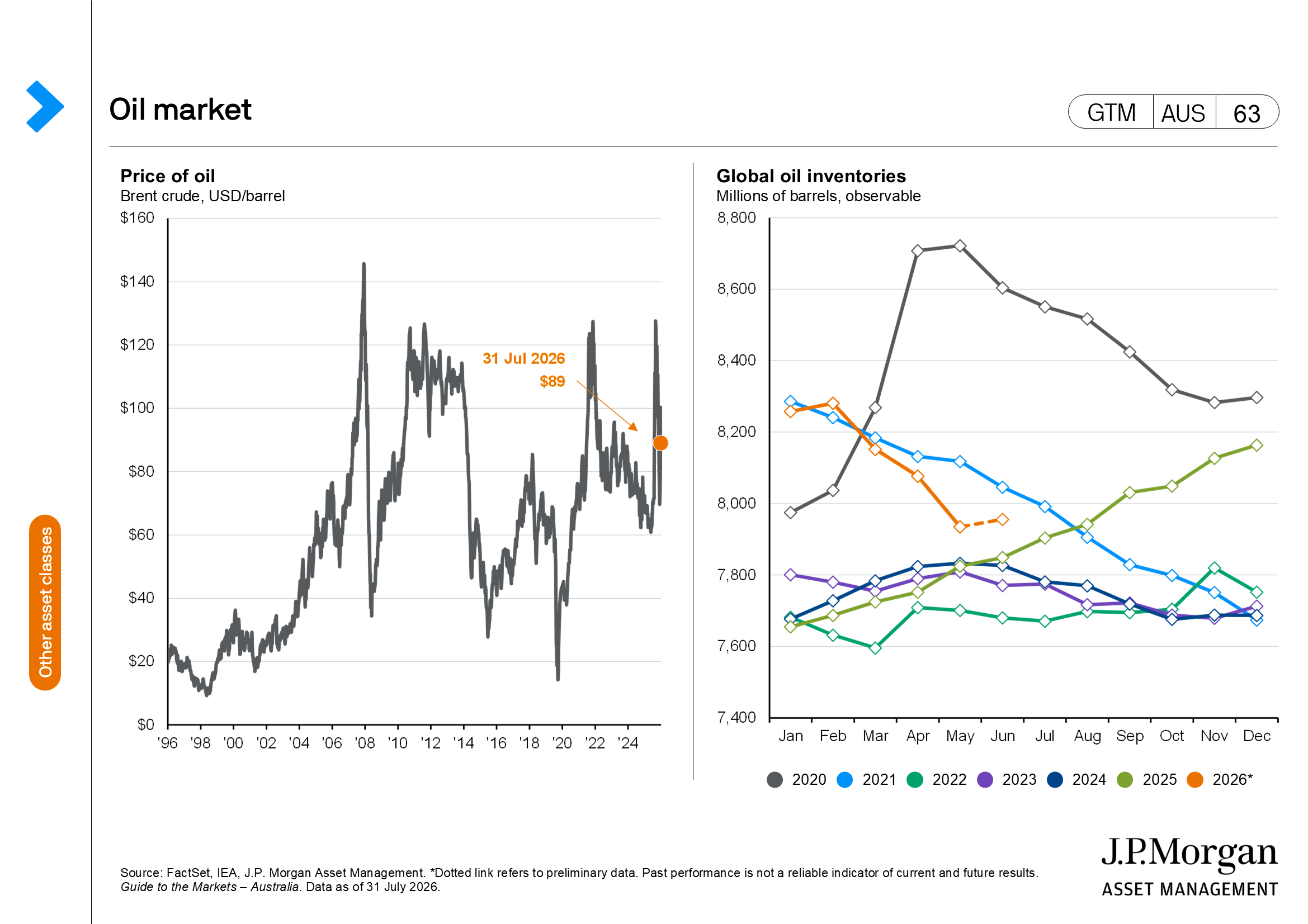

- Renewed conflict in the Middle East sent oil prices higher and kept markets on edge, with central banks and bond yields reacting to energy-driven inflation risks.

- Australia quietly outperformed, with steady rates and easing inflation supporting local equities, while investors globally became more selective and broadened their focus beyond tech.

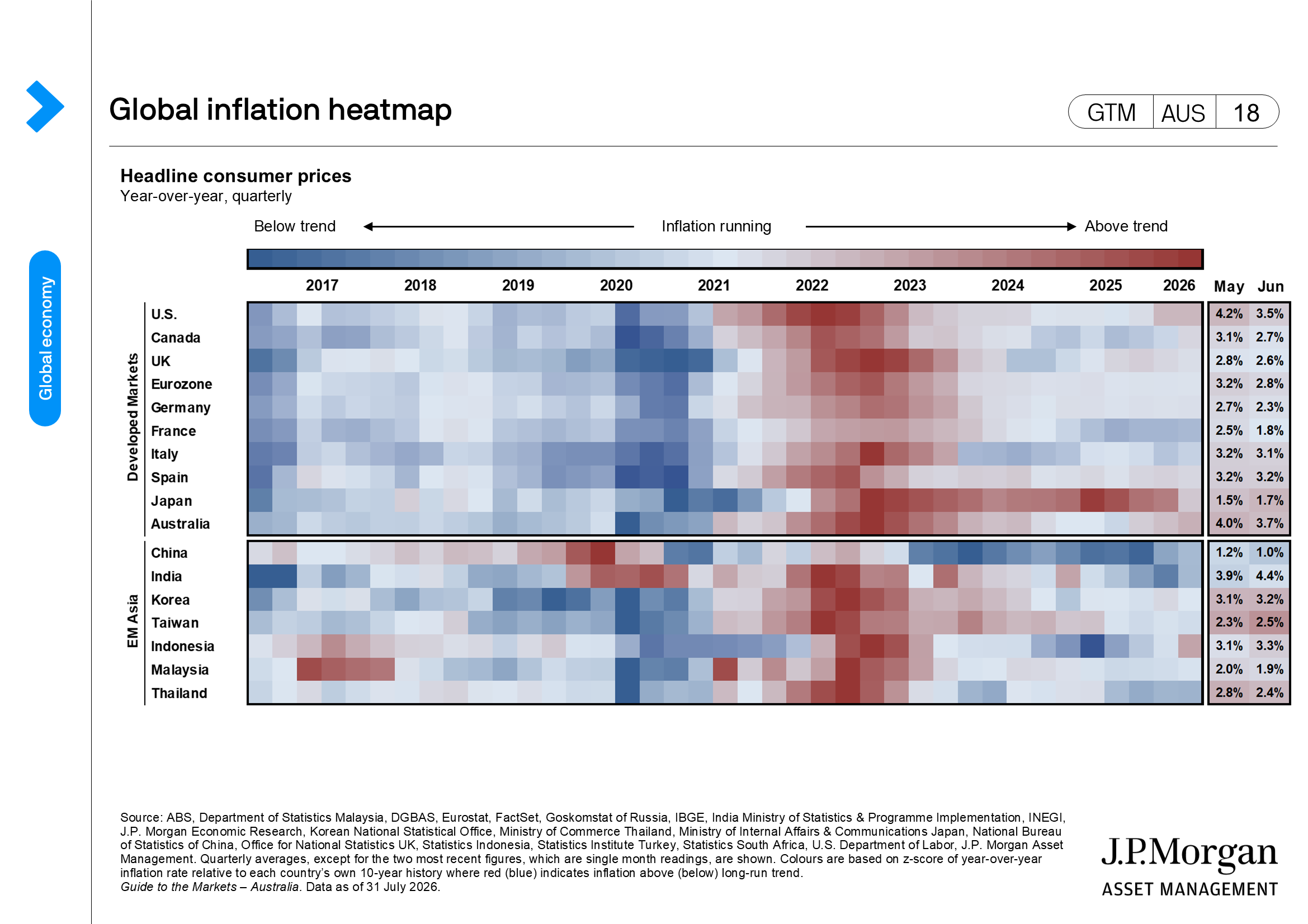

A resurgence in the Middle East hostilities and a sharp reset in artificial intelligence (AI)-related valuations tested market resilience in July. Developed-market central banks remained patient as June inflation figures around the globe were softer, but the prospect of energy-driven inflation meant that markets continued to price in policy tightening by year-end.

AI Capex questioned

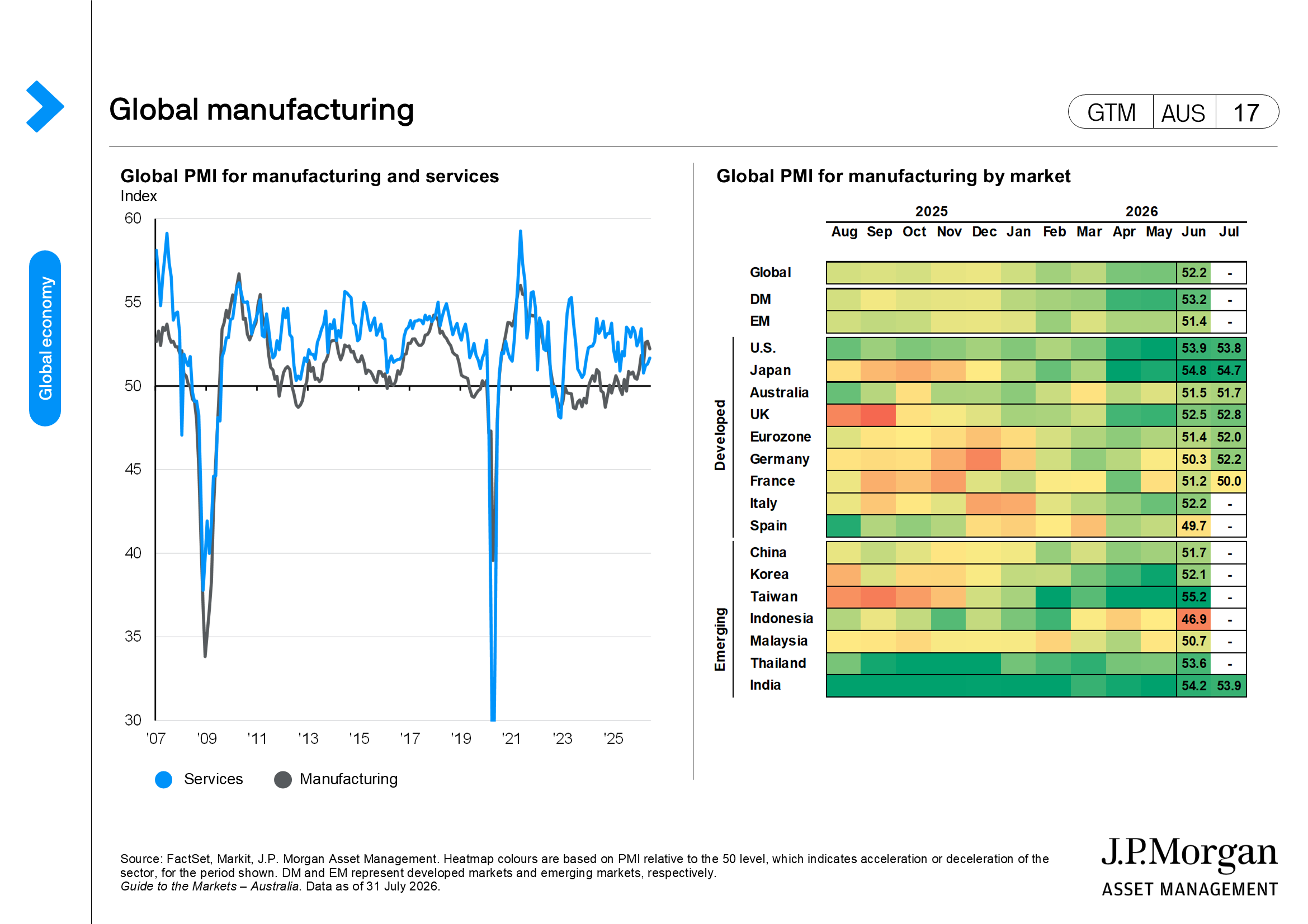

July was a month with two distinct narratives. The first was a quickly moving reassessment of AI capital spending that reverberated up the AI supply chain as markets debated the return on investment in the face of increased competition from open-weight models and rising token costs. As enterprise adoption broadens, investors are paying closer attention to token costs, return on investment, and whether productivity gains justify the scale of spending.

Given the strong performance of semiconductor and memory supplier names earlier in the year, the more recent unwinding in performance could be a move away from crowded positioning and resetting of expectations rather than a structural shift in the AI story.

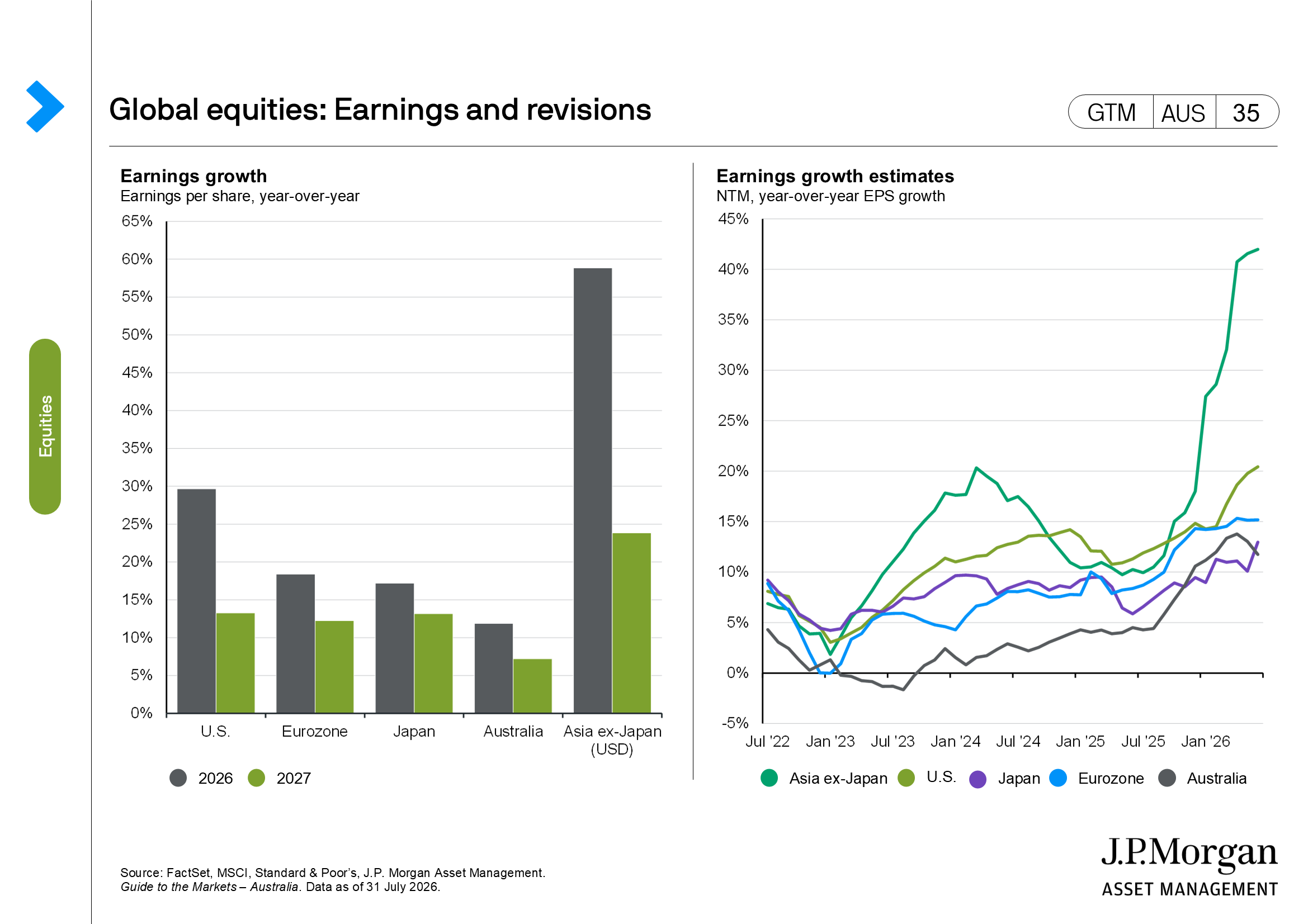

U.S. hyperscalers capex plans will need to be justified not only by future demand, but also by credible evidence of monetisation. Importantly, the fundamentals have not deteriorated to the same degree as sentiment. Second-quarter earnings growth in the U.S. is tracking a healthy 45% year-over-year (y/y), which is higher than the 22% expected when the earnings season began. The strength of earnings growth offsets some of the concern around capex but companies that missed on revenues experienced sharper drawdowns on the day following their earnings announcement than those that missed on earnings.

The Middle East conflict reignited

Geopolitics added a second layer of volatility. The fragile ceasefire that had allowed oil prices to retrace during June broke down in July, effectively closing the Strait of Hormuz again. The price of Brent crude surged again, reaching USD 100/bbl before falling back to USD 88/bbl by the end of July.

Attention is on the ability to traverse the Strait even if another ceasefire is reached and how this will impact normalising flows, insurance costs, inventories and petrochemical logistics. This concern is exacerbated by the disruption of shipping through the Bab El-Mandeb Strait, the southern outlet of the Red Sea.

The renewed energy shock reinforced why bond markets remained so sensitive to the Middle East headlines, given its potential to reverse the disinflation trend of the last few months, at a time when developed-market central banks are trying to assess the need for further policy tightening.

The Fed’s “Family Fight”

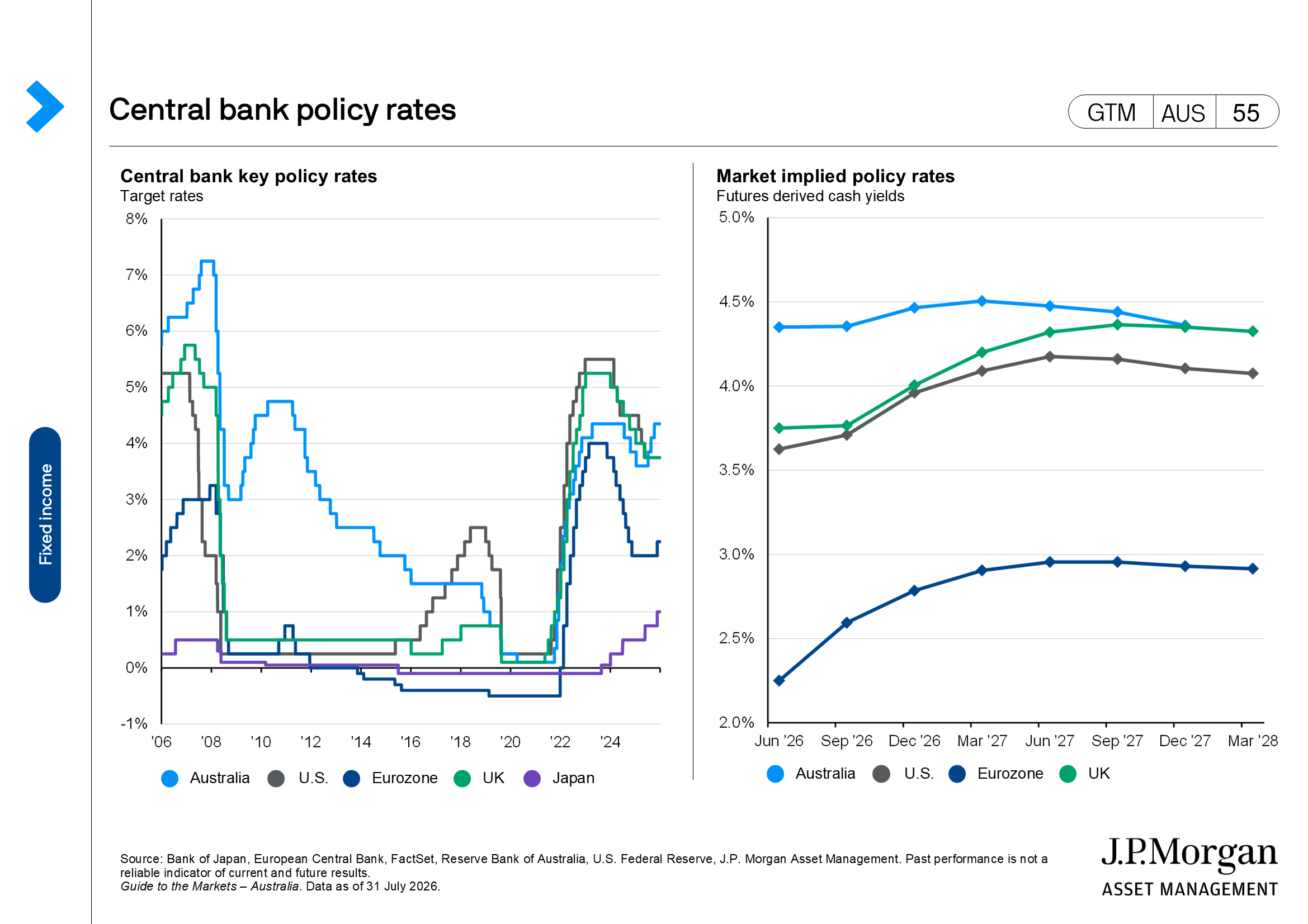

This tension was most evident at the U.S. Federal Reserve’s (Fed’s) July Federal Open Market Committee (FOMC) meeting, as the vote was split, with three regional presidents dissenting in favour of an immediate hike. This left the policy path for the rest of 2026 uncertain, given the next move in rates may reflect a Fed defending its credibility as well as moving inflation back towards the 2% target. If the Fed does tighten later this year, we think it would likely be precautionary rather than the start of an aggressive hiking cycle. In the meantime, bond markets may experience more volatility as investors decipher the policy outlook.

Longer-dated U.S. Treasury yields moved higher after the meeting, extending a month in which fiscal and inflation concerns had already been pressuring the long end of the yield curve.

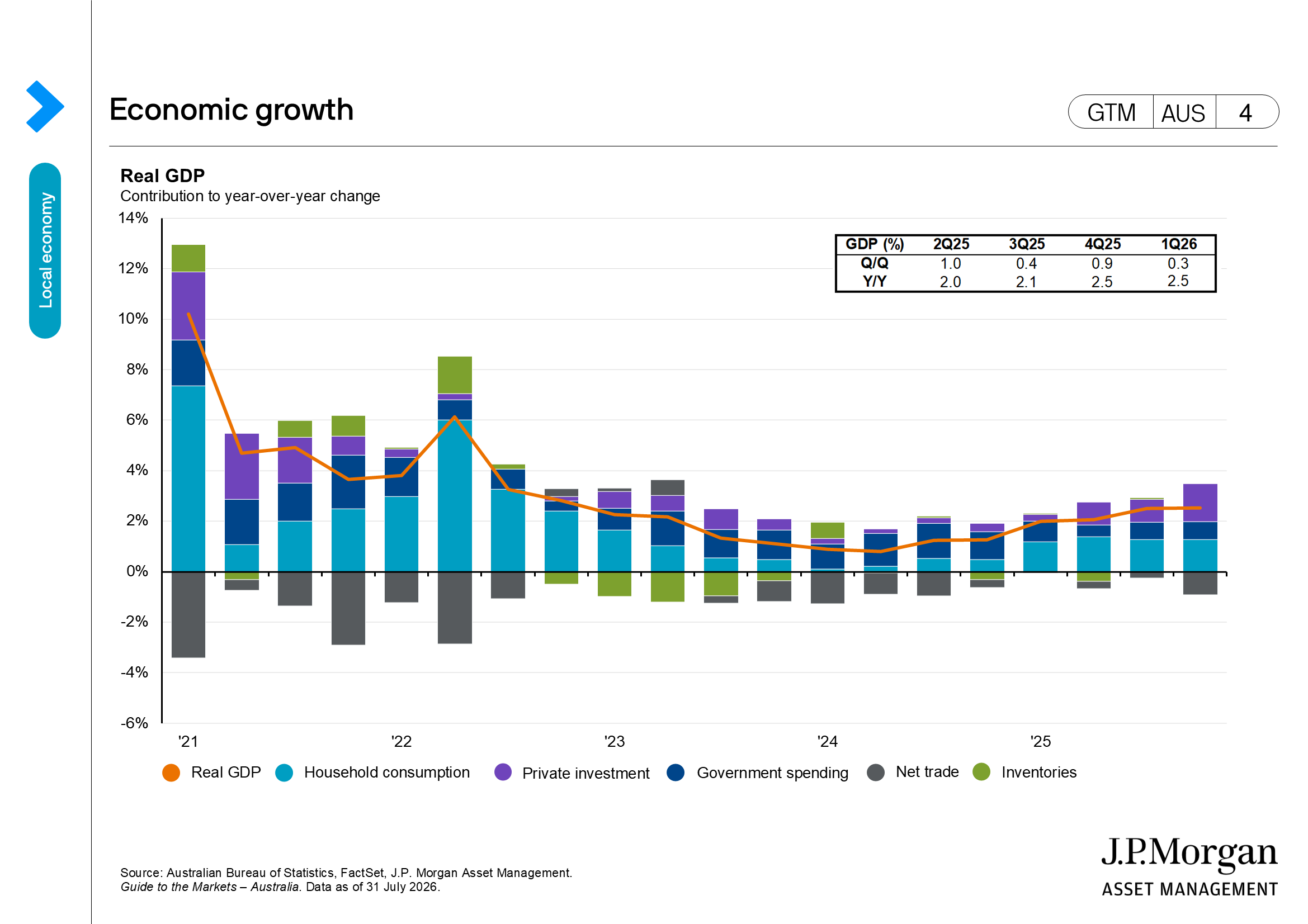

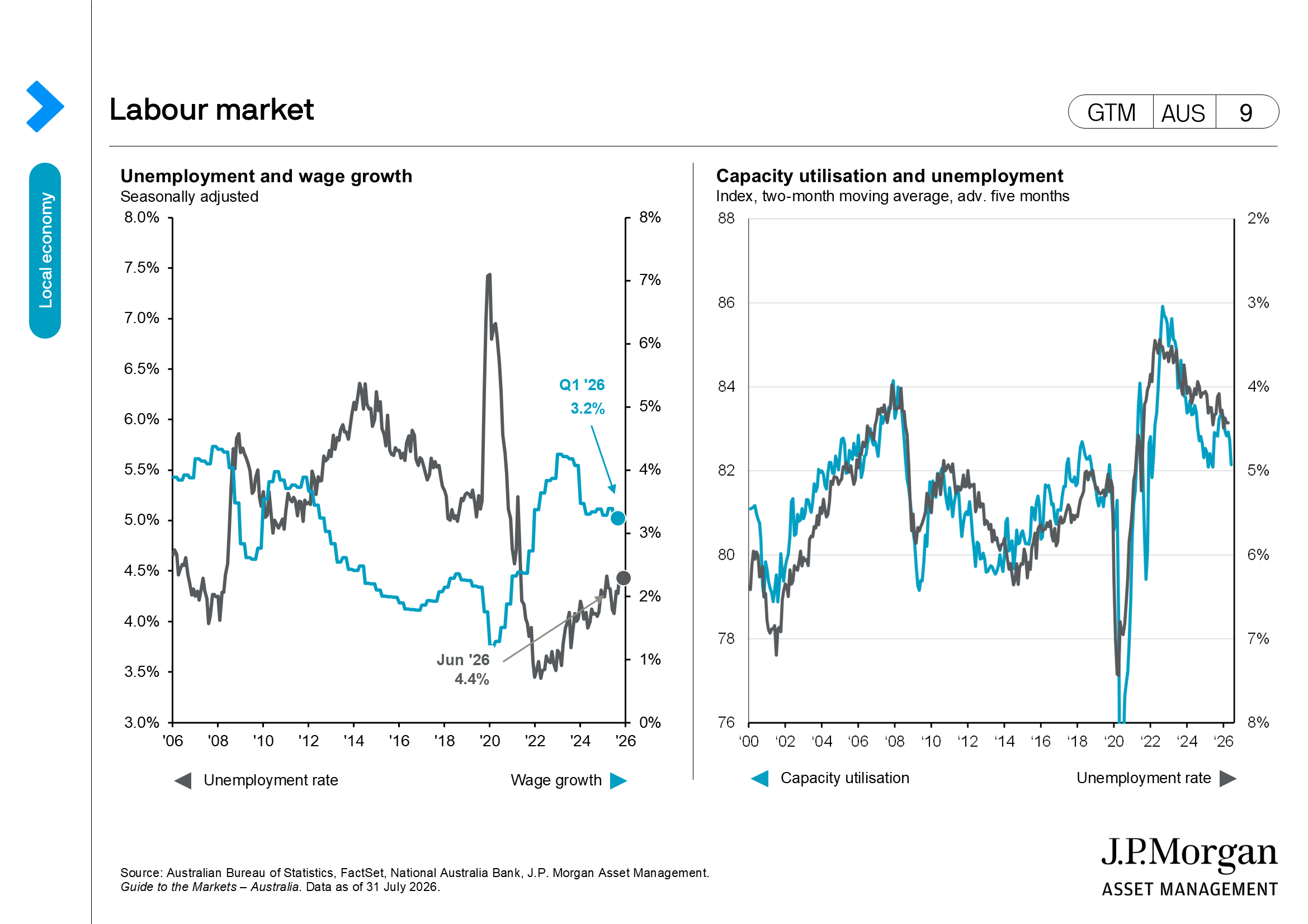

Australia’s quiet outperformance

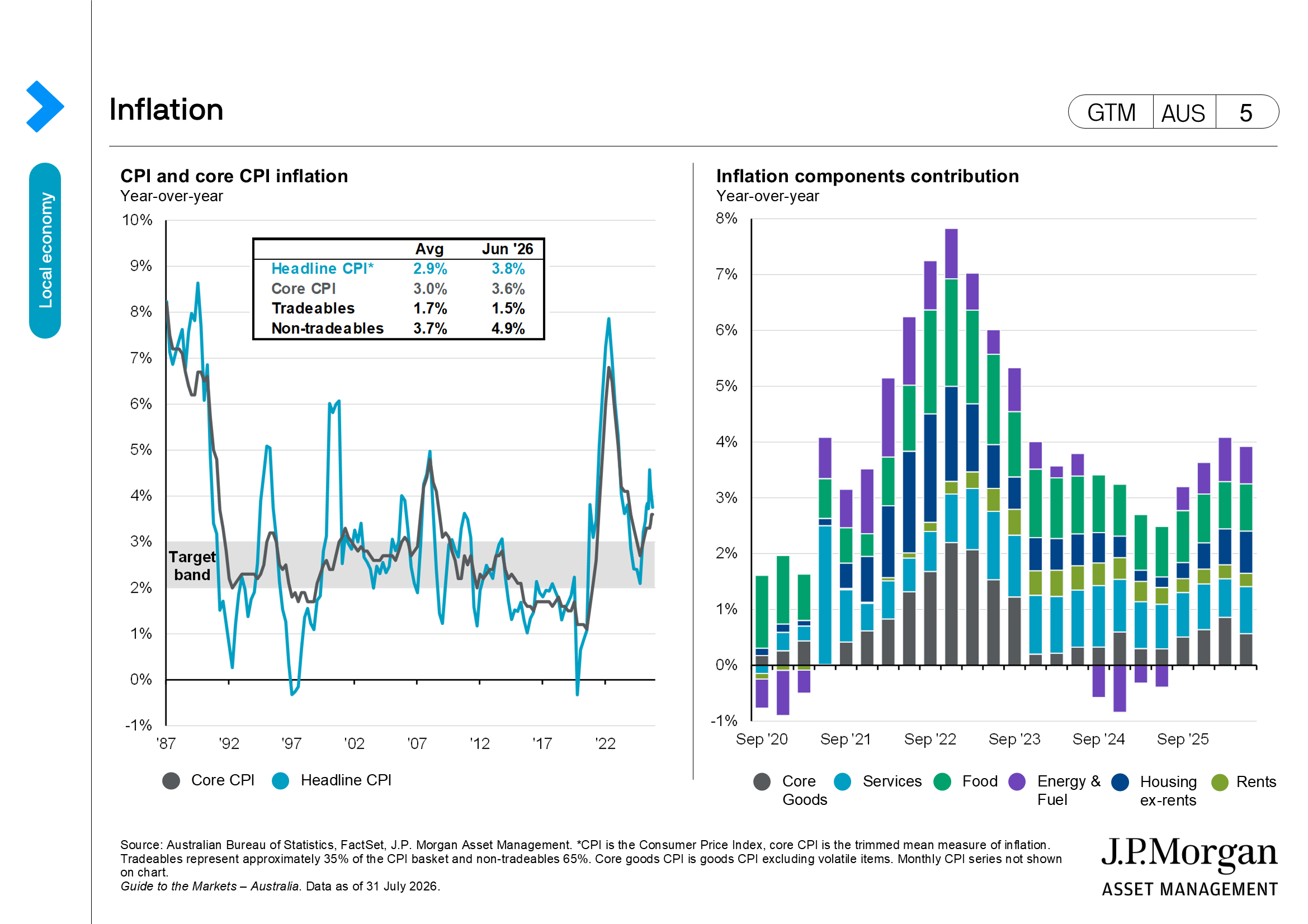

Australia offered a more constructive counterpoint. The Reserve Bank of Australia (RBA) held the cash rate steady in July at 4.35%, and the June quarter inflation data came in below expectations. Headline consumer price index (CPI) eased to 3.8% y/y, while the core rate of inflation was steady at 3.6% y/y. Markets pared back expectations of further rate hikes from the RBA to around 14 basis points (bps) of additional tightening by year-end.

Nonetheless, Australian government bond yields crept higher in sympathy with global moves. Equity investors were rewarded for staying local as the ASX 200 pushed up to a five-month high.

Markets recalibrated

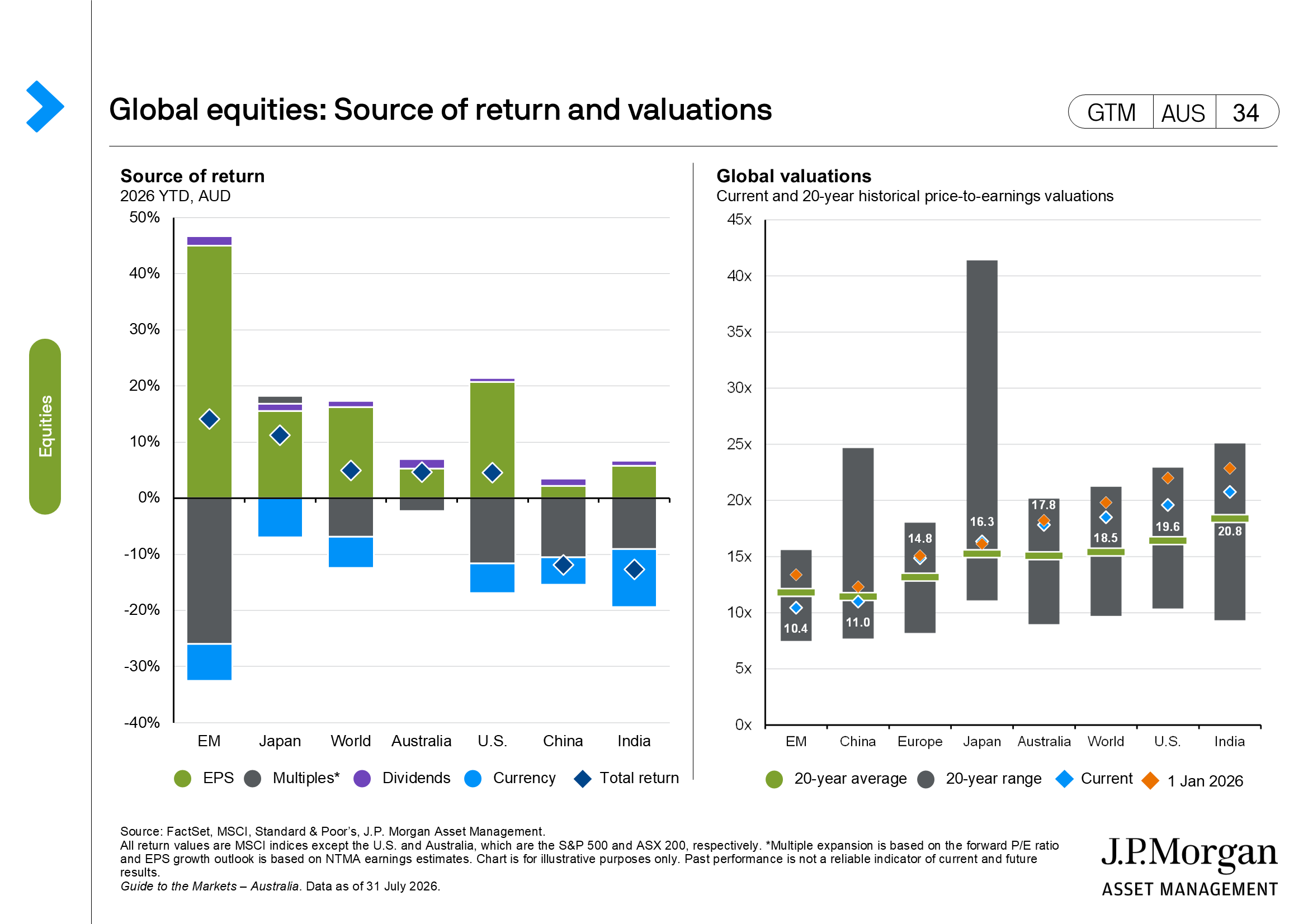

July reinforced two themes that have carried through the year: that earnings are doing more work than multiple expansion in supporting equity markets and geographical diversification.

Fresh concerns over energy supply and the economics of AI have not shaken confidence in the equity market outlook. They have prompted investors to be more selective. Technology and semiconductor giants, especially in South Korea, Taiwan, and the U.S., remain supported by what we expect to be robust demand, but the market is now rewarding companies with pricing power and reliable cash flow over those banking on future investments.

The move away from narrow market leadership is a positive sign, as a steadier global growth outlook lets investors revisit sectors like financials, defence, certain industrials, and Asian markets beyond technology. However, investors will need to monitor risks carefully, higher short-term yields, energy uncertainty, and questions about artificial intelligence profits could all spark sudden shifts.

Global economy

- The July FOMC meeting delivered a hawkish hold, with the Fed leaving rates unchanged as expected but facing three dissents in favour of a 25 bps hike. Chair Warsh emphasised the Fed’s commitment to price stability while avoiding explicit forward guidance, contributing to uncertainty around the reaction function.

- The European Central Bank (ECB) kept the deposit rate unchanged at 2.25% following June’s 25 bps hike, but Lagarde’s press conference leaned hawkish. The Governing Council maintained a meeting-by-meeting approach amid energy-price volatility and the Middle East uncertainty, while removing language on downside growth risks and emphasising that second-round inflation effects still need monitoring. Markets took the “hawkish hold” largely in stride, with limited movement in rates.

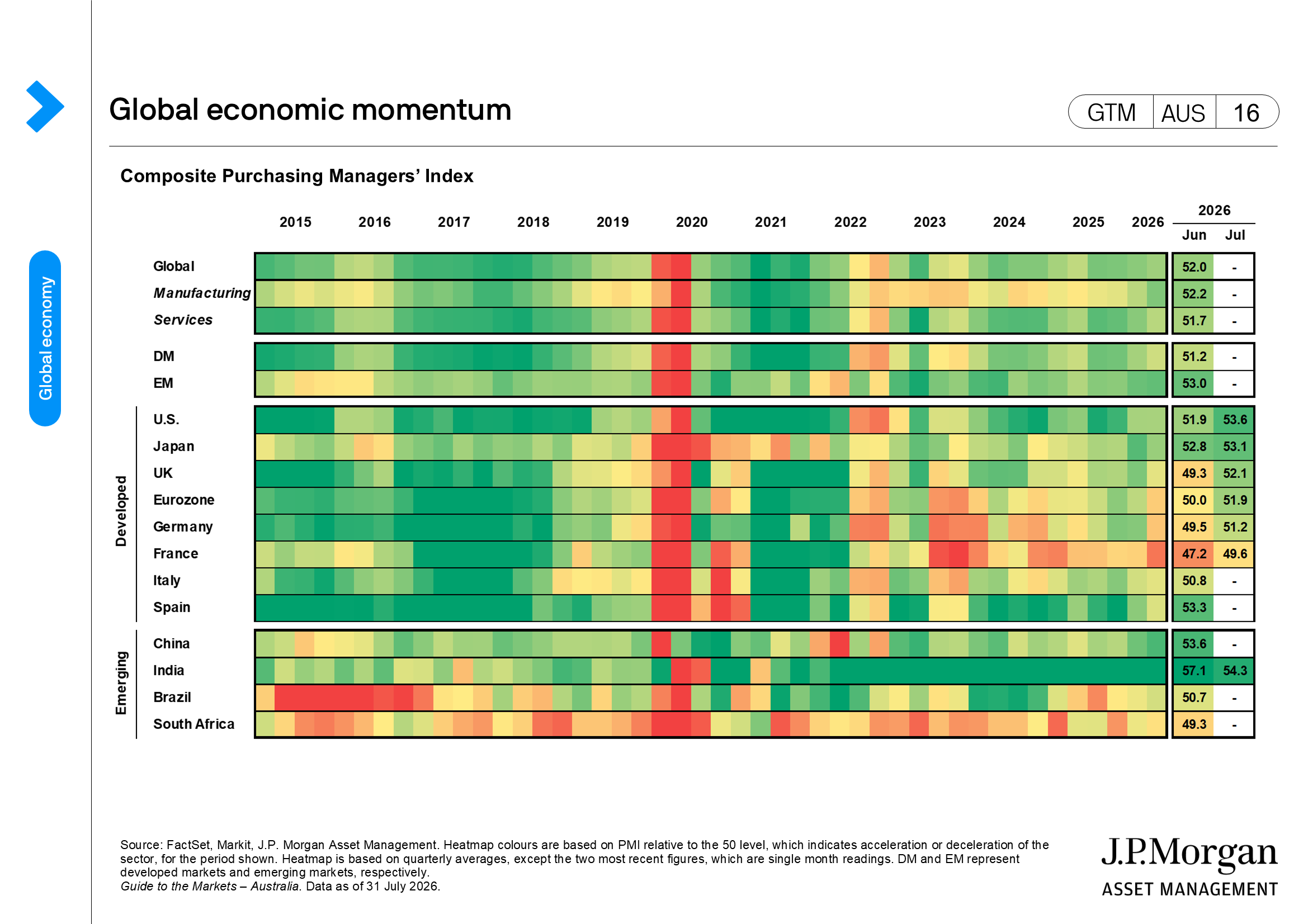

- In China, growth momentum slowed as real gross domestic product (GDP) rose 4.3% y/y in 2Q26, below expectations and down from 5% in 1Q26, though first-half growth of 4.7% remained within the government’s 4.5%–5.0% target range. Exports and high-tech manufacturing remained the key supports, helped by strong demand for AI hardware, semiconductors and advanced equipment, while domestic demand stayed weak amid soft retail sales, contracting investment and continued property-sector pressure. The GDP miss is likely to increase expectations for targeted policy support at the July Politburo meeting rather than a broad-based stimulus package.

- The Bank of Japan (BoJ) kept its policy rate on hold at 1%, as widely expected, but delivered a hawkish signal on normalisation, with an 8-1 vote and one member favouring a move to 1.25%; it also flagged the risk that underlying inflation could potentially hit its 2% target. Takaichi continued to vow for advancing the USD 2.3trillion stimulus plan with a temporary food sales-tax cut. Authorities also conducted currency intervention to support the Japanese yen (JPY), pulling the currency away from a four-decade low.

Equities

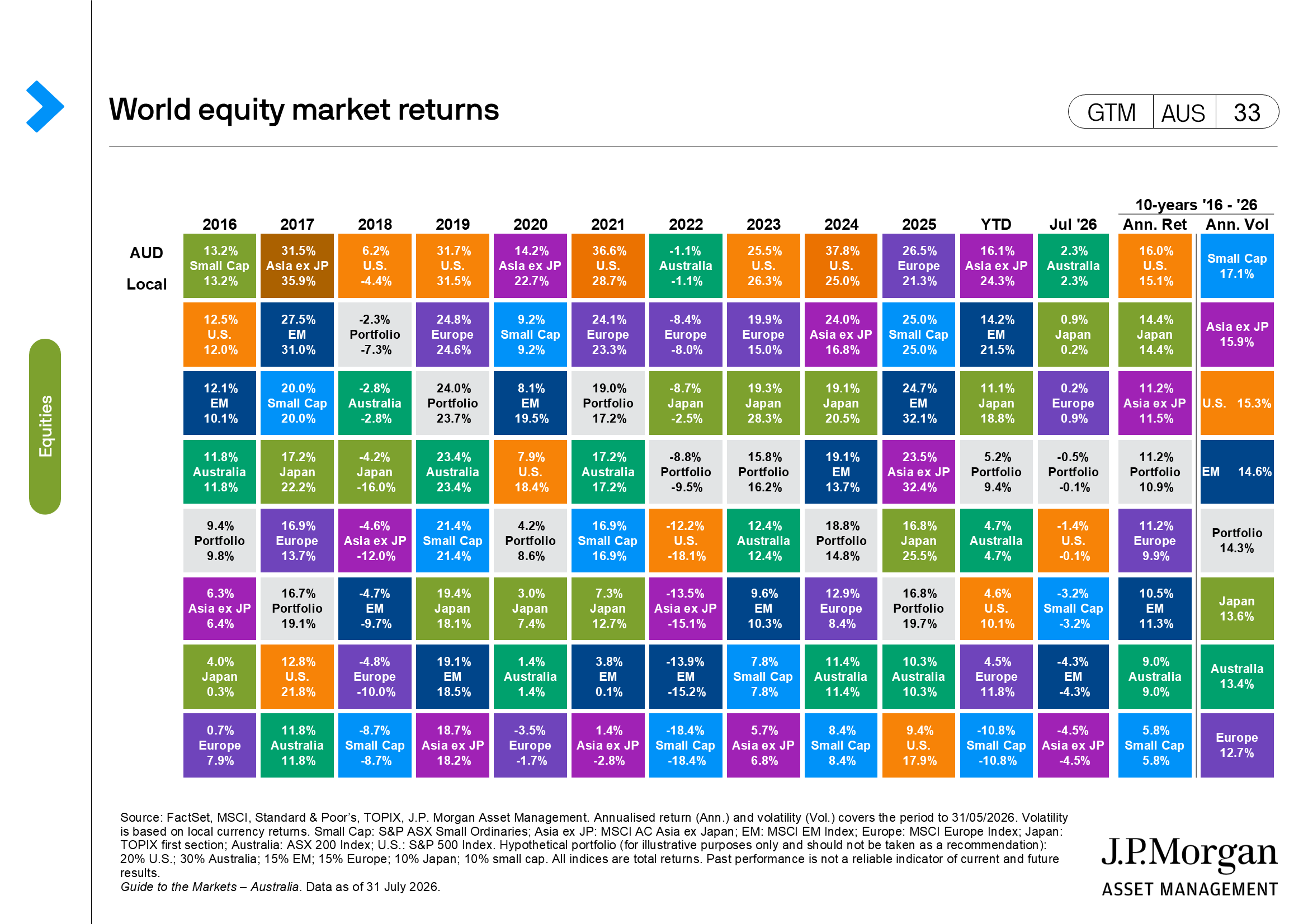

- MSCI World was flat in July, with the S&P 500 and Nasdaq both down for a second straight month, though the equal-weight S&P 500 outperformed the cap-weighted index as market breadth improved. AI remained the key under-the-surface theme, but leadership rotated sharply as semiconductors and memory stocks sold off on concerns around AI capex returns, valuations, and crowded positioning, while energy, financials, real estate, healthcare and staples outperformed.

- Asian equities declined in July, with the MSCI Asia Pacific ex Japan index lower, though performance was highly dispersed across the region. South Korea and Taiwan lagged amid extreme volatility in AI- and chip-linked shares, while Australia, Singapore and parts of Southeast Asia outperformed, supported by strength in energy, financials, local currencies and more resilient domestic sentiment.

- Australian equities advanced in July, with the ASX 200 higher for a fourth straight month and ending near all-time highs after a late-month breakout from a narrow trading range. Energy and financials led performance, supported by higher oil prices, strength in refiners and major banks, while the information technology and industrials sectors were softer.

- Greater China was mixed, with Hong Kong rallying strongly as sentiment improved and investors rotated into the market, while mainland technology-heavy benchmarks sold off on concerns over valuation, positioning and AI-related crowding. Broader China macro data remained soft, with weaker consumption, property pressure and disappointing investment offsetting resilience in industrial production and exports.

- Japan was mixed in July, with the Nikkei declining sharply while the broader Topix posted a modest gain, reflecting rotation away from more growth- and technology-sensitive areas. Macro policy remained a key focus as the BoJ held rates steady but kept the door open to further normalisation, while JPY weakness prompted direct FX intervention and fiscal-policy headlines added upward pressure to bond yields.

Fixed income

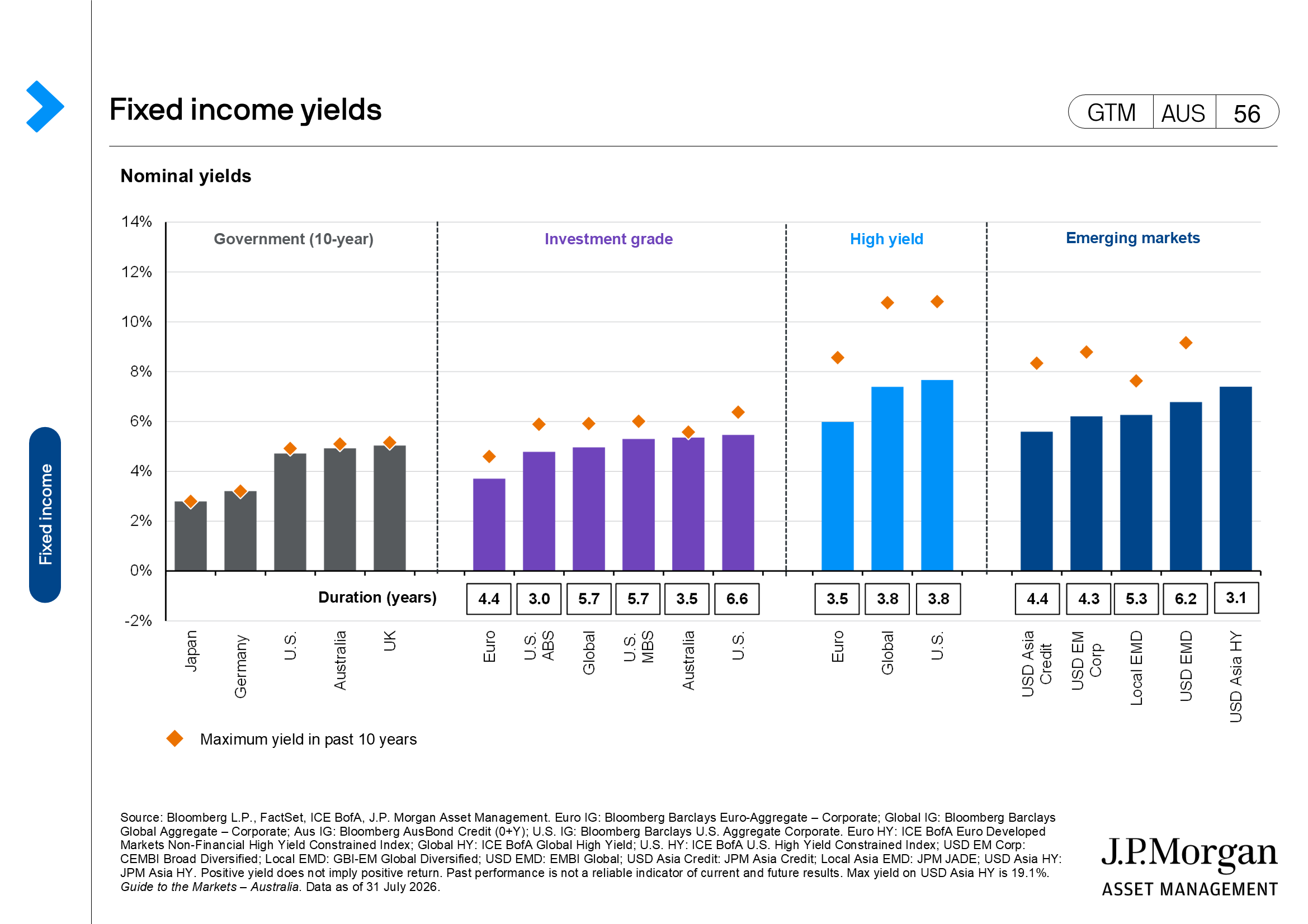

- The U.S. Treasury (UST) yield curve bear-steepened in July, with 2-year and 30-year yields up 12 bps and 32 bps, respectively. Amid a sharp increase in energy prices and more hawkish Fed policy expectations, these have weighed on the short-end of the curve. And additional pressure was placed on long-end yield, which reflects market questions around the Fed’s credibility to commit to its inflation mandate, following Warsh’s lack of forward guidance at the press conference. With Overnight Index Swap (OIS) markets already pricing in a full rate hike by this year end, the risk of further tightening is now pushed into next year with 53 bps of rate increase priced in by June 2027.

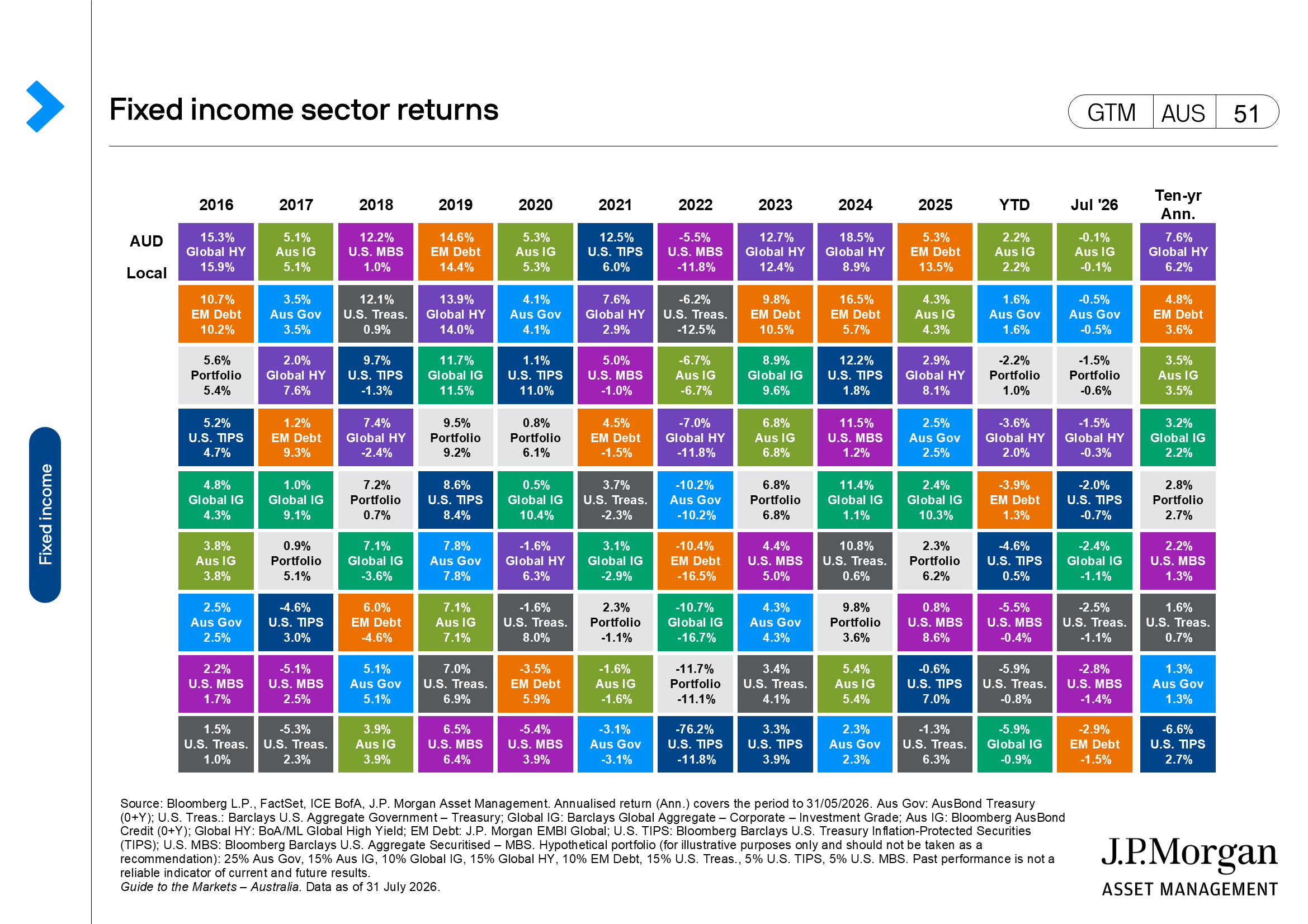

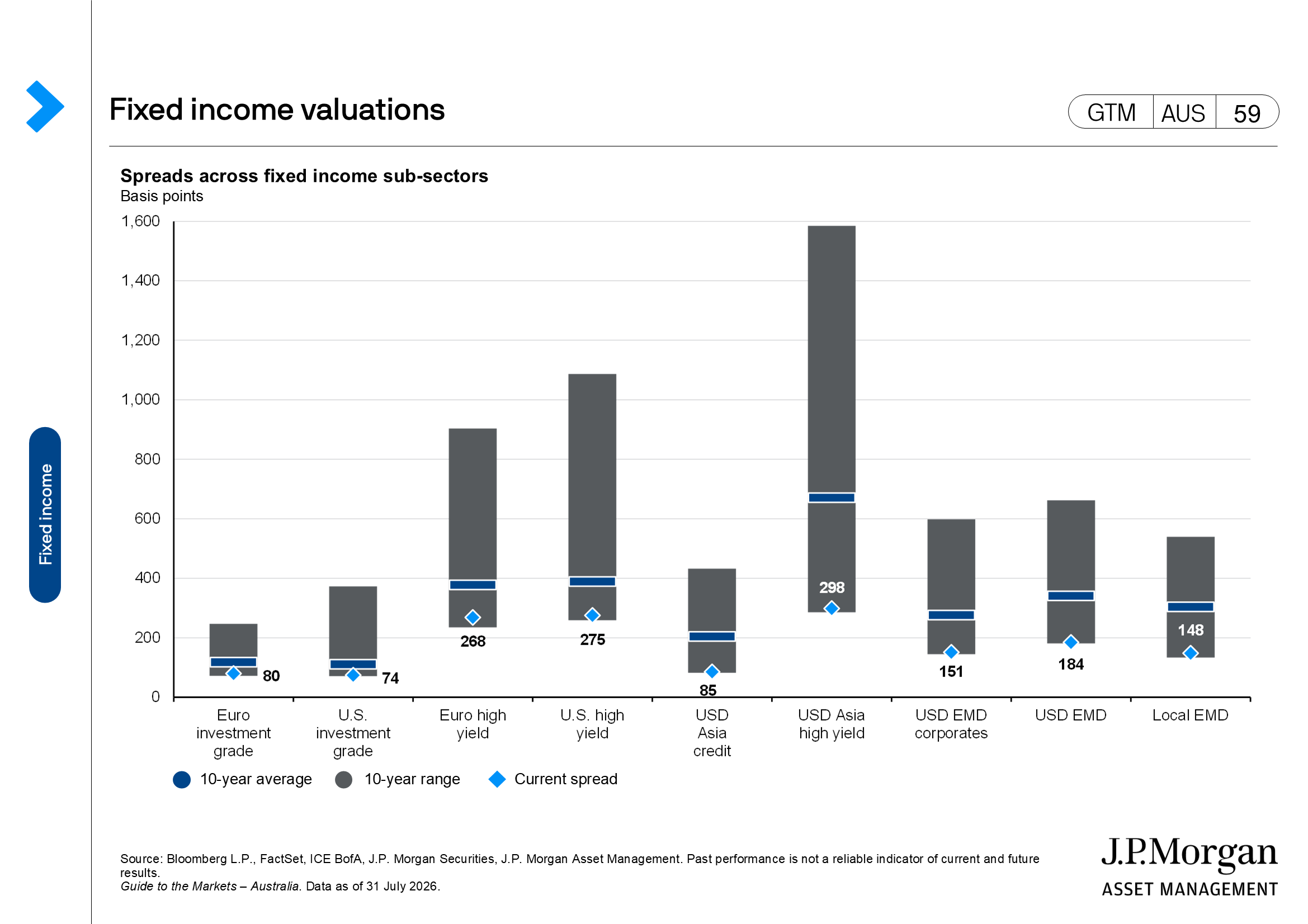

- Credit spreads nudged higher toward late July, as increased bond issuance from tech hyperscalers weighed on top of market’s hawkish pricing, although the impact remains manageable as markets focus on robust balance sheet fundamentals. As such, global investment grade and high yield spreads marginally widened by 2 bps and 7 bps, respectively, but remains near the tight end of historical range.

Alternatives

- According to PitchBook data, the number of global private equity deals in 2Q26 is estimated to have increased to 5,672, up from 5,552 in the last quarter. Momentum on deal value stalled, however, with deal activity estimated to amount to USD 420billion in 2Q26, lower than USD 544billion in the last quarter. Exit activity in global private equity also slowed, with USD 275billion across 948 exits estimated in 2Q26, down from USD 343billion across 1,000 exits in the last quarter.

- As for the U.S. middle market, the J.P. Morgan Private Assets Index-Middle Market recorded a 17.5% trailing 12-month return as of June, with revenue growth, net debt change and multiple expansion contributing 10.6%, -2.4% and 9.0%, respectively.

- Based on the KBRA DLD Direct Lending index, the trailing 12-month default rate was flat over June at 3.9% excluding non-accruals and 6.1% including non-accruals on a par-weighted basis, while yield to maturity rose 7 bps to 9.14%.

Other financial assets

- Oil prices moved sharply as a renewed U.S.–Iran confrontation in July again disrupted traffic through the Strait of Hormuz, reversing the brief relief from the mid-June MOU and shifting market focus back to execution risk to physical flows, insurance costs, inventories and petrochemical logistics.

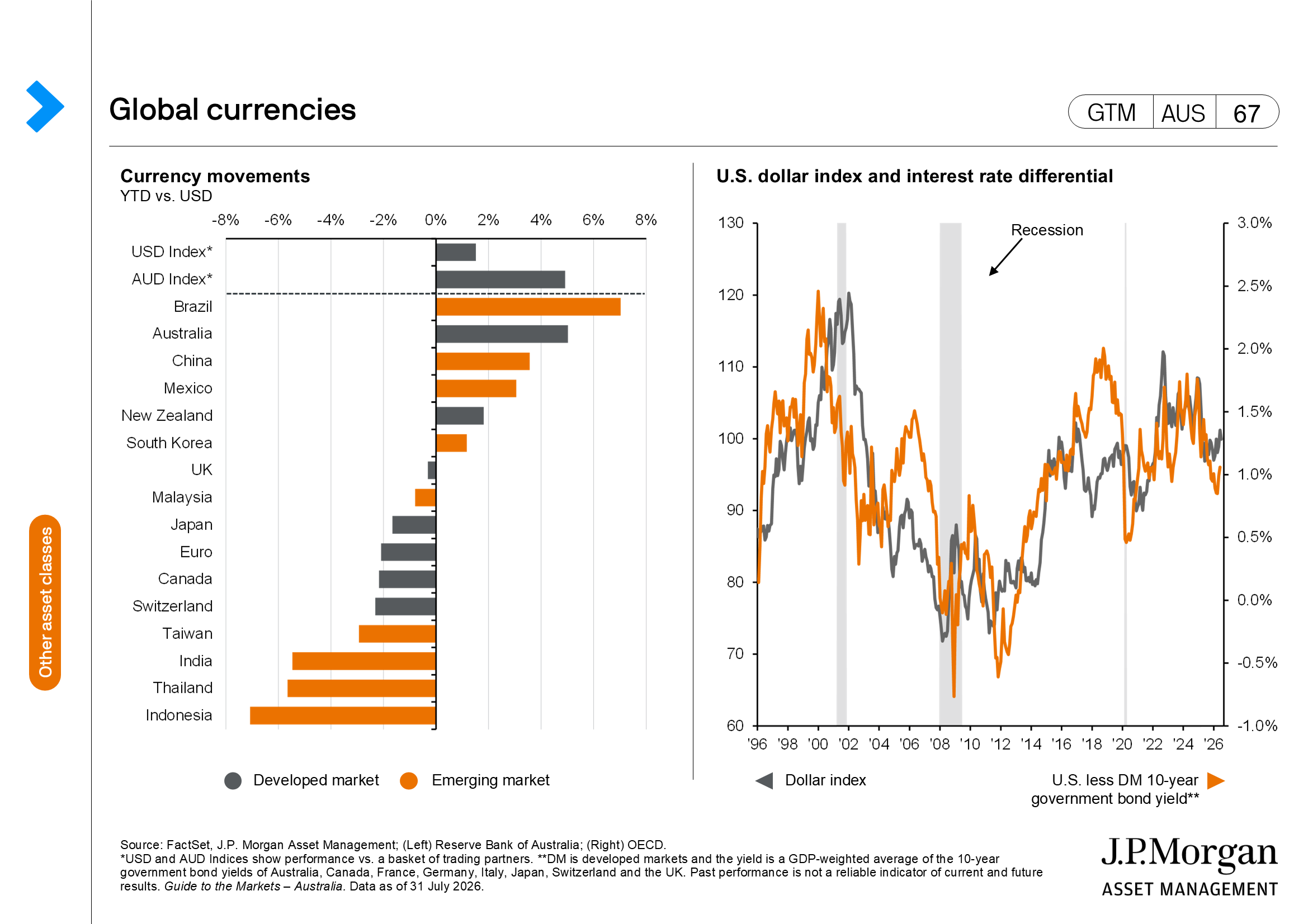

- U.S. dollar momentum reversed over the month, as the FOMC meeting raised renewed questions around the Fed’s credibility and commitment to its inflation targets, with the DXY index down 1.3% to 99.9 by July-end. As for other developed market currencies, most gained over the month, with the EUR up 0.6% and the GBP up 1.4%, while the CHF fell 0.3%. Asian currencies similarly gained, with the JPY most notably up 2.1% on the intervention efforts by both governments and the KRW up 8.8% on a hawkish Bank of Korea and domestic risk-off flows. The CNY also gained 0.6% over the month in accordance with the People’s Bank of China’s (PBoC’s) fixing, while the INR fell 0.8% and marked one of the weakest currencies in Asia.