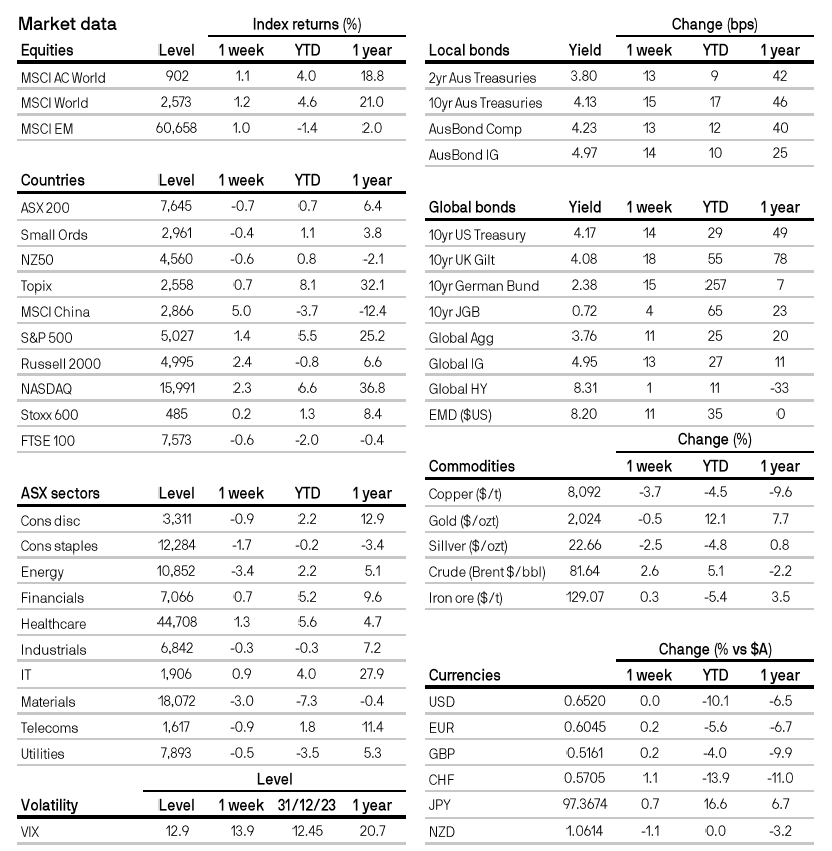

Week in review

- RBA keeps rates on hold at 4.35%

- Chinese inflation falls to -0.8% y/y

- NZ unemployment rate rises to 4.0%

Week ahead

- Australia consumer and business confidence

- Australia unemployment rate

- U.S. CPI inflation

Thought of the week

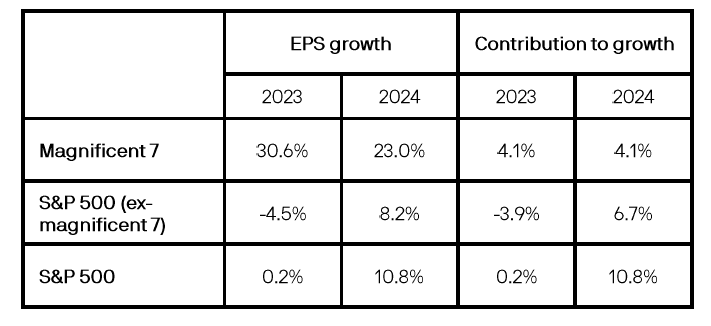

A big question for investors in the U.S. equity market is whether the rally will broaden out beyond the mega-cap ‘magnificent seven’. The ‘magnificent seven’ were responsible for nearly all the earnings growth and return on the S&P 500 in 2023. However, repeating the 31% profit growth these companies experienced last year will be a tough ask and the bar to surprise the market is now higher. Meanwhile the hurdle for the remaining 493 companies is lower. These companies could see a turn in earnings growth from negative to positive, contributing more to the 11% consensus earnings estimate for 2024. That double-digit earnings growth could be at risk as the economy slows moderating expected equity returns in 2024. However, quality companies can still make a profit in a weak economy and investors should diversify their exposure in U.S. large cap as they seek out higher quality earnings.

Magnificent seven, better than the rest in 2023

Year-over-year earnings growth and contribution to expected earnings

Source: FactSet, J.P. Morgan Asset Management. Data reflect most recently available as of 09/02/24.

All returns in local currency unless otherwise stated.

Equity price levels and returns: Levels are prices and returns represent total returns for stated period.

Bond yields and returns: Yields are yield to maturity for government bonds and yield to worst for corporate bonds. All returns represent total returns. AusBond Comp is the AusBond Composite 0+ Yr, AusBond IG is the AusBond Credit 0+ Yr both provided by Bloomberg.

Currencies: All cross rates are against the Australian dollar. An appreciation of the foreign currency against the Australian dollar would be positive and a depreciation of the foreign currency against the Australian dollar would be negative.

0903c02a82467ab5

For more information, please call or email us. You can also contact your J.P. Morgan representative.

1800 576 100 (Application enquiries)