Week in review

- ECB leaves cash rate at 4.5%

- European and U.S composite PMI

- U.S. economy expands by 3.3% q/q saar in 4Q 2023

Week ahead

- U.S. Federal Reserve meeting

- Australia retail sales

- Australia CPI inflation for 4Q 2023

Thought of the week

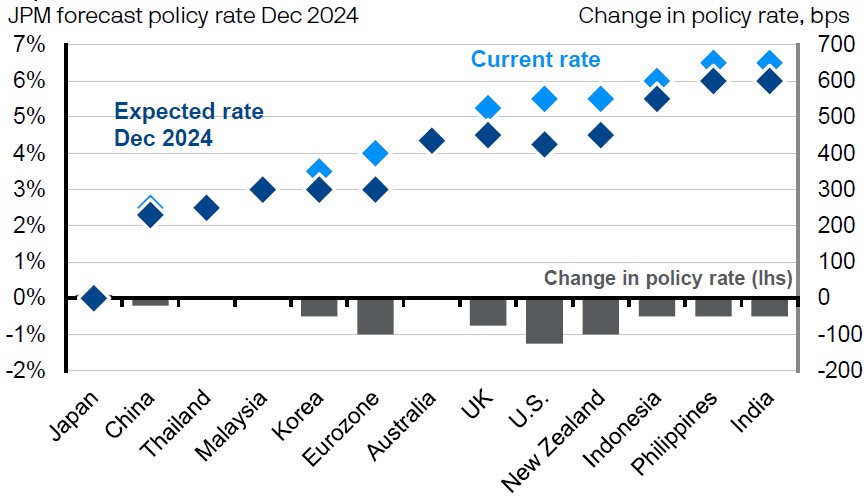

This week the U.S. Federal Reserve (Fed) will meet, as will the Bank of England. Both are likely to provide a similar narrative to the European Central Bank (ECB) from last week and rebuff market expectations for early rate cuts until there is more convincing evidence that inflation is sustainably returning to target. Globally inflation pressures continue to ease, but labour markets are only slowly loosening and unemployment rates remain low. Meanwhile, the recent shipping disruptions could add to the potentially more challenging ‘last mile’ in the fight on inflation. However, outside of energy the shipping disruption inflationary impact should be muted. Rate cuts are coming, so what difference does a few months make? A lot. Market pricing of earlier cuts suggest a faster pace of disinflation along with stable growth. Later cuts could mean stubborn inflation and a weaker growth outlook or even recession creating a very different market dynamic.

Expectations for interest rates in 2024

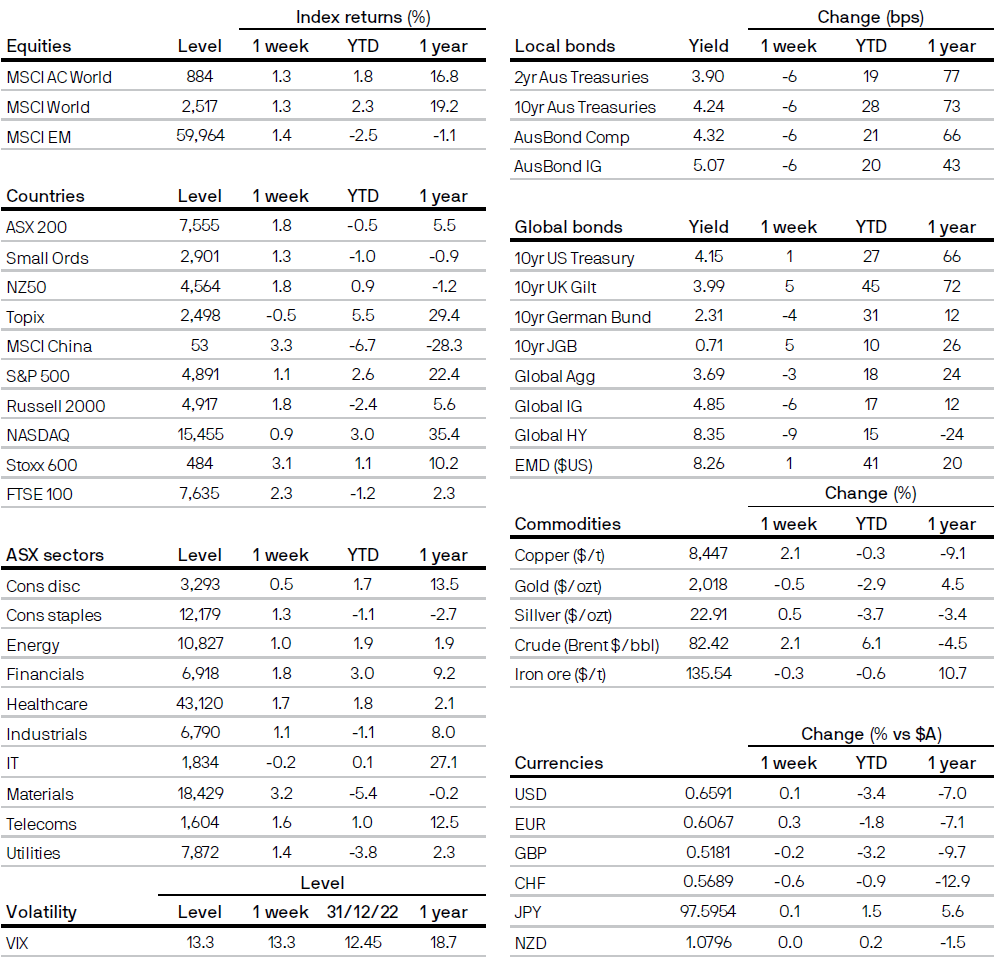

Market data

Source: FactSet, J.P. Morgan Economic Research, J.P. Morgan Asset Management. Data reflect most recently available as of 26/01/24.

All returns in local currency unless otherwise stated.

Equity price levels and returns: Levels are prices and returns represent total returns for stated period.

Bond yields and returns: Yields are yield to maturity for government bonds and yield to worst for corporate bonds. All returns represent total returns. AusBond Comp is the AusBond Composite 0+ Yr, AusBond IG is the AusBond Credit 0+ Yr both provided by Bloomberg.

Currencies: All cross rates are against the Australian dollar. An appreciation of the foreign currency against the Australian dollar would be positive and a depreciation of the foreign currency against the Australian dollar would be negative.

0903c02a82467ab5

For more information, please call or email us. You can also contact your J.P. Morgan representative.

1800 576 100 (Application enquiries)