Week in review

- Australia unemployment rate unchanged at 3.5%

- Chinese 2Q real GDP 6.3% y/y

- U.S. retails sales 0.2% m/m

Week ahead

- Australia 2Q CPI inflation

- Eurozone and US composite PMIs

- U.S. Federal Reserve policy meeting

Thought of the week

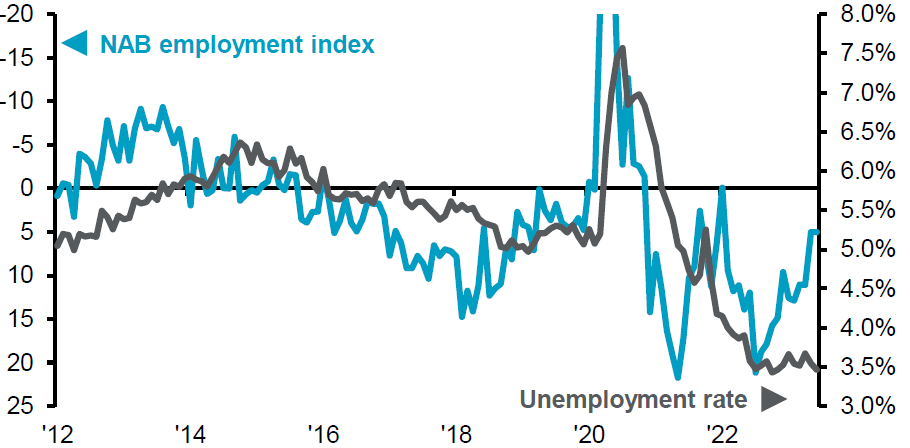

Disinflationary pressures may be building around the world as more countries publish softer inflation figures. The latest is the UK where inflation came down to 7.9% y/y and lower than had been expected by the market and the Bank of England. This week will be Australia’s turn as the second quarter inflation figure are released. The monthly inflation figures for Australia are not perfect but suggest that price pressures are normalizing. As inflation falls the question being asked is whether this can continue as aggregate demand remains elevated and labour markets are yet to experience any softness? The unemployment report for Australia last week showed that supply is running higher than demand as the economy added another 32,600 jobs and the unemployment rate held steady at 3.5%. The tightness remains despite the forward-looking indicators for labour demand moving in the other direction. The still tight labour market in Australia and inflation above the RBA’s target suggest another rate hike in August seems likely, unless the inflation figure is well below what is expected. An August rate hike would coincide with a new set of economic forecasts from the RBA.

Australian unemployment rate diverging from forward indicators

Unemployment rate and the NAB employment index (inverted)

Source: ABS, FactSet, NAB, J.P. Morgan Asset Management. Data reflect most recently available as of 21/07/23.

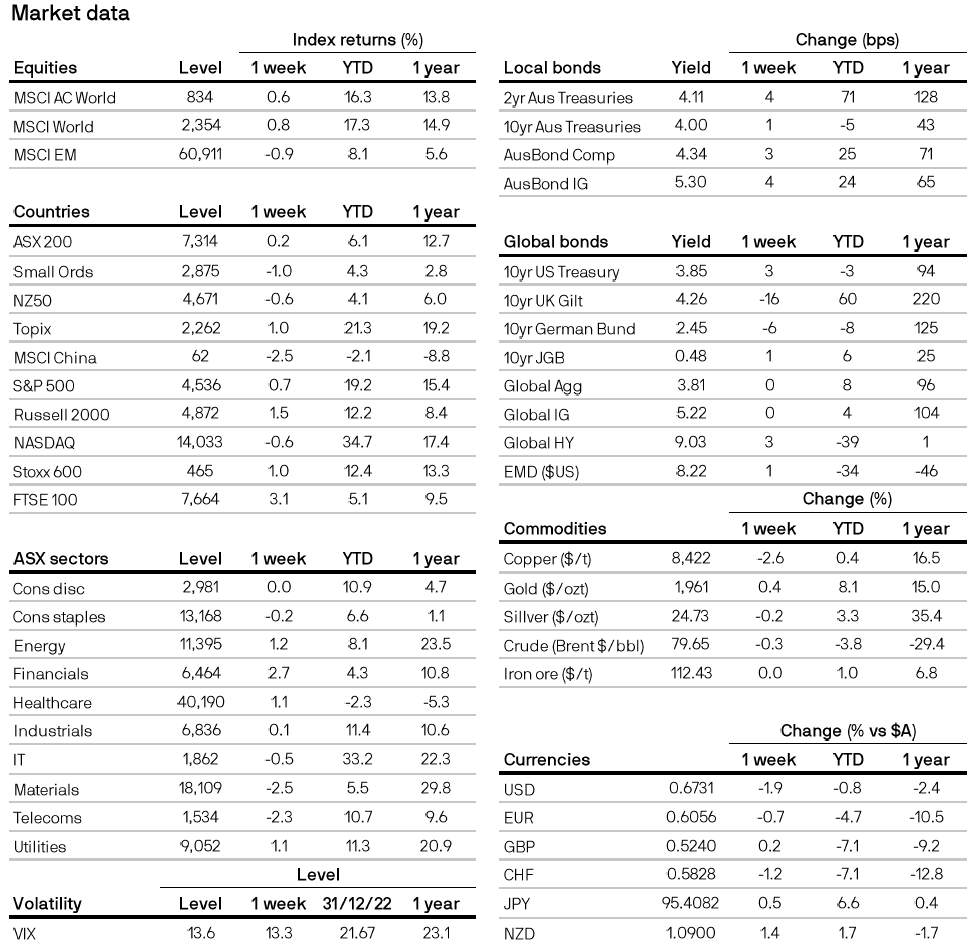

All returns in local currency unless otherwise stated.

Equity price levels and returns: Levels are prices and returns represent total returns for stated period.

Bond yields and returns: Yields are yield to maturity for government bonds and yield to worst for corporate bonds. All returns represent total returns. AusBond Comp is the AusBond Composite 0+ Yr, AusBond IG is the AusBond Credit 0+ Yr both provided by Bloomberg.

Currencies: All cross rates are against the Australian dollar. An appreciation of the foreign currency against the Australian dollar would be positive and a depreciation of the foreign currency against the Australian dollar would be negative.

0903c02a82467ab5

For more information, please call or email us. You can also contact your J.P. Morgan representative.

1800 576 100 (Application enquiries)