Green bonds: Is doing good compatible with doing well in fixed income?

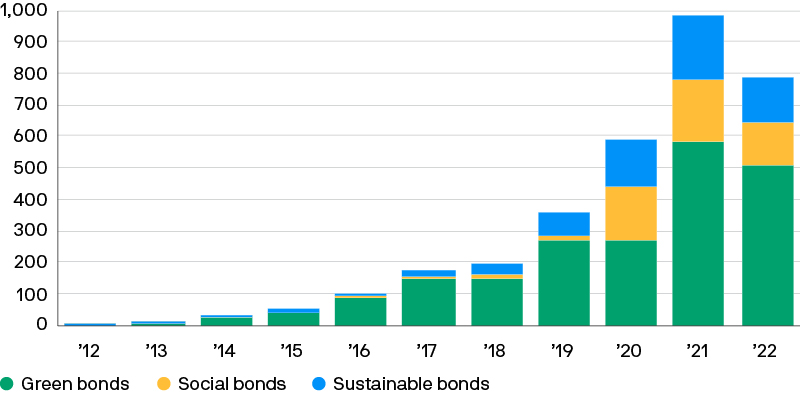

Since the issuance of the first green bond by the European Investment Bank in 2007, the green bonds market has grown substantially (Exhibit 1), with green bond issuance now exceeding $500bn per year.

Exhibit 1: Global sustainable, social and green bond issuance

USD billions

Source: Refinitiv Eikon, J.P. Morgan Asset Management. Green bonds are those where 100% of the net bond proceeds are allocated to green projects. Social bonds are those where the bond proceeds have a focus on delivering positive social outcomes. Sustainable bonds are those where the bond proceeds are directed to a mix of both green and social projects or if the bond coupon/ characteristics can vary based on achieving predefined sustainability targets. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2022.

This growth should accelerate further in the coming years, as the proceeds from green bonds are used to finance the energy transition. Forecasts for the amount of global investment needed to reach Net Zero stand at several trillion dollars per year by 2030.1

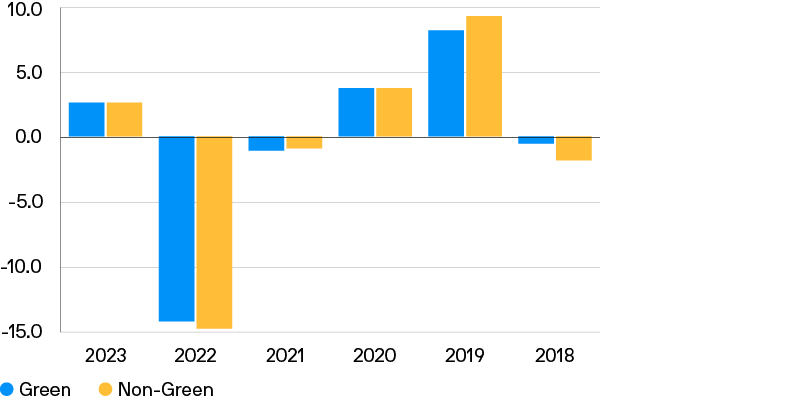

A substantial part of these climate-related investments could be financed through the issuance of green bonds, as these generally offer slightly lower financing costs, or a “greenium” (Exhibit 2), compared to traditional bonds, thanks to the strong demand for this type of instrument.

However, while this greenium is a financial advantage for issuers of green bonds, the benefits for investors is less clear. Why, one may wonder, would investors accept a lower yield on their investment for reasons beyond a regulatory requirement or non-financial incentive? The answer, we believe, lies in the strong fundamental, quantitative and technical factors that underpin demand for green bonds.

Exhibit 2: Spread between green and traditional corporate bonds

Basis points

Source: Barclays Research, J.P. Morgan Asset Management. Data shown is for a Barclays Research custom universe of green and non-green investment-grade credits, matched by issuer, currency, seniority and maturity. The universe consists of 160 pairs, 99 EUR denominated and 61 USD denominated. Spread difference is measured using the option- adjusted spread. Past performance is not a reliable indicator of current and future results. Guide to the Markets - Europe. Data as of 31 December 2022.

1. Fundamentals: Green bonds are more defensive than traditional bonds and have similar duration-adjusted returns

When comparing the Bloomberg Global Aggregate Index and the Bloomberg MSCI Global Green Bond Index, we observe that although the green bond index has a higher credit quality, it has underperformed and has been more volatile than its non-green counterpart since its inception.

However, this discrepancy is mainly due to its higher duration (7.2 vs. 6.8) which weighed on the relative performance of the green bond index as yields rose in 2022. When we look at the security level, by comparing bond pairs (green and non-green) that have similar features2, it appears that green bonds have similar duration-adjusted returns (Exhibit 3) but with a lower spread volatility (Exhibit 4) and better downside protection.

Exhibit 3: Duration adjusted returns

%

Exhibit 4: Non-Green less Green Spread Difference

Basis points

Sources: Bloomberg, J.P.Morgan Asset Management. Data as at January 2023.

2. Quantitative: The greenium is not as negative as investors may think

The greenium is a well-known feature of green bonds but its size is generally limited. The Federal Reserve3 has recently estimated that “on average, dollar- and euro-denominated green corporate bonds have a primary market credit spread that is 8 basis points lower compared to conventional”.

In addition, following the yield increase in 2022, the greenium’s share of total yield has decreased substantially, from almost 10%4 of the green bond yield at the start of 2022 to around 2% today.

Finally, because the greenium is a function of the supply and demand imbalances for green bonds, it is not stable over time and across regions, thereby offering alpha opportunities for active investors (Exhibit 2).

3. Technicals: The green bonds market allows investors to benefit from strong flows into sustainable investment solutions

Demand for green bonds should remain elevated, amid increased investor appetite for sustainable securities that offer transparency over the use of proceeds. Environmental, social and governance (ESG) funds, such as those categorised as Article 9 under the European Union’s Sustainable Finance Disclosure Regulation (SFDR), have been gaining traction since the SFDR was introduced. Article 9 funds, which have an explicit sustainable objective and only allocate to sustainable investments, are not obliged to invest in green bonds instead of traditional bonds. However, green bonds can be more attractive for Article 9 funds because they provide greater transparency over the use of proceeds.

On top of investor demand, central banks could also potentially contribute to an increase in demand for green bonds. Some central banks see climate change as part of their mandate, with the European Central Bank (ECB) going so far as to announce that its “corporate bond holdings will be tilted towards issuers with better climate performance”5. The ECB has also recognised the important role that green bonds will play in funding the climate transition and could therefore give preferential treatment to green bonds in its primary market bidding behaviour, subject to certain conditions.6

Conclusion

We believe green bonds will continue to benefit from strong fundamental, quantitative and technical factors.

The greenium is generally seen as a “financial cost” for investors. However, it has historically been relatively limited, while its share of total yield has decreased substantially recently. In addition, the greenium is not stable over time and across regions, and so offers alpha opportunities for active investors.

Moreover, green bonds have historically been proven to be more defensive than traditional bonds, as evidenced by lower duration-adjusted volatility, and have similar duration-adjusted returns.

The demand for green bonds should remain elevated, amid increased investor appetite for sustainable securities that offer transparency over the use of proceeds, and ongoing regulator and central bank encouragement.

However, to fully harness the potential of green bonds, active management is essential. Given the absence of a global definition of what a green bond is, the ability to analyse the use of the proceeds is key to avoid greenwashing and regulatory risks.

1 International Energy Agency (IEA) World Energy Investment 2022 report. 2030e is based on the IEA’s net zero by 2050 scenario.

2 Issuer, capital structure, currency, rating and maturity.

3 https://www.federalreserve.gov/econres/ifdp/files/ifdp1346.pdf

4 Based on a theoretical Greenium of 8 basis points as % of Yield to worst of the Bloomberg MSCI Global Green Bond Index.

5 https://www.ecb.europa.eu/press/pr/date/2022/html/ecb.pr220704~4f48a72462.en.html

6 https://www.ecb.europa.eu/mopo/implement/app/html/ecb.cspp_climate_change-faq.en.html

094z233001161515