Week in review

- U.S. Federal Reserve kept policy rate unchanged at 3.50%-3.75%

- Bank of Japan kept policy rate unchanged at 1.00%

- China YTD industrial profits slowed to 18.7% y/y in June

Week ahead

- U.S. July nonfarm payrolls

- China July trade balance

- Japan June wage growth

Thought of the week

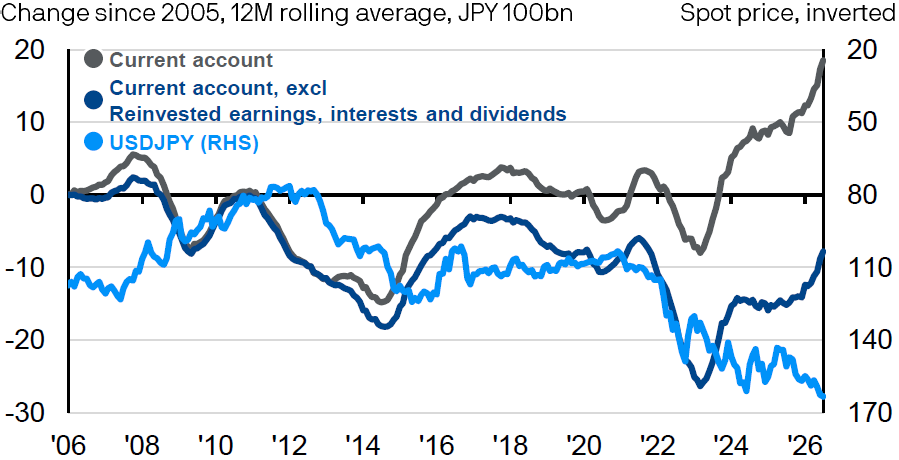

The Japanese Yen remains exceptionally cheap relative to history. Interest rate differentials, fiscal concerns and speculative carry trades are often cited as the main drivers, while last week’s BoJ meeting also reinforced market focus on whether policy remains “behind the curve.” But another less discussed force may be adding structural pressure. Japan’s current account surplus is at record highs, and such surpluses would normally translate to greater demand for the currency. In the JPY’s case, however, that relationship appears increasingly diluted. Years of overseas expansion and investment mean a larger share of Japan’s primary income is now earned abroad. And recent JPY weakness may further reduce the incentive to repatriate those earnings, encouraging reinvestment overseas instead. This limits the incremental JPY demand and can reinforce a feedback loop of continued weakness. So, while the recent MoF’s intervention may offer some near-term support, it remains to see if the JPY can return to a sustainable strengthening path.

USDJPY and Japan’s current account

Source: FactSet, Bank of Japan, Ministry of Finance, J.P. Morgan Asset Management. Data reflect most recently available as of 31/07/2026.

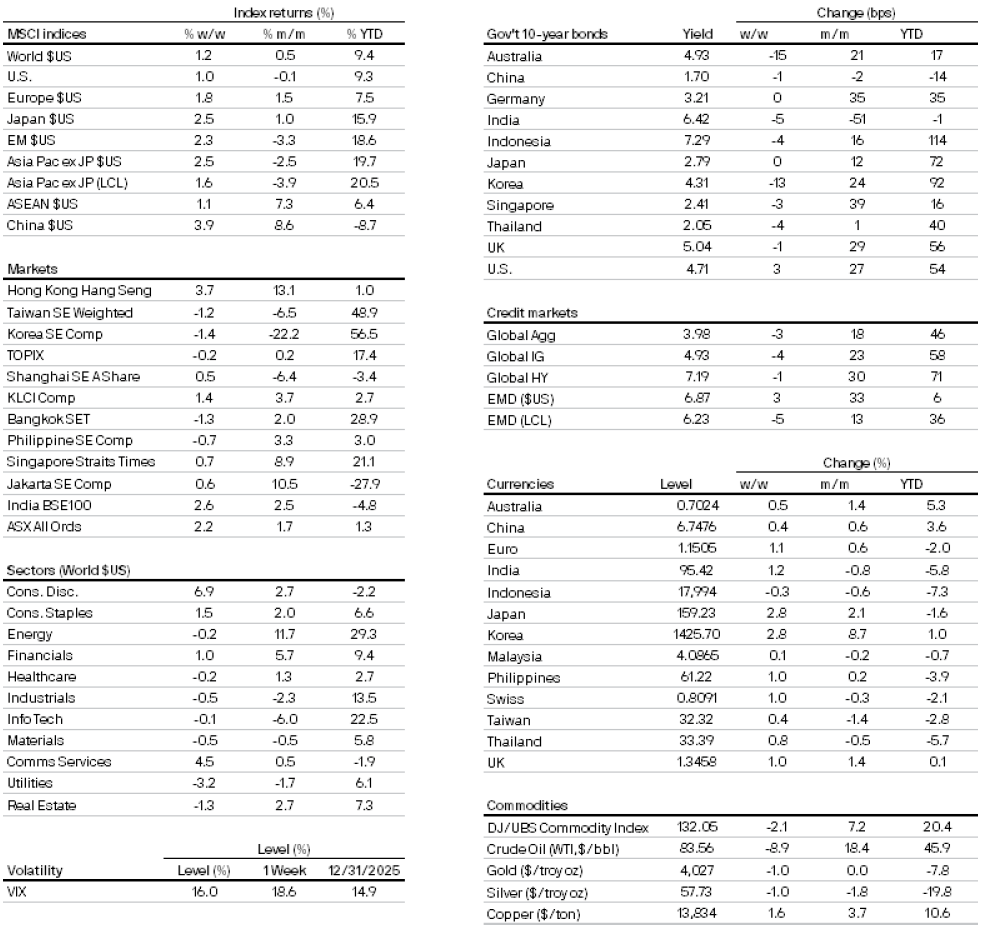

Market data

300a4900-f9d9-11e8-839f-fe2ee17e7f12

All returns in local currency unless stated otherwise.

Currencies’ return are based on foreign currencies per U.S. dollar. An appreciation of the foreign currency against the U.S. dollar would be positive and a depreciation of the foreign currency against the U.S. dollar would be negative.