European Union (EU) governments and business leaders believe that one of the best ways to achieve their sustainability goals is to encourage capital to flow towards efforts that promote and enable a more sustainable economy. Many investors also support this objective, but often lack enough information to assess and compare sustainable investment options on the basis of how they are aligned to their investment goals.

The EU Action Plan on Sustainable Finance, which features a series of interlinking regulations designed to encourage sustainable investing, represents a major step towards redirecting capital to the sustainable economy. A key part of the plan is the EU Sustainable Finance Disclosure Regulation (EU SFDR), which came into effect on 10 March 2021. Further regulations are planned, including the EU Taxonomy Regulation, which will establish specific environmental criteria related to economic activities for investment purposes, and is expected to impact the product classifications set out in the EU SFDR, from 1 July 2022. An extended environmental taxonomy and a social taxonomy are expected to follow.

In this Q&A, we look specifically at the EU SFDR, seeking to explain the importance of this wide-reaching regulation and to show how it will impact asset managers, advisers and investors alike.

What is the EU SFDR?

The EU SFDR is a regulation that is designed to make it easier for investors to distinguish and compare between the many sustainable investing strategies that are now available. The EU SFDR aims to help investors by providing more transparency on the degree to which financial products have environmental and/or social characteristics, invest in sustainable investments or have sustainable objectives. This information is now being presented in a more standardised way.

The EU SFDR requires specific firm-level disclosures from asset managers and investment advisers regarding how they address two key considerations: Sustainability Risks and Principal Adverse Impacts. In addition, the EU SFDR aims to help investors to choose between products by classifying funds into three distinct categories, according to the degree to which sustainability is a consideration. Binding investment criteria with specific disclosures are also required for each category. These categories align to Articles 6, 8 and 9 within the EU SFDR and are summarised below:

"Article 6" strategies either integrate environmental, social and governance (ESG) considerations into the investment decision making process, or explain why sustainability risk is not relevant, but do not meet the additional criteria of Article 8 or Article 9 strategies.

“Article 8” strategies promote social and/or environmental characteristics, and may invest in sustainable investments, but do not have sustainable investing as a core objective.

“Article 9” strategies have a sustainable investment objective.

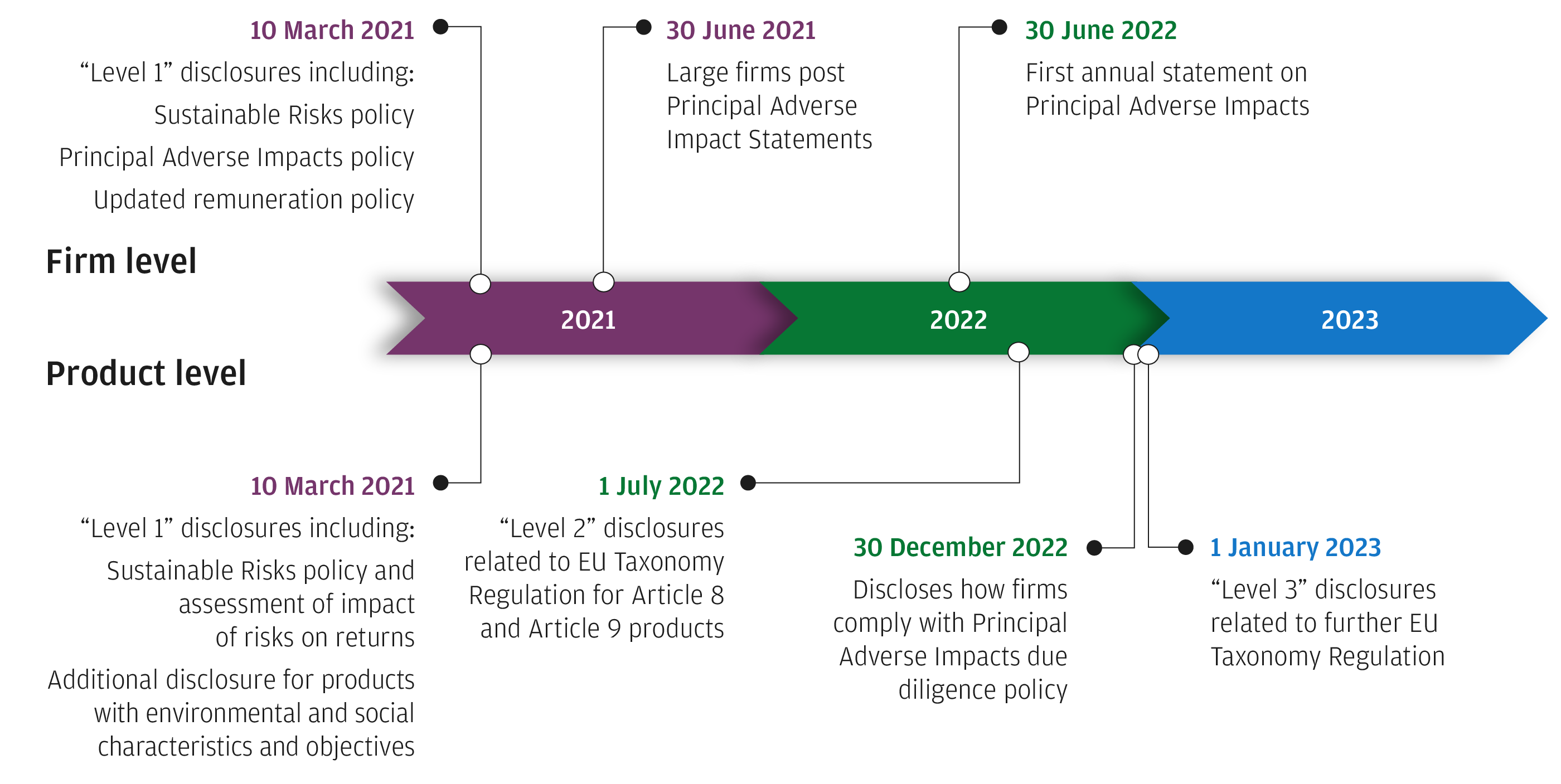

The disclosures, which went into effect 10 March 2021, apply to several financial products, including UCITS, AIFs and segregated mandates.

Why is the EU SFDR important?

Re-orienting capital towards sustainable growth and helping clients make better sustainable investing choices

The primary goals of the EU SFDR are to provide greater transparency on environmental and social characteristics, and sustainability within the financial markets, and to create common standards for reporting and disclosing information related to these considerations.

Increasing transparency and introducing standards supports two important additional considerations. First, it makes it harder for asset managers to “greenwash” their products – in other words, they cannot simply brand a product with an ESG or sustainable label, without being transparent with regards to how this is achieved.

Second, it provides investors with a significantly improved ability to compare investment options in terms of the degree to which ESG factors are a consideration within the investment decision-making process, which helps them make informed decisions that align with their investing goals.

Who is affected by the EU SFDR and which types of products and services does it apply to?

The EU SFDR applies to all financial market participants and financial advisers based in the EU. A financial market participant is any firm creating investment products, or generally, an asset manager. Financial advisers are individuals providing investment or insurance advice.

Investment managers or advisers based outside of the EU, who market (or intend to market) their products to clients in the EU under Article 42 of the Alternative Investment Fund Managers Directive (AIFMD), will also need to follow the SFDR disclosures.

Disclosures will apply to UCITS, AIFs, separately-managed portfolios and sub-advisory mandates, as well as to financial advice.

The UK is currently out of the scope of the EU SFDR. In June 2021 the UK Financial Conduct Authority (FCA) published a proposal to require climate-related financial disclosures for asset managers and insurers, among others (see link). We will need to wait and see how these proposals develop.

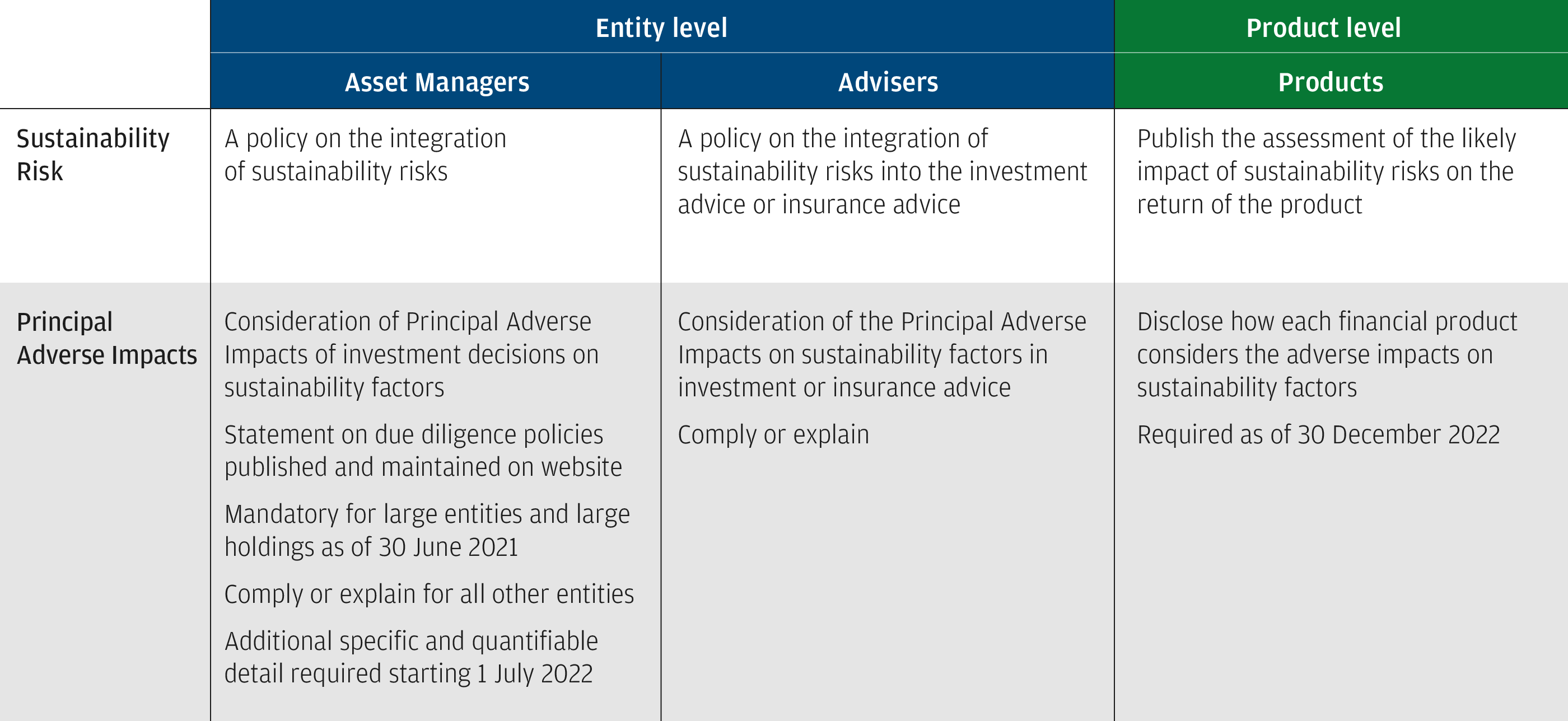

What are Sustainability Risks and Principal Adverse Impacts, and how do they impact asset managers and advisers?

To achieve the EU SFDR’s goal of improving sustainable finance by increasing transparency and creating standards, asset managers and advisers must disclose the manner in which they consider two key factors: Sustainability Risks and Principal Adverse Impacts. Asset managers are required to disclose their policies at both the firm and product level, while advisers are required to explain how they consider these factors in their advice.

The EU SFDR outlines specific definitions for Sustainability Risks and Principal Adverse Impacts:

- Sustainability Risks refer to environmental, social or governance events, or conditions, such as climate change, which could cause a material negative impact on the value of an investment.

- Principal Adverse Impacts are any negative effects that investment decisions or advice could have on sustainability factors. Examples could include investing in a company with business operations that significantly contribute to carbon dioxide emissions, or that has poor water, waste or land management practices.

Asset managers and advisers need to provide specific information on Sustainability Risks and Principal Adverse Impacts

Larger firms are required to disclose how they consider Principal Adverse Impacts from 30 June 2021, with Principal Adverse Impact reporting estimated to commence mid-2023 (representing Principal Adverse Impact data throughout 2022).

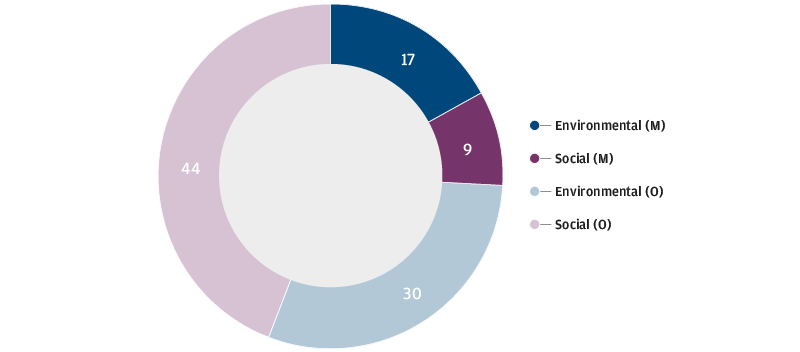

Subject to it being passed into EU law , from 1 July 2022, asset managers will be required to break out how they consider Principal Adverse Impacts into more specific and quantifiable detail, including in the region of nine indicators related to climate and the environment, and five indicators related to social and employee issues, respect for human rights, and anti-corruption and anti-bribery matters. There are currently an additional 16 environmental and 24 social indicators, which are optional, for which investment managers are encouraged to provide detail, when possible.

Number and type of sustainability indicators for measuring Principal Adverse Impacts

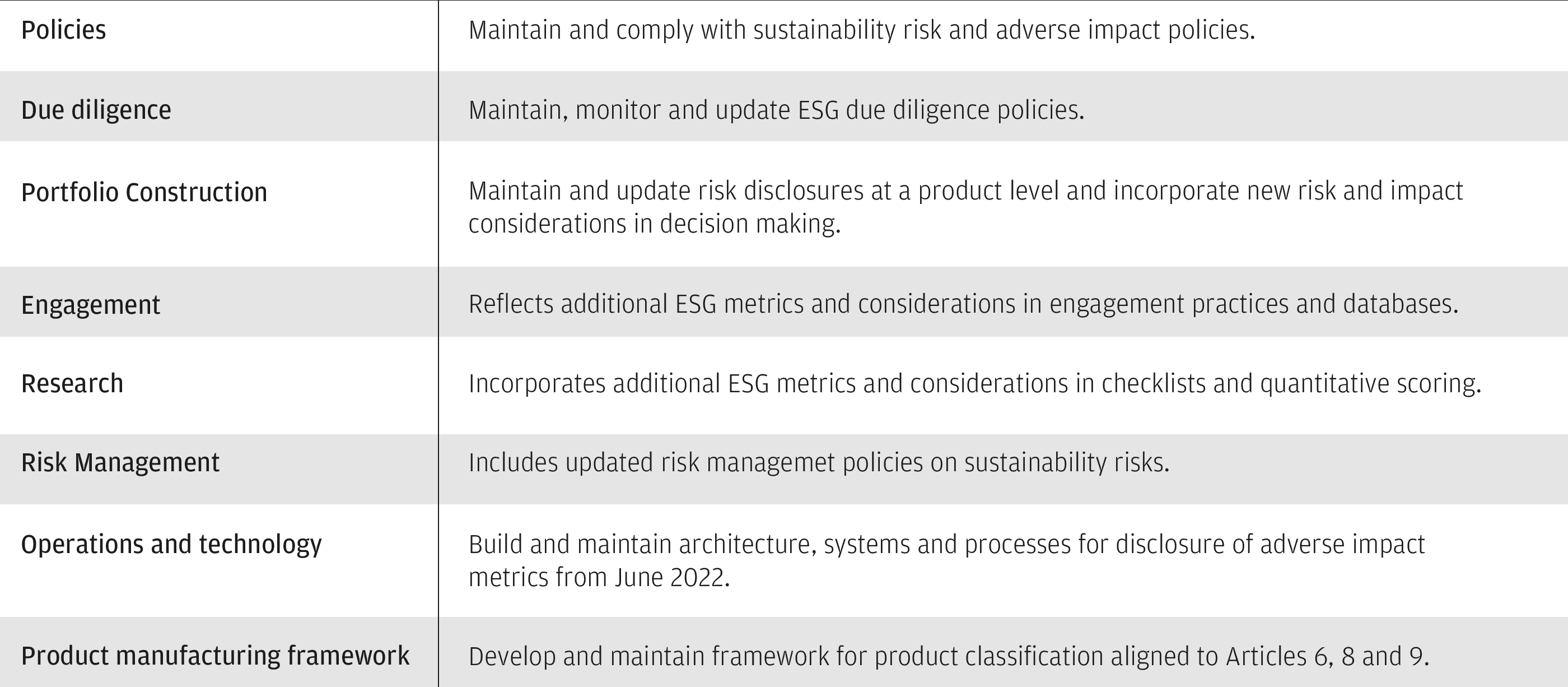

For asset managers, incorporating Sustainability Risks and Principal Adverse Impacts happen at several points during the investment process.

Checklist for asset managers incorporating Sustainability Risks and Principal Adverse Impacts into the investment process

Key Impacts

What are the ESG product categories and disclosures introduced by the EU SFDR?

The EU SFDR currently specifies three distinct categories for investment products with regards to sustainable investing and ESG considerations:

Article 6 products either integrate ESG considerations into the investment decision making process, or explain why sustainability risk is not relevant, but do not meet the additional criteria of Article 8 or Article 9 strategies.

Article 8 products promote environmental and/or social characteristics, and may invest in sustainable investments, but do not have sustainable investing as a core objective.

Article 9 products have sustainable investment as their core objective. The SFDR defines sustainable investment as an investment in an economic activity that contributes to an environmental or social objective, provided that the investment does not significantly harm any environmental or social objective and that the investee companies follow good governance practices.

Article 6, Article 8 and Article 9 disclosures

Article 6 financial products must disclose the manner in which sustainability risks are integrated into their investment decisions as well as an assessment of the likely impacts of sustainability risks on the returns of the financial products.

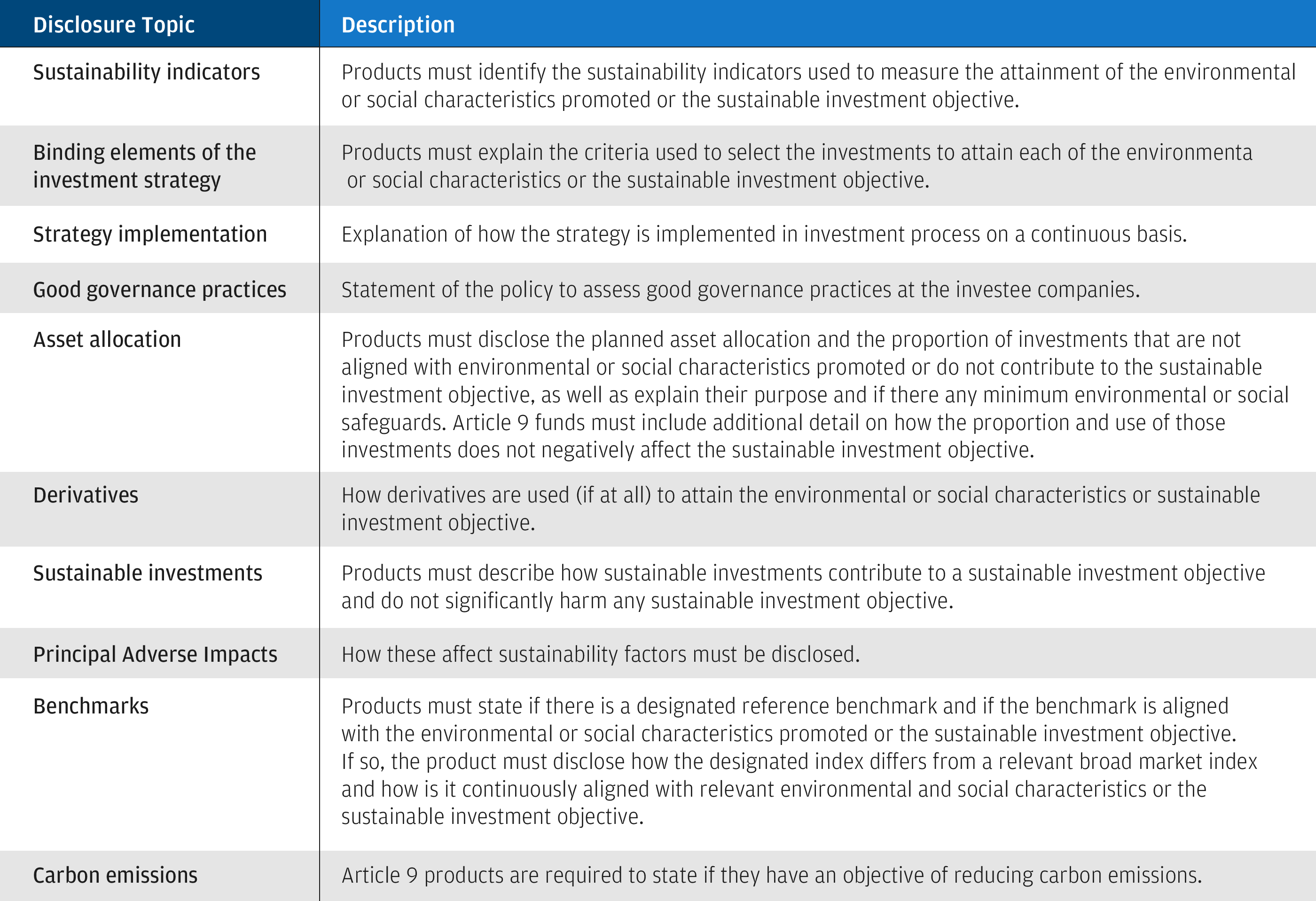

Article 8 and Article 9 financial products feature details on a variety of sustainability and ESG topics. The table below highlights a sample of the topics, though it is not a complete list.

Sample of topics featured in the disclosures for both Article 8 and Article 9 products

What is the EU Taxonomy Regulation and how does it affect the EU SFDR?

Upcoming additional EU Taxonomy disclosures

EU Taxonomy Regulation (EU TR) becomes effective 1 January 2022. Subject to it being passed into EU lawiii, from 1 July 2022, elements of the EU TR, which introduces a standard environmental criteria within the EU, will be integrated into the disclosure obligations set out by the EU SFDR. This will affect financial products that are classified as either Article 8 or Article 9. The EU TR specific elements to be disclosure under EU SFDR are outlined below.

Article 8 products will need to state if they have any investments in sustainable investments and, if so, will need to disclose whether these investments are in activities aligned with the EU TR.

Article 9 products, which by definition have sustainable investment as an objective, will have to disclose whether sustainable investments are in activities aligned with the EU TR.

What are upcoming developments should investors be aware of?

The implementation of the EU SFDR’s “Level 1” regulatory requirements – the disclosures that came into effect on 10 March 2021 and the initial statement of Principle Adverse Impacts for large companies published on 30 June 2021 – has been achieved. There remain a few additional items for investors to watch:

- The draft “Level 2” regulatory technical standards (RTS) disclosures, which will integrate the EU Taxonomy with the Article 8 and Article 9 disclosures. Approval for these proposed standards remains outstanding but is expected in the medium term and implementation is expected on 1 July 2022.

- As noted earlier, in June 2021 the UK FCA released a consultation on proposals to introduce climate-related financial disclosure rules and guidance for asset managers (see link), creating a parallel disclosure framework that goes beyond the EU SFDR.

- Developments driven by the European Commission will need to be reviewed, particularly the Commission’s focus on a potential social taxonomy and an extended environmental taxonomy.

- Third-party ESG-related industry standards will need to be reviewed as they get updated to align with the EU SFDR and the EU Taxonomy Regulation.

- The integration of ESG considerations may have implications for the delegated acts (DAs) under the UCITS, AIFMD, MiFID II, IDD and Solvency II frameworks.

- Parallel regulatory labelling requirements, such as Ecolabels, and/or related regulatory disclosure requirements from regulators in other regions, such as the Hong Kong Securities and Futures Commission (see link), may interact with the EU SFDR and have an aggregated impact on products and disclosures.

Looking ahead

The EU SFDR represents a positive step in the growth and development of sustainable and ESG investing within the EU. As investor interest in sustainable and ESG investing continues to grow, the regulation offers investors clear comparisons and advice on ESG and sustainable investments, enabling asset managers and advisers to help capital flow towards investment products that support a sustainable economy. The EU Taxonomy Regulation comes into effect on 1 January 2022. More information on this regulation, and how it interacts with the EU SFDR, will be made available in due course.

J.P. Morgan Asset Management is proud to help clients achieve their ESG and sustainable investing goals. If you have questions about the SFDR or sustainable investing, please contact us at sustainableinvesting.am@jpmorgan.com.

i https://ec.europa.eu/info/publications/210712-sustainable-finance-platform-draft-reports_en

ii 8 July 2021 the European Commission confirmed a six-month delay in the application of the detailed (“Level 2”) disclosure requirements (from January to 1 July 2022). Once this single text is adopted by the European Commission, the European Parliament and Council will then have three-months in which to scrutinise it before it becomes EU law.

iii 8 July 2021 the European Commission confirmed a six-month delay in the application of the detailed (“Level 2”) disclosure requirements (from January to 1 July 2022). Once this single text is adopted by the European Commission, the European Parliament and Council will then have three-months in which to scrutinise it before it becomes EU law.

09jf212307102203