NAIC 2023 Summer National Meeting

Global Insurance Solutions

09/01/2023

Wheatley Garner

Highlights:

- A proposal giving the SVO authority to revoke FE status receives significant industry pushback

- Negative IMR to be allowed, providing relief from elevated interest rates

- Residual tranche RBC factor to be increased for life insurers; regulators will also look to better define a residual interest

- Regulators finalize accounting rules for Schedule D bonds; to propose clarifying guidance for bonds pushed to Schedule BA

- The American Academy of Actuaries proposes new RBC framework for asset-backed securities

VOSTF1/SVO2 Updates

The SVO receives significant industry pushback from its proposal to overhaul the Filing Exempt (FE) process

In response to a years-long concern by regulators on the insurance industry’s overreliance on NRSRO3 ratings, along with a proliferation in the use of financial engineering to produce favorable regulatory results, the SVO released a proposal in May that would overhaul the FE process, giving the SVO additional authority to challenge and revoke the FE status of a security.

The proposal included various details as to what the process and criteria for a potential SVO challenge would look like, including:

- Sufficient notice to allow an insurer to appeal or provide additional information before any action is taken.

- A formal review process by the SVO, with an opportunity for a regulator(s) to consult on the deliberation, if they request.

- The establishment of a materiality threshold required to remove an NRSRO rating or security from FE eligibility. The materiality threshold is currently defined as a three or more notch difference in rating between the NRSRO assessment and the SVO’s assessment (NAIC 1.G versus NAIC 2.C, for example).

- A means to either deactivate the notice of concern or revoke FE eligibility.

- If FE eligibility is revoked, provide notice that a full filing is required.

- A means to re-instate the NRSRO rating or security to FE eligibility should changing conditions or ratings warrant.

In response, the proposal was met with strong opposition from various corners of the insurance, financial services and capital markets communities.

Notable criticisms of the proposal:

- A belief that the new rules would make the SVO an unregulated competitor of the NRSROs.

- The right to challenge an NRSRO rating sits solely with the SVO or potentially with one regulator. There is also no independent oversight to ensure consistency or ensure an independent review if SVO staff and an insurer disagree. A separate, independent appeals process, not overseen by the SVO, would also be preferred.

- The challenge process should have public disclosure requirements, as multiple insurers can be affected if they all hold the same security. Challenges could also be of interest to other market participants, such as other rating agencies. The lack of transparency could lead to market uncertainty and disruption.

- As a transparency measure, the NAIC should be required to publish aggregate statistics related to ratings challenges and their outcomes.

- A preference that the SVO not be the final arbiter when there is a disagreement between the SVO and an insurer on FE eligibility.

There is widespread concern that the proposal is affecting the demand for certain debt instruments, particularly due to the lack of certainty around capital requirements depending on the outcome.

The Financial Condition Committee (E Committee), which is the ultimate overseer of all investment-related NAIC activities, released a report that also suggested a few regulatory enhancements. This included support for reducing the reliance on NRSROs and developing a due diligence framework (with the help of an outside consultant) that would provide clear parameters around the use of NRSRO ratings for NAIC purposes. The goal of the E Committee isn’t for the SVO to replace NRSROs or perform their functions, but to enhance the SVO’s overall analytical abilities in ways that would strengthen its oversight.

The E Committee will also consider establishing a broad investment working group that could advise regulators on areas that may need more intensive regulator engagement and analysis on a confidential basis.

Discussions will continue amongst the SVO, VOSTF and the E Committee, with modified proposals to follow at a later date.

Adopted Items

Funds using repurchase agreements – Guidance amendment to clarify the type of repo that qualifies as a derivative

To eliminate confusion regarding a fund’s use of derivatives, the SVO has adopted a guidance amendment to clarify the type of repurchase agreements that qualifies as a derivative under the NAIC’s fund rules4 (derivative transactions within funds are limited in their use when not used for hedging currency or interest rate risks). The revised guidance specifies that any repurchase agreement where the fund sells securities and simultaneously agrees to repurchase the same or substantially the same securities at a stated price on a specified date would qualify as a derivative transaction.

The SVO amends its guidance pertaining to the credit deterioration of firms issuing letters of credit in reinsurance transactions

In response to the recent banking crisis affecting firms such as Silicon Valley Bank and Signature Bank, the SVO is proposing to update its guidelines for the removal of a financial institution from the list of Qualified U.S. Financial Institutions (QUSFI) eligible to issue letters of credit that can be used to reduce an insurer’s liability when ceding reinsurance to certain assuming insurers. To qualify as a QUSFI, the financial institution issuing a letter of credit must have a minimum rating of BBB-/Baa3. But the speed of recent bank failures has prompted the SVO to amend its guidance, allowing for prompt removal of a failed firm from the list once action has been taken or announced by its primary regulator.

Exposed Items, to be further considered

The SVO considers industry feedback on its proposal to update the definition of an NAIC Designation

In order to streamline its guidance on NAIC Designations, the SVO is currently proposing to consolidate and redefine some of its guidance on the use and purpose of an NAIC Designation, along with how it defines and governs securities with non-payment risks5 (Subscript “S” securities).

Feedback provided by the industry detailed a few concerns and further clarifications were requested on the proposal’s intent on a number of items:

- The definition of an NAIC Designation addresses the likelihood and probability of timely and full payment of principal and interest, but does not address expected recovery or loss given default (LGD). There is concern that this is a departure from the norm as NRSROs give consideration to LGD when assigning ratings, with the same also applying to RBC factors, which were designed with a consideration to LGD.

- The new definition also now incorporates the consideration of tail risks, without detail into what that consideration entails. Would it apply to both issuer obligations and structured securities, and how would it be analyzed? And would the tail risk analysis be consistent with the work done for the RBC framework?

- For securities with non-payment risks, the revised guidance appears to give the SVO additional authority to notch down NRSRO ratings used for filing exempt securities. There are questions as to whether that is appropriate for regulatory purposes and how a potential notching methodology would be defined.

Regulators will continue with their review of the industry’s concerns on the proposed guidance and turn around additional edits, where necessary.

Investment RBC Updates

Adopted Items

Residual tranches – An increase in capital charge adopted for life insurers

In June, the NAIC adopted its life RBC proposal on residual tranches, officially raising the pre-tax capital charge from 30% to 45%, with the change becoming effective at year-end 2024. For 2023, the applicable charge will stay at 30%, but life companies will also be required to apply an additional sensitivity test factor of 15%, which allows regulators to analyze what the potential impact to RBC ratios would have been had the change been effective for 2023.

Since this adoption only applies to life insurers, questions were raised about P&C and health residual tranche factors. Regulators detailed that because this was a more pressing matter for the life industry, the initial focus has primarily been placed on the life RBC framework. There are plans to address the residual tranche factors for P&C and health entities in the future, but a timeline on that project has yet to be determined.

Mortgage loans – RBC reduced for non-performing loans

Life regulators have adopted an RBC change to reduce the capital charges for non-performing mortgage loans. Due to the RBC reductions for real estate equity adopted in 2021, the RBC for non-performing loans (rated CM6 and CM7) was no longer in alignment with the RBC for Schedule A and Schedule BA real estate investments.

Prior to the 2021 change, the CM7 RBC factor for In Process of Foreclosure Commercial and Farm Mortgages reconciled with the 23% factor (pre-tax) for Schedule BA real estate equity, while the CM6 factor for 90-days Delinquent Commercial and Farm Mortgages was aligned with the 18% factor for Schedule A real estate equity. Those RBC factors have subsequently been lowered to 13% for Schedule BA and 11% for Schedule A. The proposed change is designed to retain consistency within the life RBC framework for mortgages and real estate investments. The expectation by regulators is that the change will be immaterial to the industry, as insurers rarely ever hold CM6 or CM7 loans.

Exposed Items, to be further considered

The American Academy of Actuaries proposes RBC changes for asset-backed securities (ABS)

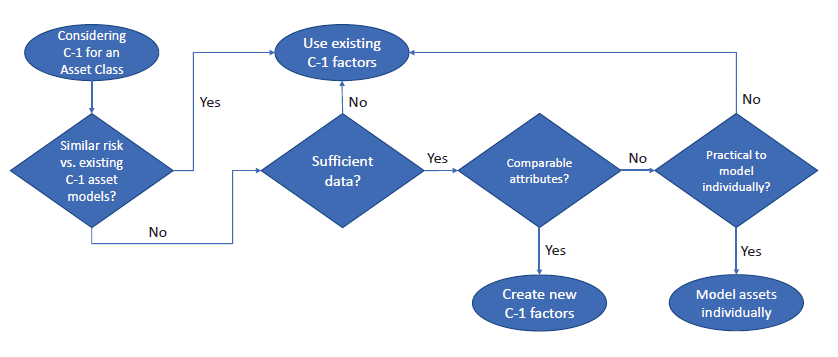

The American Academy of Actuaries (Academy) is proposing changes to the life RBC framework that institute asset modeling and incorporate a flowchart (EXHIBIT 1) to determine whether the ABS asset class needs to be modeled to determine its C-1 bond RBC factors, or if certain securities should be modeled individually to determine their bond factors.

EXHIBIT 1: Proposed C-1 RBC Factor Flowchart for ABS

Source: The American Academy of Actuaries, NAIC.

The goal of the project is to incorporate a principles-based approach to RBC for ABS that gives regulators flexibility to adapt to new structures as they emerge in the marketplace. The Academy’s proposal also acknowledges that for an asset class to be considered for this framework, 1) its risk must be material to the industry, 2) the risk being modeled needs to be applicable for the purposes of C-1 factors and 3) the benefits of any new processes should outweigh the costs, time and energy spent building out the process.

The proposed framework would consider a few pertinent questions to determine whether modeling would be appropriate for an asset class:

- Does similar risk exist versus current C-1 asset models? If so, then the current C-1 factors should suffice.

- Is there sufficient data to perform the modeling? For example, some esoteric ABS may not have the data necessary to build out a model.

- Do the individual assets within an asset class have easily identifiable attributes that can be used to sort the assets into risk buckets. For example, most CLOs have NRSRO ratings that place each tranche into a specific risk category. The same applies for mortgage loans – while they aren’t rated, the use of LTV and DSCR metrics allows them to be placed into industry accepted risk categories.

- Is it practical to model an asset individually? It may not be cost effective to model out individual deals. How common the underlying characteristics are would likely play a role in whether a model could be applied in a scalable manner.

The Academy would like to use this proposal as a starting point for future discussions with regulators, which will take place at upcoming Risk-Based Capital Investment Risk and Evaluation Working Group meetings.

Statutory Accounting Updates

Adopted Items

Negative IMR – Short-term proposal adopted to provide regulatory relief (Ref #2022-19)

Regulators have adopted revisions to the accounting rules for interest maintenance reserve (IMR) to provide relief from the negative accounting impacts of rising interest rates. The proposal will provide limited admittance of net negative IMR, which under current rules is disallowed and non-admitted.

The new guidance includes the following provisions:

- Allowance to admit up to 10% of adjusted capital and surplus – first in the general account (GA), and then, if all disallowed IMR in the GA is admitted and the percentage limit is not reached, to the separate account (SA) proportionately between insulated and non-insulated accounts.

- Requirement for RBC over 300% after an adjustment to exclude various soft assets (e.g. admitted positive goodwill, electronic data processing equipment and operating system software, DTAs and admitted IMR).

- There is no exclusion for derivatives losses included in negative IMR if the insurer can demonstrate historical practice in which realized gains from derivatives were also reversed to IMR (as liabilities) and amortized as part of IMR.

- Inclusion of a new reporting entity attestation.

- Application guidance for admitting/recognizing IMR in both the GA and SA.

The new guidance is officially listed as a temporary solution, with the effective date extending through December 31, 2025. The guidance automatically nullifies on January 1, 2026, but the effective date can be adjusted (nullified earlier or extended) based on regulator actions to establish permanent guidance.

Regulators adopt new accounting rules for Schedule D bonds; will also look to clarify guidance for bonds pushed to Schedule BA (Ref #2019-21)

After years of work on the principles-based project to revamp the accounting rules for Schedule D bonds, regulators have begun to finalize and adopt significant portions of the new guidance. SAPWG6 has adopted its new SSAP 26R (issuer obligations) and SSAP 43R (asset-backed securities), which will detail what’s allowable for Schedule D-1 access. The adoption will be effective as of January 1, 2025, to allow insurers time to analyze the resulting impact on their investment portfolios.

For bonds that no longer qualify as Schedule D bonds, regulators have incorporated a few clarifying edits:

- Debt securities that do not qualify as bonds for Schedule D-1 purposes, and for which the primary source of repayment is derived through rights to underlying collateral, qualify as admitted assets if the underlying collateral primarily qualifies as admitted invested assets. Any residual tranches or first loss positions held from the same securitization that did not qualify as a bond also only qualify to the extent the underlying collateral primarily qualifies as admitted invested assets. Furthermore, if a debt security from a securitization is (or would be) non-admitted, then any residual interests or first loss positions held from the same securitization would also be non-admitted.

- SAPWG will sponsor a blanks proposal to revise Schedule BA for bonds that do not qualify as Schedule D-1 securities, with an additional request that the SVO assess whether additional guidance is needed to clarify and/or permit the assignment of SVO-provided NAIC Designations for bonds that do not qualify as Schedule D-1 securities (clarity on the FE eligibility would also need to be addressed). SAPWG is also requesting that the CATF7 opine on the RBC impact of the split between non-Schedule D-1 bonds with SVO-assigned NAIC Designations versus securities without NAIC Designations. This is particularly important for life insurers, which have historically had the ability to reduce the capital charges on Schedule BA assets with NAIC Designations.

Reference Rate Reform (Ref #2023-05, INT 20-01)

To prepare for the transition away from the London Interbank Offered Rate (LIBOR) and other interbank offered rates, regulators previously adopted guidance that granted temporary (optional) waivers from derecognizing hedging transactions and provided some exceptions for assessing hedge effectiveness. The relief also included derivative instruments affected by changes to the rates used for discounting, margining or contract price alignment (regardless of whether they referenced LIBOR or another interbank rate that is expected to be discontinued). Regulators have adopted guidance to extend these temporary waivers to December 31, 2024, which will allow for the continuation of existing hedge relationships and thus not require hedge de-designation due to reference rate reform.

CLOs – Financial modeling added to statutory accounting rules (Ref #2023-02)

Regulators officially adopted a new amendment to add CLO modeling guidance to the statutory accounting guidance for ABS (SSAP 43R), while also clarifying that CLOs are not captured as legacy securities8.

Exposed Items, to be further considered

Residual tranches – Guidance amendment proposed to clarify definition and reporting requirements (Ref #2023-12)

Regulators have proposed revisions to accounting guidance to better clarify the definition and reporting requirements for investment structures that represent residual interests or a residual security tranche. When reviewing the 2022 annual statements, regulators concluded that residuals might have been underreported by insurers, possibly due to the various forms that residual investments can take. The structural design of a residual interest or residual security tranche can vary, but the overall concept is that they receive “residual” cash flows after all debt holders receive contractual interest and principal payments. Guidance is being added to SSAP 48 – Joint Ventures, Partnerships and Limited Liability Companies and SSAP 43R – Loan-Backed and Structured Securities that also specifies that:

- Residuals exist in structures that issue one or more classes of debt securities created for the primary purpose of raising debt capital backed by collateral assets.

- The primary source of debt repayment is derived through rights to the cash flows of a discrete pool of collateral assets.

- The collateral assets generate cash flows that provide interest and principal payments to debt holders through a contractually prescribed distribution methodology (e.g., waterfall dictating the order and application of all collateral cash flows).

- The residual holders in the structure continue to receive payments from the collateral so long as there are cash flows in excess of the debt obligations. The payments to the residual holder may vary significantly, both in timing and amount, based on the underlying collateral performance.

Following a short comment period ending September 12, the goal remains for this to be adopted and implemented in time for year-end 2023.

Asset Valuation Reserve (AVR) and Interest Maintenance Reserve (IMR) – A long-term project will better define the accounting guidance for AVR and IMR (Ref #2023-14)

Regulators are adding to the agenda a new, long-term project to better define the accounting rules for AVR and IMR in SSAP 7 – Asset Valuation Reserve and Interest Maintenance Reserve. Historically, SSAP 7 only provided a brief overview without instructions containing more detailed language. The aim is that the project would address a few disconnects between the statutory accounting principles and the annual statement instructions for AVR/IMR, while specifically addressing a few topical issues.

Future discussions are likely to be focused on:

- Absolutes in allocating between IMR and AVR – Clarity has been requested for situations where a sale occurred before an official downgrade, but the sale was clearly the result of a notable decline in credit quality (See the following section Allocating losses between IMR versus AVR).

- Bond IMR/AVR allocation – The guidance for IMR/AVR differs between issuer obligations and ABS. Also, since the current guidance was implemented before the expansion of NAIC Designations from 6 to 20, the guidance is no longer clear on what constitutes a designation change.

- Perpetual preferred stock allocation – The guidance hasn’t been reviewed since the accounting change requiring that all perpetual preferred stock be reported at fair value.

- Delineation of non-interest versus interest and realized versus unrealized – The proposal will focus on principles-based concepts to establish the division between interest and non-interest changes, as well as the reporting of unrealized and realized changes. This will help ensure consistent application across the industry.

- Derivative guidance – Guidance revisions will be needed to improve the reporting of interest rate derivatives held at fair value (i.e. derivatives that do not qualify for hedge accounting).

- Reinsurance ceded/assumed – While the annual statement instructions include guidance for removal of IMR for reinsurance ceded, and the acquisition of IMR for reinsurance assumed, the impact of reinsurance, particularly with the dissolution of reinsurance agreements when IMR had initially been transferred, is a common question on determining IMR and AVR for insurers.

- AVR/IMR cross checks – Better cross checks are needed to ensure that items are being mapped to AVR/IMR correctly between reporting schedules.

- Overall IMR and AVR reporting in GA and SA – The reporting of IMR and AVR, including how positive balances in one account impact negative balances in another account, as well as the treatment of net negative IMR, will be a long-term focus. This will lead to a need for guidance revisions in SSAP 7 and SSAP 56 (Separate Accounts).

Allocating losses between IMR versus AVR (Ref #2023-15)

SAPWG is proposing guidance revisions to remove the ability to allocate non-interest related losses to IMR. This was always the original intent of the current rules, but the guidance in the annual statement instructions created some unintended ambiguity.

The proposed guidance revisions clarify that, for issuer obligations and preferred stocks, IMR is only for realized gains and losses that are predominately related to interest-related changes. If the NAIC Designation at the end of the holding period, or within a reasonable amount of time after the insurer has sold/disposed of the instrument, is different from its NAIC Designation at the beginning of the holding period by more than one NAIC Designation or NAIC Designation category, the gains or losses from those instruments shall NOT be reported in IMR and shall be reported in AVR.

For mortgage loans, realized gains or losses from mortgages that meet any of the following criteria shall be reported in the AVR, and not IMR:

- Any mortgage loan sold/disposed of with an established valuation allowance under SSAP 37

- Interest is more than 90 days past due

- The loan is in process of foreclosure

- The loan is in course of voluntary conveyance

- The terms of the loan have been restructured during the prior two years

Schedule BA Reporting Categories (Ref #2023-16)

Guidance revisions are being proposed to incorporate more detailed definitions for Schedule BA investments that fall under SSAP 48 – Joint Ventures, Partnerships and Limited Liability Companies. Schedule BA investments have primary reporting categories (non-registered private funds, joint ventures, partnerships or limited liability companies, or residual interests) and subcategories (fixed-income instruments, common stocks, real estate, mortgage loans, other) that denote the underlying characteristics of the assets within the primary categories. Regulators will look to refine the instructions and examples for Schedule BA’s subcategories to better reflect market convention and improve consistency.

Short-Term Investments (Ref #2023-17)

Regulators have proposed revisions to the guidance in SSAP 2R – Cash, Cash Equivalents, Drafts and Short-Term investments to establish principal concepts for the types of investments that should be permitted for reporting as either cash equivalents or short-term investments. The review of short-term investments is in response to noted situations where certain types of investments, particularly collateral loans or other Schedule BA items, are being specifically designed to meet the parameters for short-term reporting. Regulators have become aware of short-term collateral loan investments where rules are being circumvented so that they can qualify as a short-term investment on Schedule DA and not Schedule BA, thereby receiving better regulatory treatment (e.g., reduced RBC charges, exclusions from state investment limitations).

The proposed guidance is likely to include a new revision that excludes an investment from being reported as a cash equivalent or short-term investment unless it would also qualify as an issuer credit obligation under SSAP 26R – Bonds. Such investments will then only qualify as a cash equivalent or short-term investment if it has a maturity date within 3 months (cash equivalents) or 12 months (short term) from the date of acquisition or meets the specific requirements for money market mutual funds or cash pooling arrangements. This would ensure that certain investment types are captured in the intended reporting schedule.

To align with the principles-based bond project adoption (see previous Regulators adopt new accounting rules for Schedule D bonds), the proposed effective date of this new guidance is January 1, 2025.

1 Valuation of Securities Task Force

2 Securities Valuation Office

3 Nationally Recognized Statistical Rating Organization

4 NAIC Fund Lists include the 1) NAIC U.S. Government Money Market Fund List, 2) SVO-Identified ETF Bond and Preferred Stock Lists, 3) NAIC Fixed Income-Like SEC Registered Funds List and 4) NAIC List of Schedule BA Non-Registered Private Funds With Underlying Assets Having Characteristics of Bonds or Preferred Stock. Funds on the NAIC U.S. Government Money Market Fund List are not permitted to use any derivatives transactions or instruments.

5 Non-payment risks under NAIC rules pertain to contractual agreements between the insurer and the issuer in which the issuer is given some measure of financial flexibility not to make payments. This also includes situations where the insurer agrees to be exposed to participatory risk.

6 Statutory Accounting Principles Working Group

7 Capital Adequacy Task Force

8 Legacy securities are financially modeled CMBS and non-agency RMBS issued prior to 2013. The NAIC Designation for legacy securities is determined by using CUSIP-specific modeled breakpoints and the security’s book-adjusted carrying value.

094z233108163948