Too Long at the Fair: Time to retire the US/Emerging Markets barbell for a while

Summary. I have recommended since 2009 that equity investors overweight the US and Emerging Markets, and underweight Europe and Japan. The excess returns from such a strategy when applied to regional MSCI equity indexes have been enormous over that time frame. However, the time has come to retire the barbell for a while. I stayed too long at the fair, and should have made this recommendation a few months ago when Europe was trading at a record 35% P/E discount to the US. A modestly brighter picture in Japan relative to China is another reason why it’s time to put the barbell aside for now.

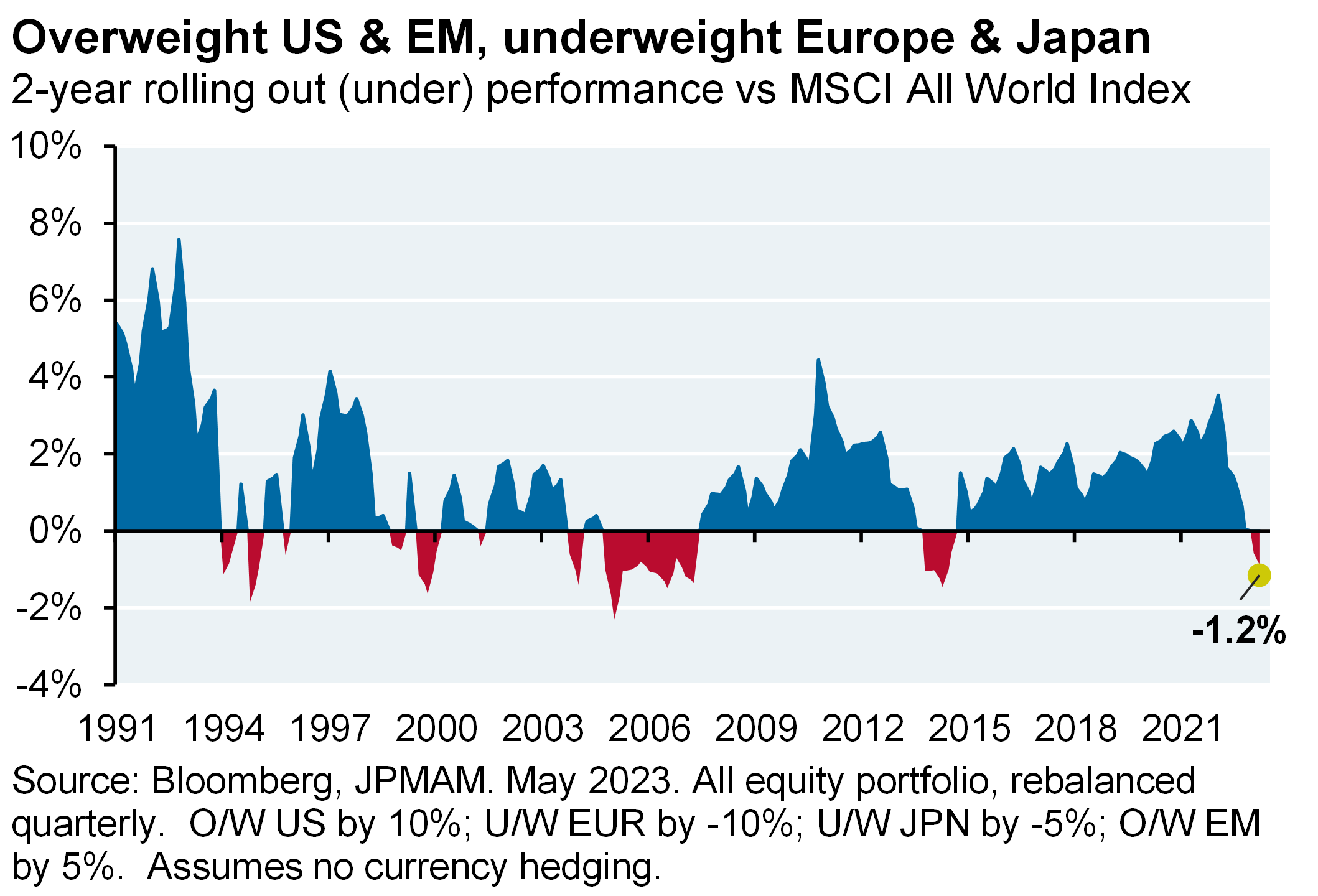

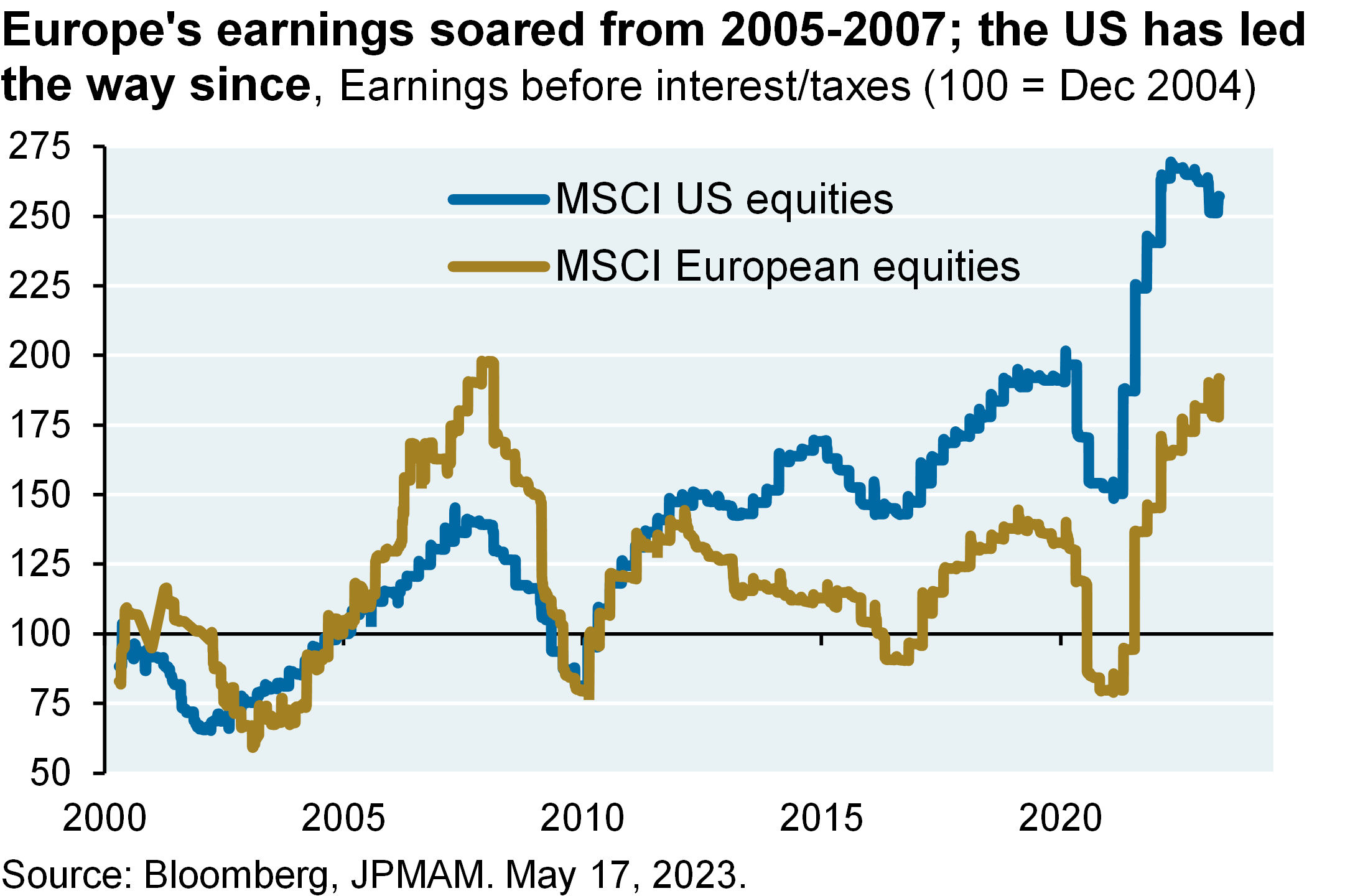

[1] The barbell’s amazing run. The barbell’s performance since 1988 is shown in the first two charts using both a three-year and two-year performance horizon. Before its underperformance this year, the barbell had a remarkable streak1. In other words, the -120 bps of barbell underperformance over the last two years is small relative to the consistency and magnitude of prior barbell outperformance. Note that the worst period for the barbell was the golden era for Europe in 2005-2007; more on that below.

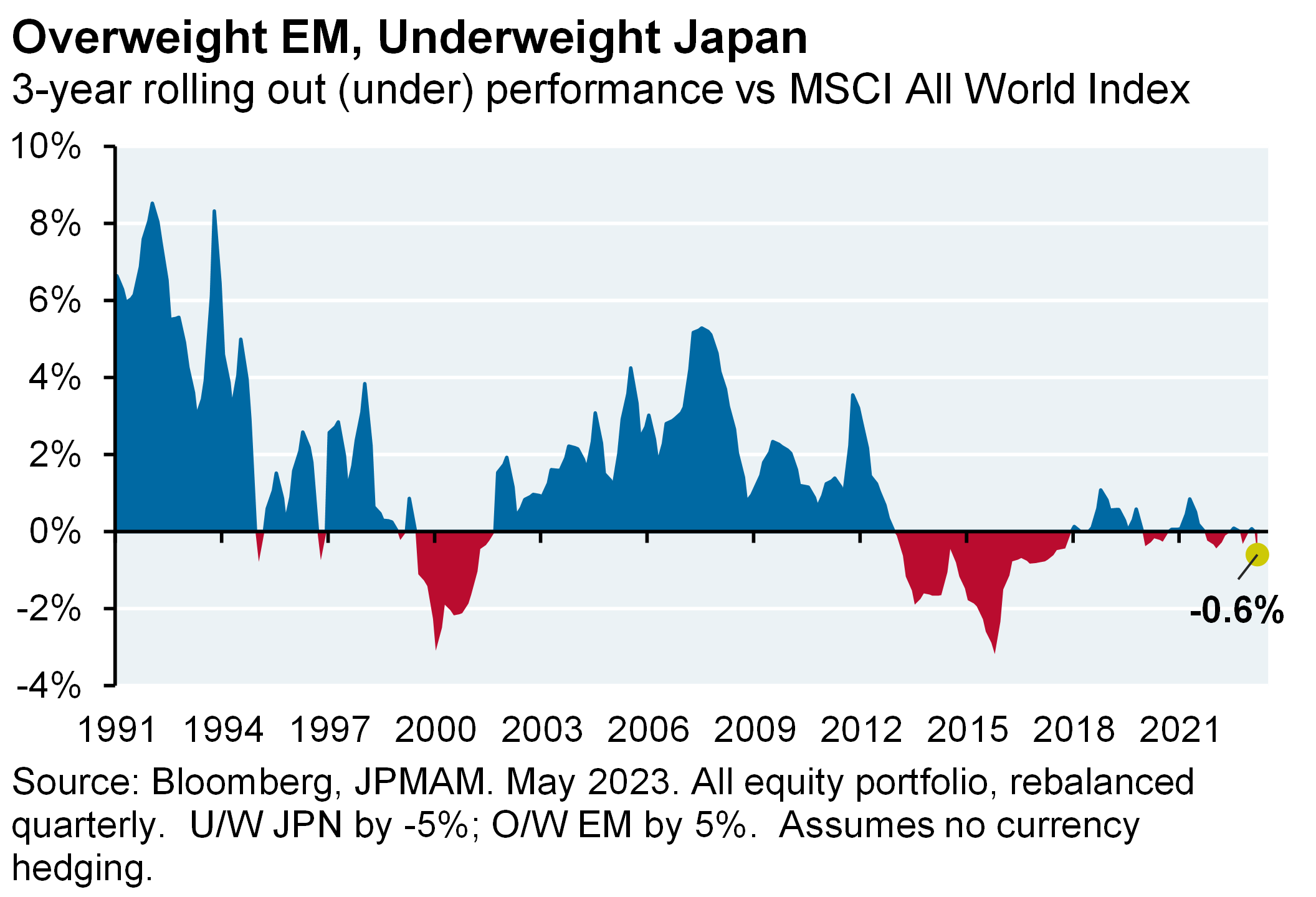

Most of the barbell outperformance since 2009 is due to US outperformance vs Europe, rather than Emerging Markets outperformance vs Japan. As shown below, the impact of overweighting Emerging Markets vs Japan was split between positive results from 2009 to 2013, underperformance from 2014 to 2019 and no material impact since 2019.

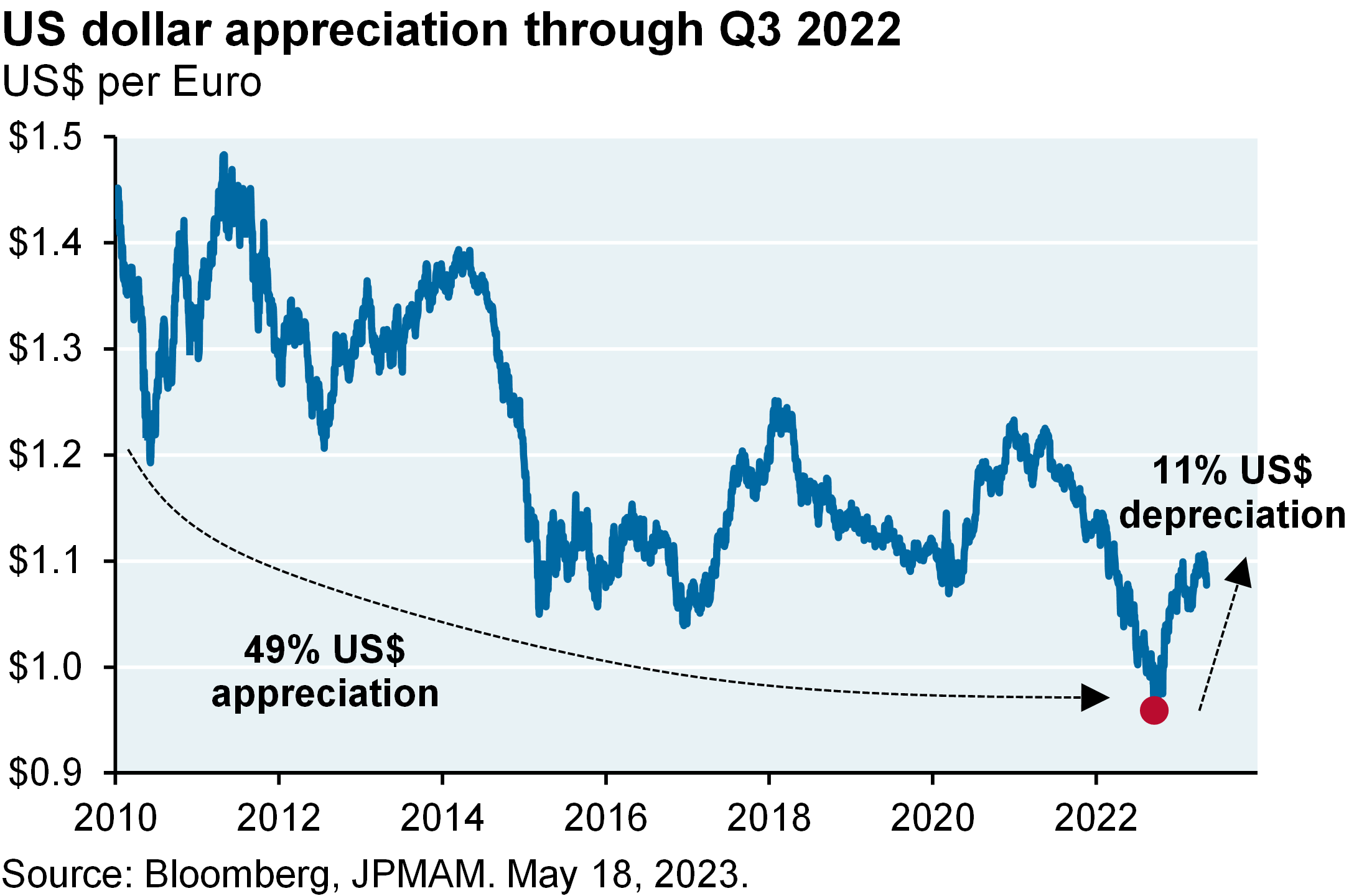

[2] Why the US outperformed Europe since 2009. The next chart decomposes reasons for US outperformance vs Europe over this period. The 5 largest factors: outperformance of the US dollar vs the Euro (illustrated in the chart above); the benefit of US sector weights which are larger in Tech and lower in Financials, Energy, Industrials and Staples; and the outperformance of US tech stocks, consumer discretionary and financials vs their European counterparts. These factors explain almost all US outperformance since 2009; only 7% of the outperformance is unaccounted for.

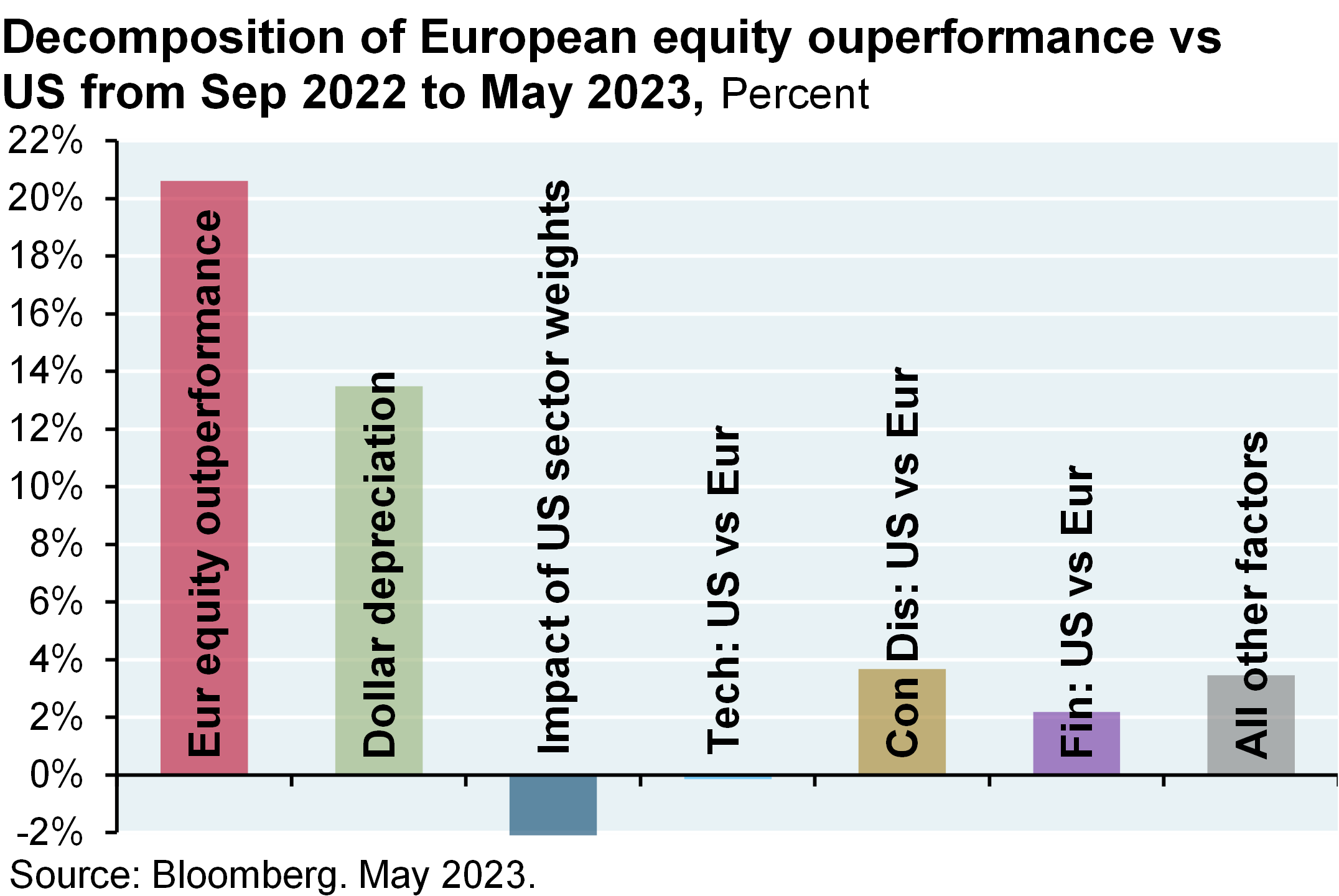

[3] What’s been driving recent barbell underperformance. Since September 2022, Europe has outperformed the US by ~20%. As shown below, 2/3 of this outperformance is due simply to the decline in the dollar vs the Euro. As we wrote last time (see Archives), while we do not see the dollar’s reserve currency status under serious threat, there’s room for the dollar to decline due to its prior sharp rise vs other currencies.

What else explains Europe’s outperformance? The other positive for Europe: outperformance of its Consumer Discretionary stocks vs US counterparts. The next largest factor: relative outperformance of EU financials, but it’s small in the context of overall European outperformance. That gap may widen further given US regional bank commercial real estate exposure, which we wrote about on April 10. But I’m reluctant to base a long Europe strategy on the reported strength of its banks. The April 10 Eye on the Market also showed how Credit Suisse ranked at or near the top of EU bank statistics on capital, leverage, liquidity and funding ratios and still failed. Certain risks are just hard to capture in balance sheet ratios.

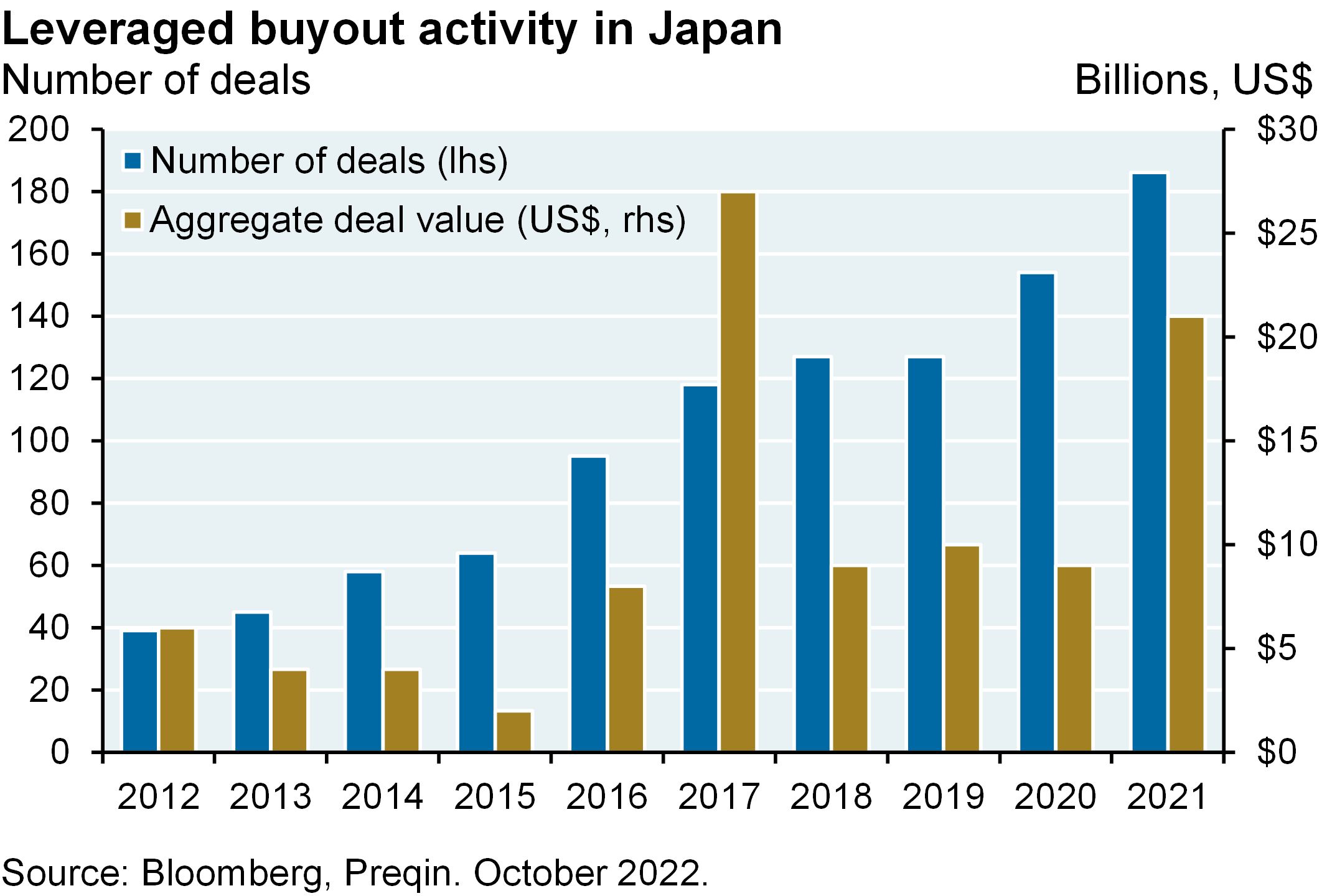

What explains Japan’s 11% outperformance vs EM since last fall? One factor is a resurgence in M&A activity in Japan, which is unusual. Much of the recent rise comes from foreign investors, which is even rarer: Bain’s acquisitions of Hitachi Metals for $5.6 bn, Evident for $3.1 bn and Gelato Pique for $1.4 bn; KKR’s acquisition of Hitachi Transport for $5.2 bn; and the Fortress acquisition of Seven & i for $1.8 bn. More on Japan below.

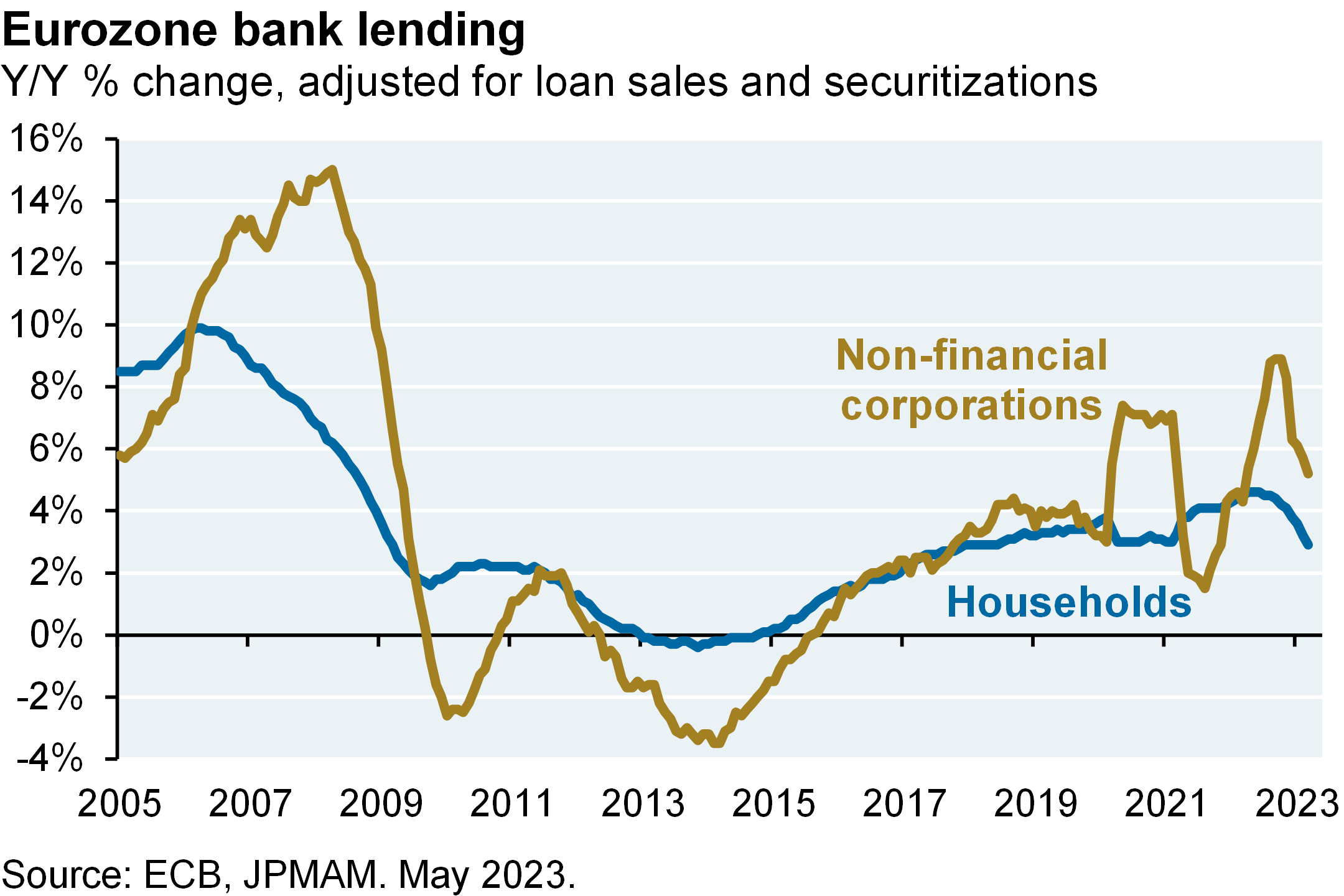

[4] The 2005-2007 era is not a useful parallel for projecting another period of European outperformance. I’ve seen research citing Europe’s earnings surge in 2005-2007 as a reason for being overweight Europe, since it could happen again as structural banking and energy constraints fade. But I don’t buy that argument: Europe’s earnings surge at the time was heavily influenced explosive bank lending that’s unlikely to repeat itself. See the charts below: bank lending has picked up in Germany and to a lesser degree in France, but in Southern Europe it never recovered. Maybe there’s some other rationale for projecting an earnings surge in Europe; the 2005-2007 period is not it.

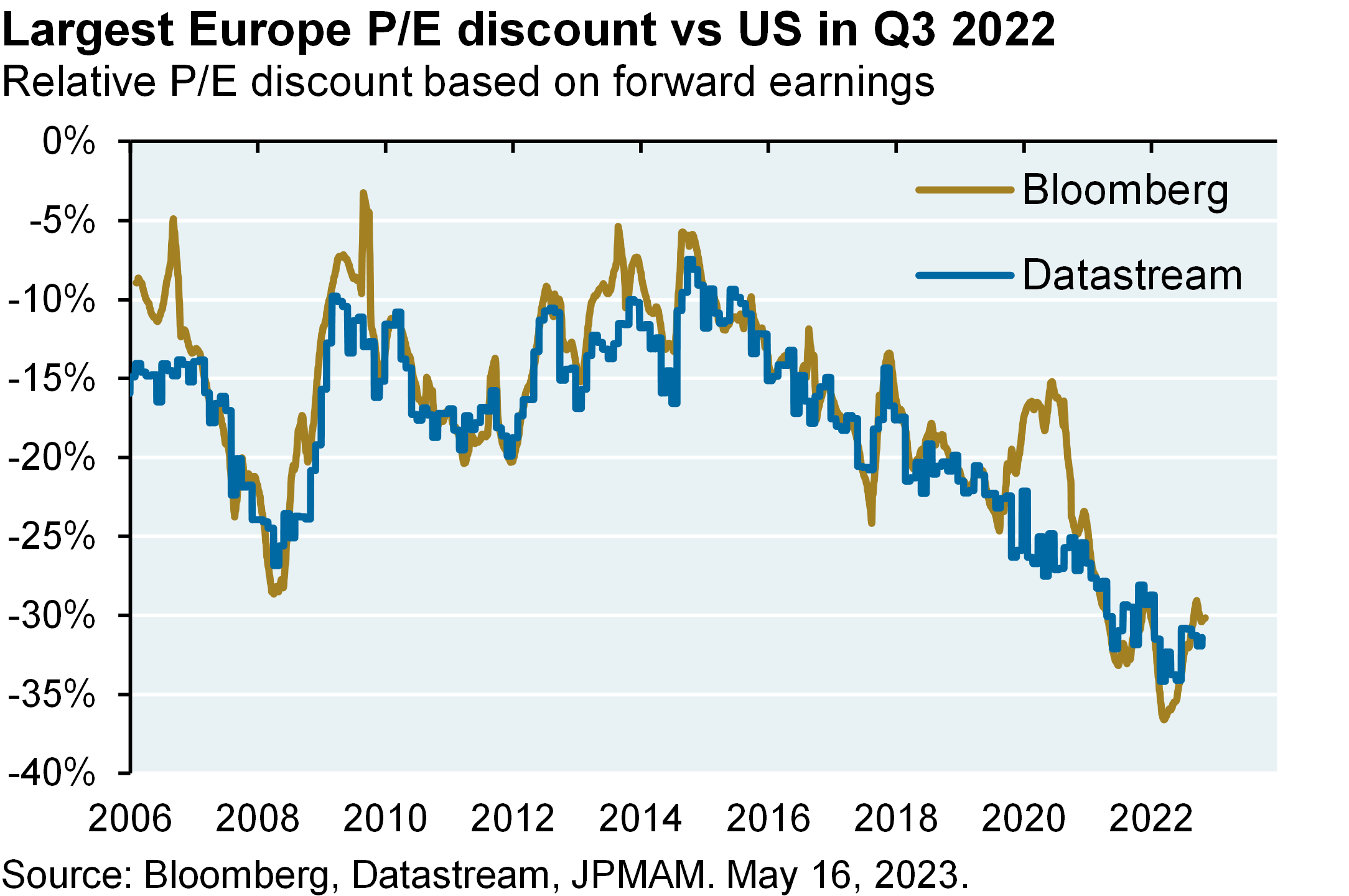

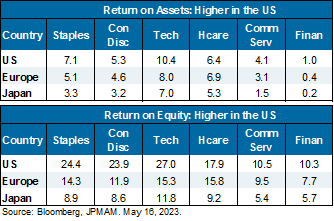

[5] Given higher sector weights in staples, financials, energy and utilities, Europe is essentially a value investment. I should have paid more attention to just how cheap it got, particularly after the Euro had declined by 50% vs the US$ since 2010. By September 2022, Europe’s P/E multiple hit a post-20062 low relative to the US. While there were valid concerns at the time about Europe’s energy situation, rising inflation and exposure to a shuttered China, investors were receiving an enormous discount for taking European equity exposure, and I should have paid more attention to that. Europe’s outperformance is likely to have a ceiling since US companies generate higher returns on equity and higher returns on assets, as shown in the table. But everything has a price, and a 35% P/E discount was apparently it. As things stand now, the discount is still large from an historical perspective.

Wrapping up. Since the valuation discount remains high, there might be some legs left in the anti-barbell trade. Another reason: Japan looks interesting again (see box), particularly relative to China which has risen to ~40% of the EM equity index and which still has a lot of problems. I wouldn’t argue for a reverse barbell, which would overweight Europe and Japan; I don’t have enough conviction in European equities for that, particularly with the ECB having more tightening to do. I also think that the US debt ceiling will be raised, one way or another3. But I do think that the barbell’s best days are behind it for a while, and believe that investors should proceed with more regional balance in global equity portfolios.

Japanese equities may benefit from the following catalysts:

- Japanese equities trade at 25%-30% P/E discount to US, as they have since 2016

- Record increase in stock buybacks driven by corporate governance reforms (i.e., Sony spinoff/buyback)

- Governance reforms: [a] ~50% of companies trade below book value and must outline a plan to maximize shareholder value and comply with shareholder, liquidity and outside director reforms; [b] 10%-20% of companies do not comply with cross-holding and free float criteria and must remedy or face delisting

- Half of Japanese companies have positive net cash positions vs <20% in the US/Europe

- Very low positioning in Japanese equities by non-Japanese investors

- A recent surge in non-Japanese LBO activity in Japan, which is extremely rare (discussed earlier)

- Lower wage pressures than US/Europe, COVID supply chain pressures easing

- Earnings expected to be flat vs contractions in the US and Europe

- The lowest real effective exchange rate in Japan in 50 years according to CEIC; the Yen has also depreciated by 30% vs the Chinese RMB, which is relevant since Japan now exports more to China than to the US

1 Professor Elroy Dimson estimates that US equities outperformed non-US markets by ~2% per year from 1900 to 2021, which translates into very large cumulative excess returns. For most of this period, higher dividends explained the difference; since 1990, higher US valuations has been the dominant factor. Jack Bogle argues that excess US returns are not random and reflect US exceptionalism with respect to deeper markets and rule of law.

2 Our European P/E charts start in 2006. Before 2006, IFRS accounting standards required European companies to amortize goodwill, and the amounts involved were at times substantial. As a result, pre-2006 P/E multiples for Europe are not comparable to post-2006 multiples, and can distort time series comparisons vs the US.

3 Yellen says it would be a calamity not to raise the debt ceiling. I wonder how she would describe the charts in our Jan 24 piece on inflation adjusted debt per capita since 1790, and on the collapse in discretionary spending due to rising entitlements. Those look like calamities too.

IMPORTANT INFORMATION

This report uses rigorous security protocols for selected data sourced from Chase credit and debit card transactions to ensure all information is kept confidential and secure. All selected data is highly aggregated and all unique identifiable information, including names, account numbers, addresses, dates of birth, and Social Security Numbers, is removed from the data before the report’s author receives it. The data in this report is not representative of Chase’s overall credit and debit cardholder population.

The views, opinions and estimates expressed herein constitute Michael Cembalest’s judgment based on current market conditions and are subject to change without notice. Information herein may differ from those expressed by other areas of J.P. Morgan. This information in no way constitutes J.P. Morgan Research and should not be treated as such.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own professional advisers, if any investment mentioned herein is believed to be suitable to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

Non-affiliated entities mentioned are for informational purposes only and should not be construed as an endorsement or sponsorship of J.P. Morgan Chase & Co. or its affiliates.

For J.P. Morgan Asset Management Clients:

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy.

ACCESSIBILITY

For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance.

This communication is issued by the following entities:

In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be.; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), which this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For all other markets in APAC, to intended recipients only.

For J.P. Morgan Private Bank Clients:

ACCESSIBILITY

J.P. Morgan is committed to making our products and services accessible to meet the financial services needs of all our clients. Please direct any accessibility issues to the Private Bank Client Service Center at 1-866-265-1727.

LEGAL ENTITY, BRAND & REGULATORY INFORMATION

In the United States, bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A. and its affiliates (collectively “JPMCB”) offer investment products, which may include bank-managed investment accounts and custody, as part of its trust and fiduciary services. Other investment products and services, such as brokerage and advisory accounts, are offered through J.P. Morgan Securities LLC (“JPMS”), a member of FINRA and SIPC. Annuities are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. JPMCB, JPMS and CIA are affiliated companies under the common control of JPM. Products not available in all states.

In Germany, this material is issued by J.P. Morgan SE, with its registered office at Taunustor 1 (TaunusTurm), 60310 Frankfurt am Main, Germany, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB). In Luxembourg, this material is issued by J.P. Morgan SE – Luxembourg Branch, with registered office at European Bank and Business Centre, 6 route de Treves, L-2633, Senningerberg, Luxembourg, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – Luxembourg Branch is also supervised by the Commission de Surveillance du Secteur Financier (CSSF); registered under R.C.S Luxembourg B255938. In the United Kingdom, this material is issued by J.P. Morgan SE – London Branch, registered office at 25 Bank Street, Canary Wharf, London E14 5JP, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – London Branch is also supervised by the Financial Conduct Authority and Prudential Regulation Authority. In Spain, this material is distributed by J.P. Morgan SE, Sucursal en España, with registered office at Paseo de la Castellana, 31, 28046 Madrid, Spain, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE, Sucursal en España is also supervised by the Spanish Securities Market Commission (CNMV); registered with Bank of Spain as a branch of J.P. Morgan SE under code 1567. In Italy, this material is distributed by J.P. Morgan SE – Milan Branch, with its registered office at Via Cordusio, n.3, Milan 20123, Italy, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – Milan Branch is also supervised by Bank of Italy and the Commissione Nazionale per le Società e la Borsa (CONSOB); registered with Bank of Italy as a branch of J.P. Morgan SE under code 8076; Milan Chamber of Commerce Registered Number: REA MI 2536325. In the Netherlands, this material is distributed by J.P. Morgan SE – Amsterdam Branch, with registered office at World Trade Centre, Tower B, Strawinskylaan 1135, 1077 XX, Amsterdam, The Netherlands, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – Amsterdam Branch is also supervised by De Nederlandsche Bank (DNB) and the Autoriteit Financiële Markten (AFM) in the Netherlands. Registered with the Kamer van Koophandel as a branch of J.P. Morgan SE under registration number 72610220. In Denmark, this material is distributed by J.P. Morgan SE – Copenhagen Branch, filial af J.P. Morgan SE, Tyskland, with registered office at Kalvebod Brygge 39-41, 1560 København V, Denmark, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – Copenhagen Branch, filial af J.P. Morgan SE, Tyskland is also supervised by Finanstilsynet (Danish FSA) and is registered with Finanstilsynet as a branch of J.P. Morgan SE under code 29010. In Sweden, this material is distributed by J.P. Morgan SE – Stockholm Bankfilial, with registered office at Hamngatan 15, Stockholm, 11147, Sweden, authorized by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB); J.P. Morgan SE – Stockholm Bankfilial is also supervised by Finansinspektionen (Swedish FSA); registered with Finansinspektionen as a branch of J.P. Morgan SE. In France, this material is distributed by JPMCB, Paris branch, which is regulated by the French banking authorities Autorité de Contrôle Prudentiel et de Résolution and Autorité des Marchés Financiers. In Switzerland, this material is distributed by J.P. Morgan (Suisse) SA, with registered address at rue de la Confédération, 8, 1211, Geneva, Switzerland, which is authorised and supervised by the Swiss Financial Market Supervisory Authority (FINMA), as a bank and a securities dealer in Switzerland. Please consult the following link to obtain information regarding J.P. Morgan’s EMEA data protection policy: https://www.jpmorgan.com/privacy.

In Hong Kong, this material is distributed by JPMCB, Hong Kong branch. JPMCB, Hong Kong branch is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission of Hong Kong. In Hong Kong, we will cease to use your personal data for our marketing purposes without charge if you so request. In Singapore, this material is distributed by JPMCB, Singapore branch. JPMCB, Singapore branch is regulated by the Monetary Authority of Singapore. Dealing and advisory services and discretionary investment management services are provided to you by JPMCB, Hong Kong/Singapore branch (as notified to you). Banking and custody services are provided to you by JPMCB Singapore Branch. The contents of this document have not been reviewed by any regulatory authority in Hong Kong, Singapore or any other jurisdictions. You are advised to exercise caution in relation to this document. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. For materials which constitute product advertisement under the Securities and Futures Act and the Financial Advisers Act, this advertisement has not been reviewed by the Monetary Authority of Singapore. JPMorgan Chase Bank, N.A. is a national banking association chartered under the laws of the United States, and as a body corporate, its shareholder’s liability is limited.

With respect to countries in Latin America, the distribution of this material may be restricted in certain jurisdictions. We may offer and/or sell to you securities or other financial instruments which may not be registered under, and are not the subject of a public offering under, the securities or other financial regulatory laws of your home country. Such securities or instruments are offered and/or sold to you on a private basis only. Any communication by us to you regarding such securities or instruments, including without limitation the delivery of a prospectus, term sheet or other offering document, is not intended by us as an offer to sell or a solicitation of an offer to buy any securities or instruments in any jurisdiction in which such an offer or a solicitation is unlawful. Furthermore, such securities or instruments may be subject to certain regulatory and/or contractual restrictions on subsequent transfer by you, and you are solely responsible for ascertaining and complying with such restrictions. To the extent this content makes reference to a fund, the Fund may not be publicly offered in any Latin American country, without previous registration of such fund’s securities in compliance with the laws of the corresponding jurisdiction. Public offering of any security, including the shares of the Fund, without previous registration at Brazilian Securities and Exchange Commission— CVM is completely prohibited. Some products or services contained in the materials might not be currently provided by the Brazilian and Mexican platforms.

JPMorgan Chase Bank, N.A. (JPMCBNA) (ABN 43 074 112 011/AFS Licence No: 238367) is regulated by the Australian Securities and Investment Commission and the Australian Prudential Regulation Authority. Material provided by JPMCBNA in Australia is to “wholesale clients” only. For the purposes of this paragraph the term “wholesale client” has the meaning given in section 761G of the Corporations Act 2001 (Cth). Please inform us if you are not a Wholesale Client now or if you cease to be a Wholesale Client at any time in the future.

JPMS is a registered foreign company (overseas) (ARBN 109293610) incorporated in Delaware, U.S.A. Under Australian financial services licensing requirements, carrying on a financial services business in Australia requires a financial service provider, such as J.P. Morgan Securities LLC (JPMS), to hold an Australian Financial Services Licence (AFSL), unless an exemption applies. JPMS is exempt from the requirement to hold an AFSL under the Corporations Act 2001 (Cth) (Act) in respect of financial services it provides to you, and is regulated by the SEC, FINRA and CFTC under U.S. laws, which differ from Australian laws. Material provided by JPMS in Australia is to “wholesale clients” only. The information provided in this material is not intended to be, and must not be, distributed or passed on, directly or indirectly, to any other class of persons in Australia. For the purposes of this paragraph the term “wholesale client” has the meaning given in section 761G of the Act. Please inform us immediately if you are not a Wholesale Client now or if you cease to be a Wholesale Client at any time in the future.

This material has not been prepared specifically for Australian investors. It:

May contain references to dollar amounts which are not Australian dollars;

May contain financial information which is not prepared in accordance with Australian law or practices;

May not address risks associated with investment in foreign currency denominated investments; and

Does not address Australian tax issues.

Too Long at the Fair

Time to retire the US/Emerging Markets barbell for a while

[START RECORDING]

FEMALE VOICE: This podcast has been prepared exclusively for institutional wholesale professional clients and qualified investors only, as defined by local laws and regulations. Please read other important information, which can be found on the link at the end of the podcast episode.

MR. MICHAEL CEMBALEST: Good morning, everybody, and welcome to the May 2023 Eye on the Market podcast. This one’s called Too Long at the Fair. I have recommended to clients for well over a decade, actually since 2009, that they should overweight the United States and emerging markets and underweight Europe and Japan in their regional equity allocations. The excess returns from that kind of strategy, if implemented, have been enormous. But the time has come to retire this barbell for a while. I stayed too long at the fair, and I should’ve made this recommendation to put the barbell aside a few months when Europe was trading at a massive 35% P/E discount to the US. And a slightly brighter picture in Japan relative to China is another reason why it’s time to put this barbell aside.

So this month’s Eye on the Market goes into the detail; we have some charts. The barbell has actually done extremely well since 1988. It’s been 30 years that investors have benefitted from overrating the United States and emerging markets versus Europe and Japan. Most of that benefit has come from overweighting the US over Europe. The EM versus Japan thing has been profitable, but smaller and kind of hitor-miss over the last decade or so. And we have some charts in here that kind of illustrate that.

So first, why did this barbell perform so well since 2009 when we started to recommend it? We have a chart here that decomposes the reasons. And there’s five major factors. One is the outperformance of the dollar versus the euro. Another one is that US sector weights are higher in tech and healthcare and lower in financials, energy, industrials, and staples. And so there’s a sector benefit in the modern world to being overweight tech and healthcare. And then within sectors, US technology, consumer discretionary, and financial stocks have substantially outperformed their European counterparts. These five factors explain over 90% of the US outperformance since 2009.

Now what has changed over the last few months, since September of last year, Europe has outperformed the US by around 20%. Around two-thirds of that is simply due to the decline in the dollar. Now as we wrote last time, while we don’t think that the dollar’s reserve currency status is under serious threat, there is room on a cyclical basis for the dollar to decline, given its sharp rise versus other currencies. And there’s other bits and pieces in there, outperformance of European consumer discretionary stocks, a tiny bit of outperformance of European financials. But the vast majority of what’s happened over the last few months has been the change in the dollar.

And the other interesting thing is that since last fall, Japan has outperformed emerging markets by about 10%. And to me, what’s notable is that one of the factors there is a resurgence in M&A activity in Japan, which is unusual, and some of which is coming from foreign investors, which is even more unusual. And you have seen some of these deals, but Bain acquired Hitachi Metals, Evident, and Gelato Pique. KKR acquired Hitachi Transport; Fortress acquired Seven & I. All of these were multi-billion-dollar deals. A little bit more on Japan later, but the increase in leveraged buyout activity is kind of a big deal in Japan.

Now we’ve seen some arguments that suggest that while we’re in for another period like 2005 to 2007, where Europe crushed the US, that was kind of a weird period in Europe. There was an explosion of bank lending everywhere from Germany to Spain, Netherlands, Italy, France, and I don’t think that’s going to be repeating itself, so I think that’s kind of a silly argument. We have some charts in here that explain why.

The mistake that I made is that by not recommending this a few months ago, Europe is essentially a value play, when you look at the context of its heavy sector weightings to staples, financials, energy, and utilities. And everything has a price in the value market, right. And eventually price to earnings, price to book could get cheap enough that everything has a price. And I should have been paying more attention to how cheap Europe got. By September of last year, Europe’s P/E multiple hit the lowest level on record versus the US of around 35% P/E discount. And while there were valid concerns that all of us had about Europe’s energy situation, rising inflation, exposure to China, which was still in lockdown, investors were receiving an enormous discount for taking European equity exposure, and I should’ve been more focused on that.

Now how much can it rally? I think Europe’s outperformance is capped when you look at return on assets and return on equity. In almost every major sector, the US companies are more profitable than the European counterparts. But you’re getting paid a lot of money at a 30 to 35% P/E discount to take exposure to Europe.

And let me just spend a couple minutes on Japan. There’s been discussions about improved corporate governance in Japan for probably 20 years. But just over the last few years, it seems like the government is a little bit more serious in doing something about it. There’s been a record increase in stock buybacks. Sony’s spinoff and buyback is one example of that. And now the government is really going after the 50% of companies that trade below book value. They have to outline a plan to maximize shareholder value and comply with these new shareholder liquidity and director reforms. And the 10 to 20% of companies that don’t comply with the crossholding and free-float rules may face delisting. So there’s a little bit more teeth now.

And around half of Japanese companies have a lot of cash compared to less than 20% in the US and Europe. So there’s a lot of potential benefits from a corporate governance move into Japan that has real momentum behind it. And of course, positioning is low in Japan. I don’t think I’ve ever talked about Japan on this podcast, or several years since I’ve talked about Japan in the Eye on the Market.

So to wrap up, the valuation discount for Europe and Japan remains pretty high. There might be a little bit more legs left in this anti-barbell trade. I wouldn’t argue for a reverse barbell, which would be overweight Europe and Japan. And I don’t have that much conviction in Europe to do that. Europe has a long history of grasping defeat from the jaws of victory, and the ECB still has tightening to do. But I also think the US debt ceiling is going to be raised one way or another.

But the bottom line is that after an incredible 30-year run, and after an incredible 14-year run over which time we’ve been recommending it, I think the barbell’s best days are behind it for a little while. And investors should have more regional balance in their global equity portfolios, at least for now. So thank you very much for listening, and we will talk to you next time.

FEMALE VOICE: Michael Cembalest’s Eye on the Market offers a unique perspective on the economy, current events, markets, and investment portfolios, and is a production of J.P. Morgan Asset and Wealth Management. Michael Cembalest is the Chairman of Market and Investment Strategy for J.P. Morgan Asset Management and is one of our most renowned and provocative speakers. For more information, please subscribe to the Eye on the Market by contacting your J.P. Morgan representative. If you’d like to hear more, please explore episodes on iTunes or on our website.

This podcast is intended for informational purposes only and is a communication on behalf of J.P. Morgan Institutional Investments Incorporated. Views may not be suitable for all investors and are not intended as personal investment advice or a solicitation or recommendation. Outlooks and past performance are never guarantees of future results. This is not investment research. Please read other important information, which can be found at www.JPMorgan.com/disclaimer-EOTM.

[END RECORDING]