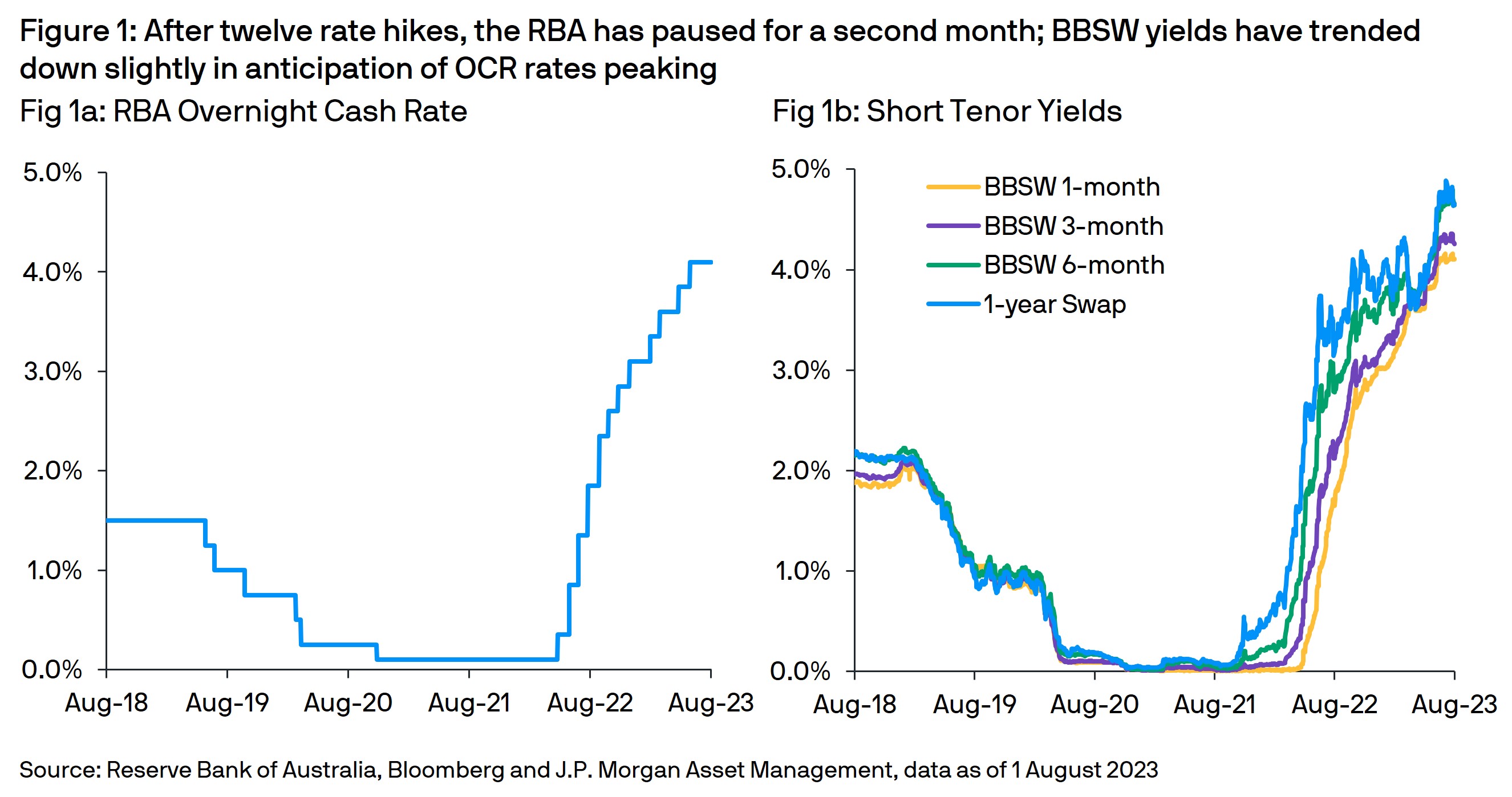

At its monetary policy meeting on 1 August 2023, the Reserve Bank of Australia (RBA) decided to leave the Overnight Cash Rate (OCR) unchanged (Fig 1) for a second month. This follows a cumulative 400bps of rate hikes over the previous fifteen months, which has taken base rates to a decade high of 4.10%. Explaining its decision, the RBA noted that “higher interest rates are working to establish a more sustainable balance… in the economy”, while “uncertainty surrounding the economic outlook” remains. The central bank also observed the recent decline in price pressures and updated economic forecasts that suggest inflation will return to target within a reasonable timeframe.

A wider path to a soft landing

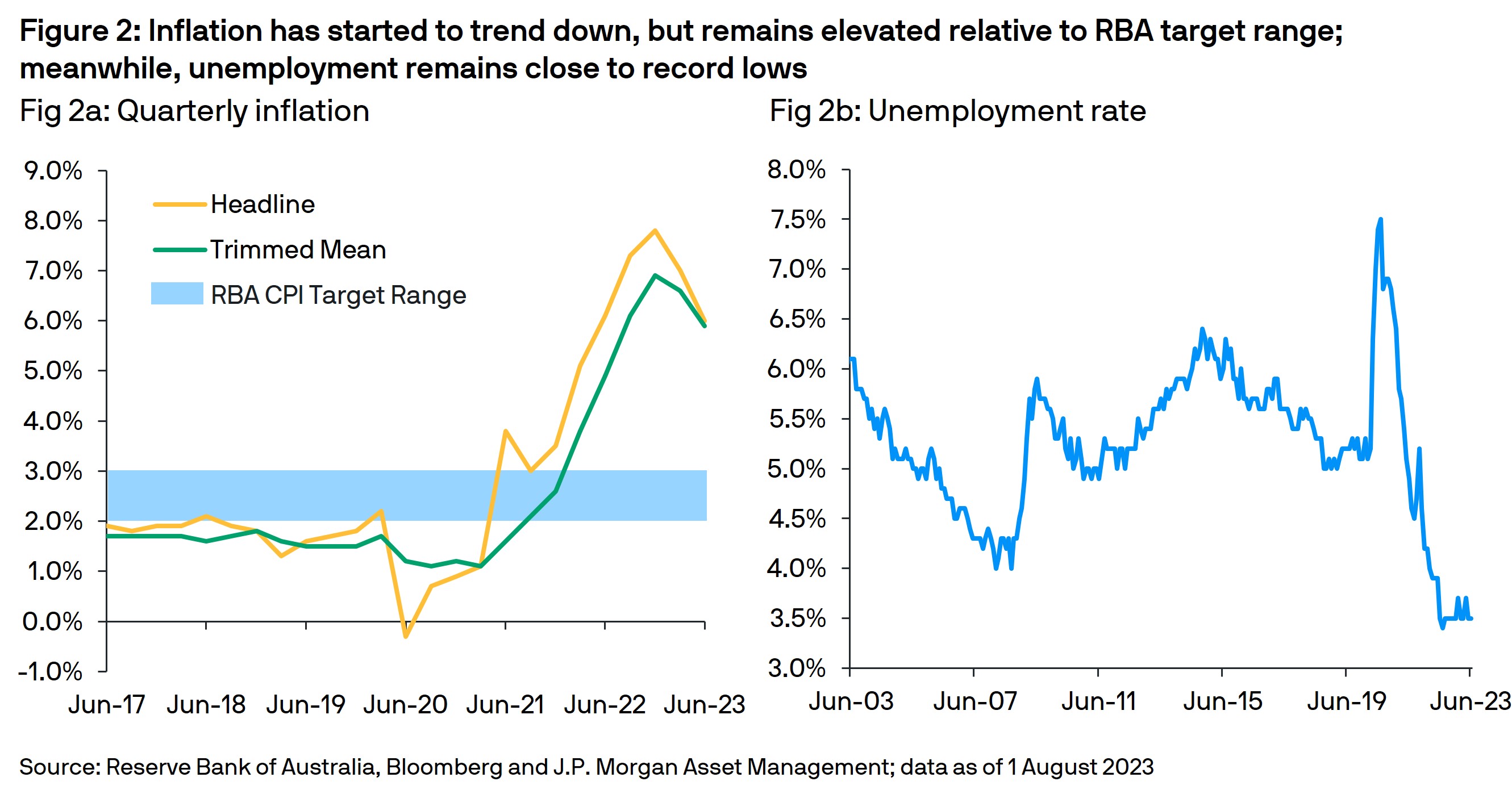

The second quarter inflation data was helpful news for the central bank – suggesting a wider path to their desired soft landing. The headline rate printed lower than expected, increasing by 0.8%q/q, slowing the annual pace to 6.0% from 7.0% previously. Core inflation also eased to 5.9%y/y, aided by lower food, housing and transportation costs. The latest RBA forecasts predict CPI will decline to 3.25% by the end of 2024 and “be back within the 2-3% target range in late 2025”. Concurrently, the impact of previous rate hikes is now visible in economic growth with household consumption slowing, manufacturing softening and construction moderating. The RBA suggests this “period of below trend growth is expected to continue for a while”, with the central bank predicting GDP will slow to 1.75% in 2024 before recovering slightly to 2.00% in 2025. Over time, this should reduce consumer demand, lessen labor shortages (employment is forecasted to increase to 4.5% by the end of 2024) and curtail wage growth – especially, as the RBA believes “medium term inflation expectations have been consistent with the inflation target”.

Nevertheless, the economy still faces multiple upside inflation risks that could upset the RBA’s optimistic narrative. The absolute level of core inflation remains elevated relative to the central bank’s 2-3% target range. Services inflation has proved persistently sticky, reducing the possibility of further sharp declines in core inflation, with the RBA observing “the prices of many services are rising briskly” while “rent inflation is also elevated”. Meanwhile, the unemployment rate has declined back towards 50-year lows with labor shortages and higher living costs encouraging faster wages growth. Finally, growing consumer expectations that interest rates are near a peak has encouraged a recovery in the property market – with house prices rising for the past five months from their February 2023 low.

Market Reaction

Following recent, less hawkish, RBA comments and the better-than-expected Q2-23 inflation data, markets had reduced the probability of an August rate hike from over 50% to less than 20%; although interestingly 18 out of 30 economists polled by Bloomberg still predicted a rate hike. Following the RBA’s announcement, market movements were relatively muted with the AUD declining slightly while bond yield dropped modestly across the curve. Market pricing of additional rate hikes has also fallen, with 26% probability of one additional hike by November to a peak rate of 4.26%.

Outlook

Keen to achieve a soft landing, the RBA leveraged the better than expected second quarter inflation data as justification to hold interest rates steady, while providing “further time to assess the impact of the increase in interest rates to date and the economic outlook”. Its latest economic forecasts also painted an optimistic picture of moderating economic growth allowing inflation to return to target. However, acknowledging the upside risks to inflation, the RBA was keen to affirm its commitment to “ensuring inflation returns to target” and noted that “some further tightening of monetary policy may be required”.

For AUD cash investors, the current high rates of return on short term investments and upward sloping yield curve continue to present relatively attractive investment opportunities. While the RBA confirmed it will remain data dependent, we believe that robust employment data and elevated inflation imply at least one further rate hike is likely. This suggests investors could consider pursing a cautious and diversified approach to cash investing.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.

09ok230208092222

NOT FOR RETAIL DISTRIBUTION: This communication has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.

This is a promotional document and is intended to report solely on investment strategies and opportunities identified by J.P. Morgan Asset Management and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. This document is confidential and intended only for the person or entity to which it has been provided. Reliance upon information in this material is at the sole discretion of the reader. The material was prepared without regard to specific objectives, financial situation or needs of any particular receiver. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are those of J.P. Morgan Asset Management, unless otherwise stated, as of the date of issuance. They are considered to be reliable at the time of production, but no warranty as to the accuracy and reliability or completeness in respect of any error or omission is accepted, and may be subject to change without reference or notification to you.

Investment involves risks. Any investment decision should be based solely on the basis of any relevant offering documents such as the prospectus, annual report, semi-annual report, private placement or offering memorandum. For further information, any questions and for copies of the offering material you can contact your usual J.P. Morgan Asset Management representative. Both past performance and yields are not reliable indicators of current and future results. There is no guarantee that any forecast will come to pass. Any reproduction, retransmission, dissemination or other unauthorized use of this document or the information contained herein by any person or entity without the express prior written consent of J.P. Morgan Asset Management is strictly prohibited. J.P. Morgan Asset Management or any of its affiliates and employees may hold positions or act as a market maker in the financial instruments of any issuer discussed herein or act as the underwriter, placement agent or lender to such issuer. The investments and strategies discussed herein may not be appropriate for all investors and may not be authorized or its offering may be restricted in your jurisdiction, it is the responsibility of every reader to satisfy himself as to the full observance of the laws and regulations of the relevant jurisdictions. Prior to any application investors are advised to take all necessary legal, regulatory and tax advice on the consequences of an investment in the products. Securities products, if presented in the U.S., are offered by J.P. Morgan Institutional Investments, Inc., member of FINRA. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities:

In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be. In Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919).

Malaysia, Philippines, Brunei, Thailand, Indonesia, India, Vietnam, Bhutan and Korea: This document is provided in response to your request. This document is for informational purposes only and does not constitute an invitation or offer to the public. This document including any other documents in connection are for intended recipients only and should not be distributed, caused to be distributed or circulated to the public. This document should not be treated as a prospectus or offering document and it has not be reviewed or approved by regulatory authorities in these jurisdictions. It is recipient’s responsibility to obtain any regulatory approvals and complying with requirements applicable to them.

People’s Republic of China: This document is private and confidential and is issued to you upon your specific request and is provided for your internal use and informational purposes only. It may not be photocopied, reproduced, circulated or otherwise distributed or redistributed to others. This document does not constitute an offer, whether by sale or subscription, in the People's Republic of China (the "PRC"). Any interests stated is not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC. Further, no legal or natural persons of the PRC may directly or indirectly purchase any beneficial interest therein without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

For materials distributed to wholesale clients in Australia, please note the following : Pursuant to ASIC Class Order 03/1102 and ASIC Class Order 03/1103 applicable to JPMorgan Asset Management (Singapore) Limited ("JPMAMSL") and JPMorgan Funds (Asia) Limited (“JPMFAL”) respectively, JPMAMSL and JPMFAL are exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 (Commonwealth)) in respect of the financial services provided by JPMAMSL or JPMFAL in Australia to wholesale clients. A copy of which may be obtained at the website of the Australian Securities and Investments Commission www.asic.gov.au. The class order exempts JPMAMSL and JPMFAL respectively from the need to hold an AFSL for financial services provided to Australian wholesale clients on certain conditions. Please note that JPMAMS is regulated by the Monetary Authority of Singapore (MAS) under the laws of Singapore, which differ from Australian laws. Similarly, JPMFAL is regulated by the Securities and Futures Commission (SFC) of Hong Kong under the laws of Hong Kong, which also differ from Australian laws.

If you would prefer not to receive these communications, you have the right to opt out. Please return email with unsubscribe in the subject line to your usual J.P. Morgan Asset Management client advisor.

Copyright 2023 JPMorgan Chase & Co. All rights reserved.