Week in review

- Bank of Japan maintained interest rate at 0.75%

- U.S. Fed maintained interest rate at 3.5-3.75%

- China RatingDog Manufacturing PMI declined to 50.3 in April

Week ahead

- U.S. April non-farm payrolls

- U.S. April unemployment rate

- China April imports and exports

Thought of the week

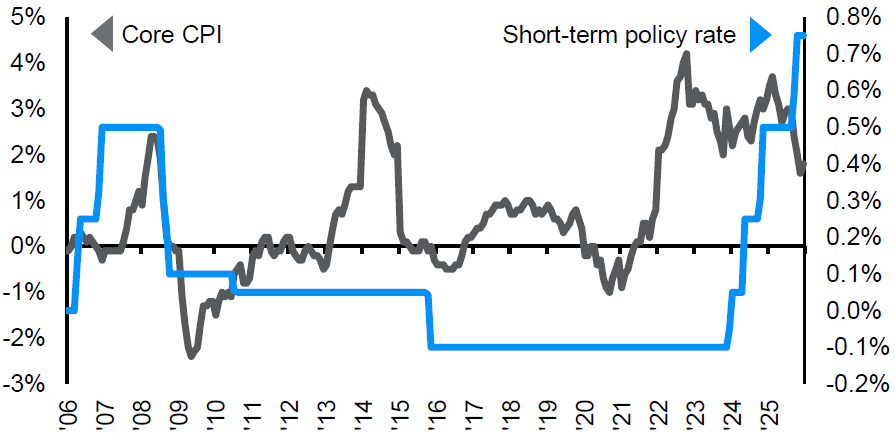

The Bank of Japan held its policy rate at 0.75%, though dissent widened to 6-3 as Nakagawa and Tamura joined Takata in voting for a hike. The Outlook Report factored in Middle East risks, revising growth forecasts down and inflation forecasts up, tilting the risk balance toward a stagflation scenario. Governor Ueda signaled a "hawkish skip," noting the likelihood of achieving the 2% price stability target has declined, while leaving the door open for a June or July hike if economic deterioration remains limited and upside price pressures persist. Markets reacted with the yen slipping, while equities fell and the JGB curve flattened. While the BOJ remains on a gradual normalization path, the pace and timing of future hikes will be highly sensitive to the evolution of Middle East tensions, their pass-through to energy prices and growth, and USDJPY dynamics, particularly as the yen is increasingly driven by global conditions and Fed policy.

Japan Core CPI YoY change and short-term policy rate

%

Source: FactSet, Bank of Japan, Ministry of Internal Affairs and Communications Japan, J.P. Morgan Asset Management. Data reflect most recently available as of 30/04/2026.

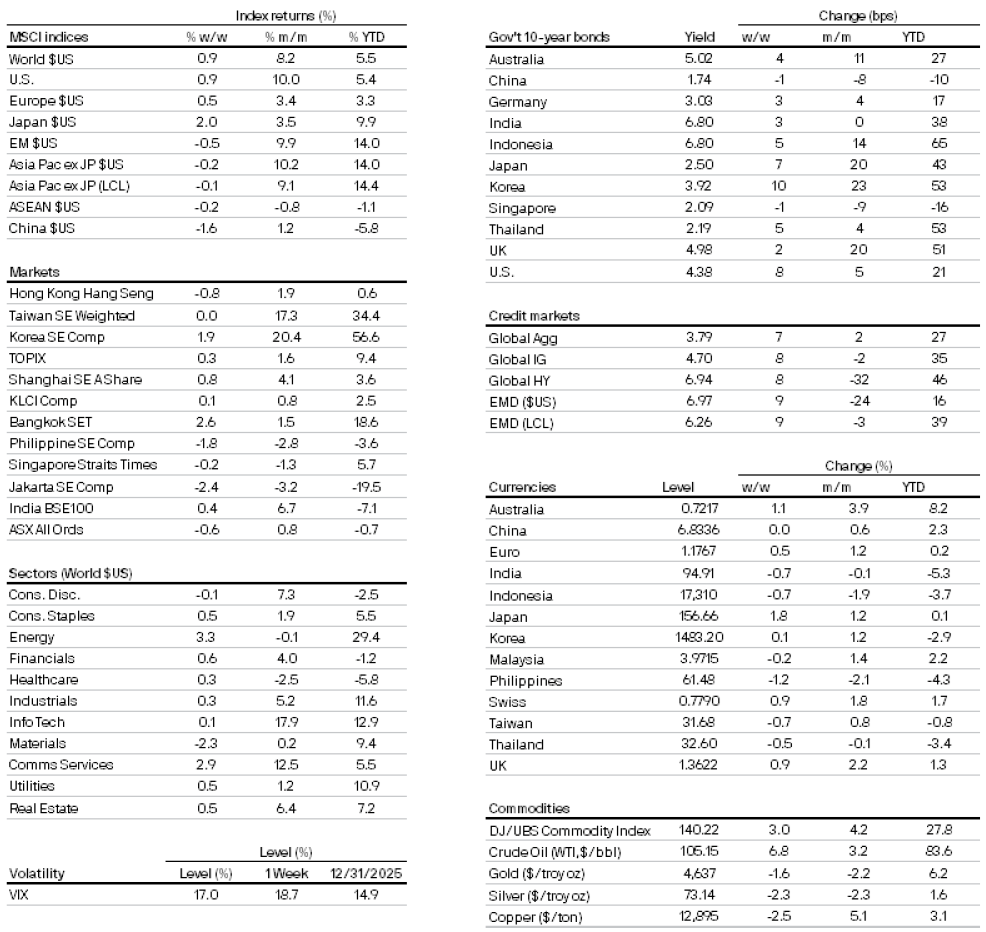

Market data

300a4900-f9d9-11e8-839f-fe2ee17e7f12

All returns in local currency unless stated otherwise.

Currencies’ return are based on foreign currencies per U.S. dollar. An appreciation of the foreign currency against the U.S. dollar would be positive and a depreciation of the foreign currency against the U.S. dollar would be negative.