Week in review

- ECB interest rate remains at 2.4%

- Japan inflation rate increased to 1.7% y/y in June

Week ahead

- U.S. interest rate decision

- Europe 2Q GDP growth rate

- U.S. GDP growth rate

Thought of the week

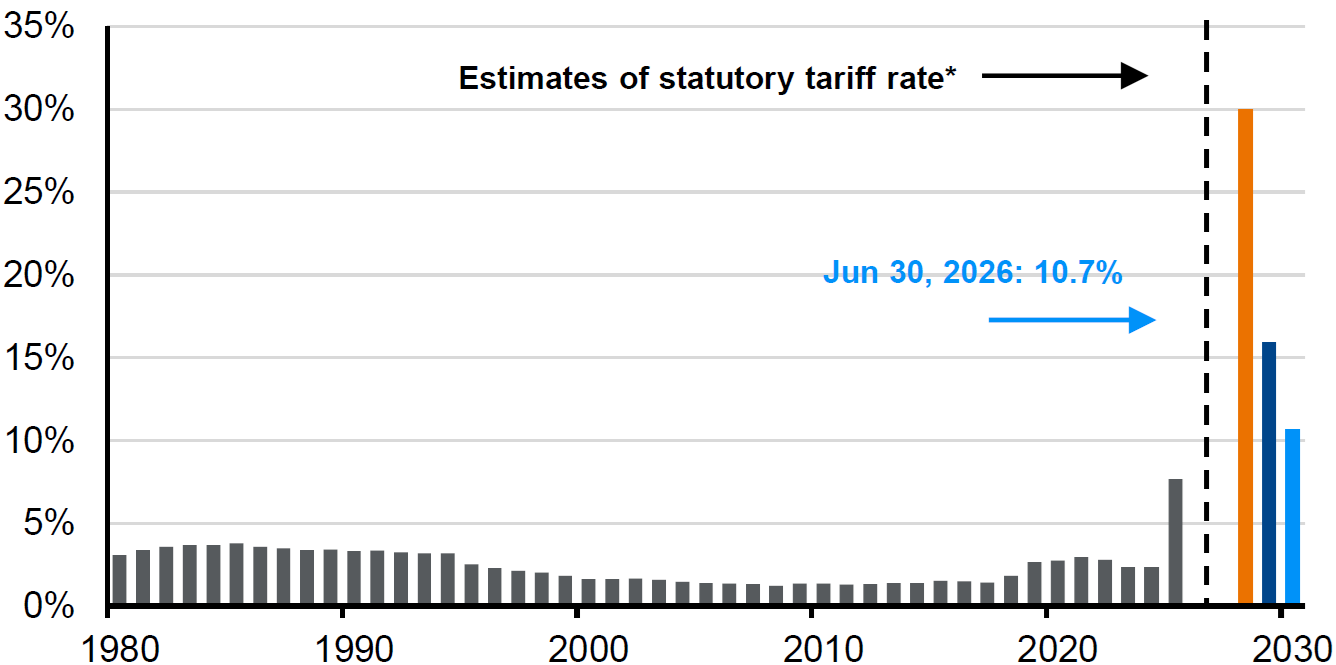

Fresh tariff action appears to be moving back to the center of the policy agenda, with potential new duties on a wide range of trading partners arriving as earlier temporary measures are set to expire. The significance lies less in any single tariff rate and more in the renewed uncertainty around global supply chains, inflation pass-through, and corporate margin planning. Broader trade restrictions could complicate the disinflation narrative if import costs rise, while sector-specific measures may create uneven pressure across industries and countries with large export exposure. However, some measures may be designed with grace periods, exemptions, or negotiated outcomes, limiting the immediate economic impact; larger multinational firms may also have more flexibility to adapt through agreements, sourcing shifts, or pricing power. Still, the direction of travel suggests trade policy could remain a persistent macro variable. Investors may be best served by monitoring how tariffs affect inflation expectations, earnings guidance, and central bank flexibility going forward.

Average tariff rate on U.S. goods imports for consumption

Duties collected / value of total goods imports for consumption

Source: U.S. Census Bureau, U.S. Department of Treasury, U.S. International Trade Commission, J.P. Morgan Asset Management. For illustrative purposes only. The estimated weighted average statutory U.S. tariff rate includes all tariffs that are currently in effect, not announced. Imports for consumption: goods brought into a market for direct use or sale in the domestic market. *Figures are based on 2024 import levels and assume no change in demand due to tariff increases. Import figures included in the table are from the U.S. Census Bureau. Estimates, projections and other forward-looking statements are based upon current beliefs and expectations. They are for illustrative purposes only and serve as an indication of what may occur. Given the inherent uncertainties and risks associated with forecasts, projections or other forward-looking statements, actual events, results or performance may differ materially from those reflected or contemplated. Data reflect most recently available as of 16/07/2026.

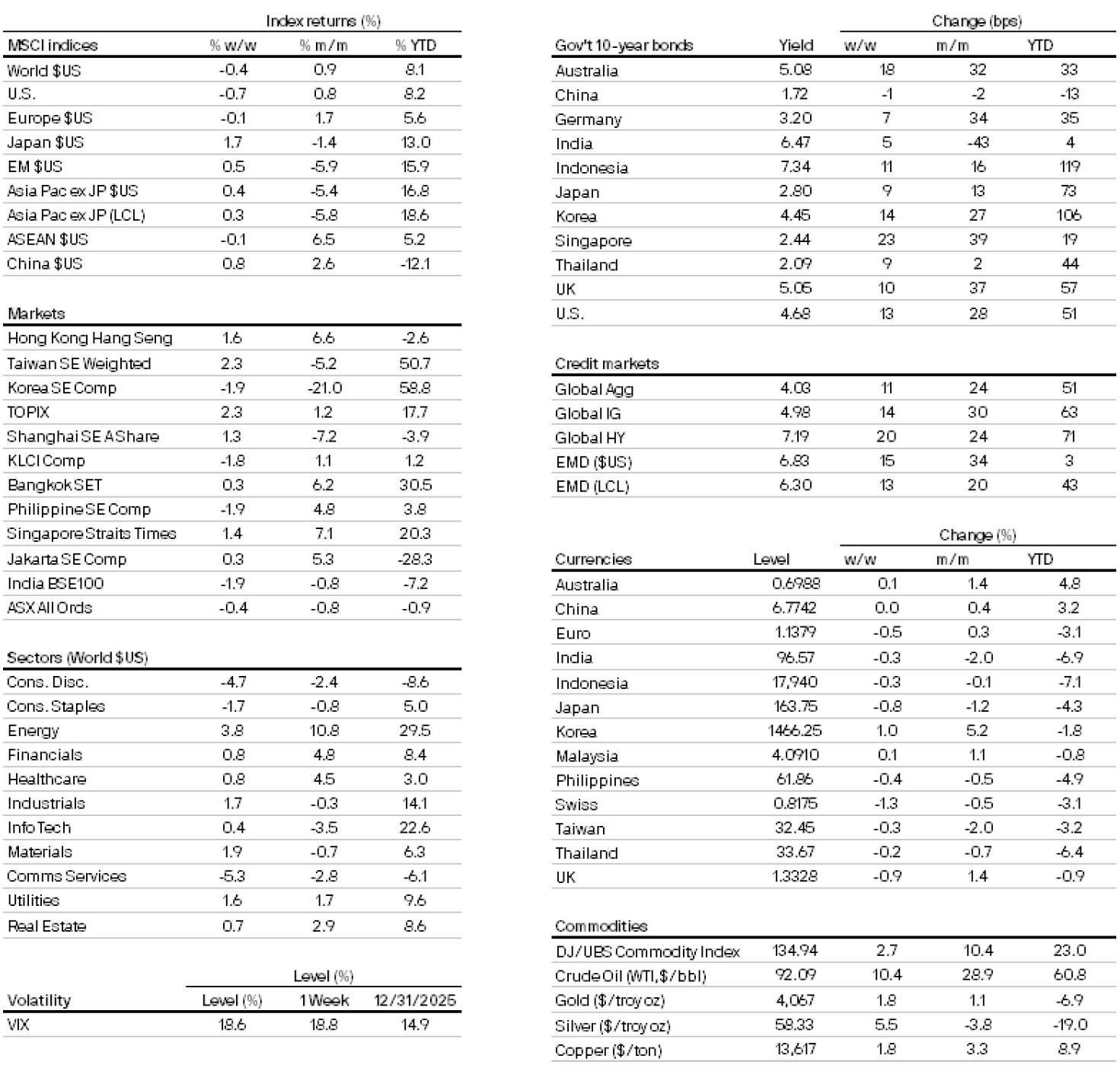

Market data

300a4900-f9d9-11e8-839f-fe2ee17e7f12

All returns in local currency unless stated otherwise.

Currencies’ return are based on foreign currencies per U.S. dollar. An appreciation of the foreign currency against the U.S. dollar would be positive and a depreciation of the foreign currency against the U.S. dollar would be negative.