You are about to enter the J.P. Morgan Asset Management website for UK Personal Investors, also known as UK retail clients.

Please read the following legal and regulatory information which applies to our company status, use of this website and information about any investment in our products referred to in this website (the "Site").

By using this Site, you agree to the placement of certain cookies on your computer – please read our cookie policy for more information.

Role Definition

Definitions for investor types

Advisers are professional investors who are authorised by relevant regulators to provide their clients with investment and/or pension advice.

Asset or Wealth Managers are financial planners, investment portfolio managers and other professional investors.

The 'Institutional' site is for pension schemes, consultants or other professional investors.

The 'Global Liquidity' site is for professional investors who are looking for liquidity investment opportunities.

Personal investors (also known as 'retail clients') are client organisations or individuals who cannot meet both (i) one or more of the professional client criteria laid down in Annex II to the Markets in Financial Instruments Directive (Directive 2004/39/EC), and (ii) one or more of the qualified investor criteria set out in Article 2 of the Prospectus Directive (Directive 2003/71/EC).

The personal investor category gives investors the greatest level of protection under the regulations and ensures investors get full information about any products they invest in.

If you are a retail investor but would like to be categorised as a professional investor, you should know that this is allowed but it would mean:

You could receive less information about our investments products and services; and

you wouldn't be entitled to receive a suitability report or appropriateness assessment in cases where they would be required for personal investors.

If you are a professional investor (also known as a 'professional client') but would like to be categorised as a personal investor, this is allowed but it doesn't necessarily mean you can refer any complaints to the Financial Ombudsman Service and you may not be eligible for compensation under the Financial Services Compensation Scheme.

Professional investors (also known as 'professional clients')

The definition of a professional client comes from the MiFID directive which provides definitions for professional and retail clients as well as eligible counterparties.

MiFID adopts two main categories of client: retail and professional. There is a separate and distinct third category for a limited range of business: eligible counterparty (ECP) has the lowest level of protection under MiFID.

Professional clients are those who may be deemed to possess the experience, knowledge and expertise to make their own investment decisions and properly assess the risks associated thereto. The list below taken from the official Journal of the European Union (L 145/44 EN Official Journal of the European Union 30.4.2004) should be understood as including all authorised entities carrying out the characteristic activities of the entities mentioned: entities authorised by a Member State under a Directive, entities authorized or regulated by a Member State without reference to a Directive, and entities authorised or regulated by a non-Member State:

Credit institutions

Investment firms

Other authorised or regulated financial institutions

Insurance companies

Collective investment schemes and management companies of such schemes

Pension funds and management companies of such funds

Commodity and commodity derivatives dealers

Locals

Other institutional investors

Large undertakings meeting two of the following size requirements on a company basis:

balance sheet total: EUR 20 000 000

net turnover: EUR 40 000 000

own funds: EUR 2 000 000

National and regional governments, public bodies that manage public debt, central banks, international and supranational institutions such as the World Bank, the International Monetary Fund (IMF), the European Central Bank (ECB), the European Investment Bank (EIB) and other similar international organisations

Other institutional investors whose main activity is to invest in financial instruments, including entities dedicated to the securitisation of assets or other financing transactions

Please note that the above summary is provided for information purposes only. If you are uncertain as to whether you can be classified both as a professional client under the Markets in Financial Instruments Directive and classed as a qualified investor under the Prospectus Directive then you should seek independent advice.

Terms of Use

1. General information

The information on this Site is approved for issue by JPMorgan Asset Management (UK) Limited, which is part of the J.P.Morgan Asset Management ("JPMAM") marketing group (hereafter referred to as ‘we’ or ‘us’), which sells investments, life assurance and pension products. It is authorised and regulated in the UK by the Financial Conduct Authority under registration number 122754.

This Site has been produced for information purposes only and the views contained in it are not to be taken as advice or a recommendation to buy or sell any investment. (Reliance upon information in the Site is at the sole discretion of the reader).

This Site provides information about J.P. Morgan investment funds ("JPM Funds"). This Site is strictly limited to information ends and is not allowed to be used for subscription or transactions of units/shares in JPM Funds.

Any research described in the Site has been obtained by us for our own purpose. The results of such research are being made available as additional information and do not necessarily reflect our views.

Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated our own at the date of the relevant content. They are considered to be reliable at the time of writing, may not be all-inclusive and their accuracy and any forecasts are not guaranteed. They may be subject to change without reference or notification to you.

This information should not be regarded as giving you legal, investment or tax advice about our products. If you are unclear about any of the information on this Site or its suitability for you, please contact your legal, financial or tax adviser, or an independent legal, financial or tax adviser before making any investment or financial decisions.

This Site should not be accessed by any person in any jurisdiction where (by reason of that person's nationality, residence or otherwise) the publication or availability of this Site is prohibited. In particular, this Site is reserved exclusively for non-US Persons*. The information in this Site is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

Messages that you send to us by e-mail may not be secure. We recommend that you do not send any confidential information to us by e-mail as it may be intercepted by a third party. If you choose to send any confidential information to us via e-mail you do so at your own risk with the knowledge that a third party may intercept this information and we do not accept any responsibility for the security or integrity of such information.

We will try to keep this site operational at all times. However, we cannot guarantee that this Site or any of the various features upon it will always be available.

The hyperlinks provided on this Site are only provided for information and convenience purposes. JPMorgan Asset Management (UK) Limited is not responsible for the content of external internet sites that link to or are accessible from this Site. JPMorgan Asset Management (UK) Limited does not assume any responsibility or liability with respect to any website accessed via this Site.

Prospective investors should consult their own professional advisers on the tax implications of making an investment in, holding or disposing of any JPM Fund and the receipt of distributions with respect to such a fund.

2. Privacy and cookie policies

Please refer to our Privacy and Cookie Policies via the footer link.

3. Where our funds are available for sale

The countries our funds are authorized for sale will depend upon your country of domicile for tax purposes. To the extent you have questions about your status, you should consult your financial or other professional advisor.

4. Key investment risks

It is important that you read the relevant documentation (funds prospectus, Key Investor Information Document ‘KIID’) before you invest in JPM Funds to ensure you understand the specific risks involved and to determine whether it is a suitable product for you. A copy of the funds prospectus, the Key Investor Information Document ‘KIID’, as well as the annual and semi annual reports of the JPM Funds are available free of charge upon request from JPMorgan Asset Management (UK) Limited.

The value of shares/units of JPM Funds and any income from them can go down as well as up and you may not get back all that you have invested.

Estimates of future returns or indications of past performance on this Site are for information purposes only and should not be construed as a guarantee of current or future returns or performance.

Exchange rate changes may cause the value of underlying overseas investments to go down as well as up. Changes in currency rates of exchange may have an adverse effect on the value or income (if any) of the JPM Funds.

When investing in emerging market funds, emerging markets may be more volatile and the risk to your capital is greater.

The level of tax benefits and liabilities will depend on individual circumstances and may be subject to change in the future.

5. Combating financial crime

We are committed to combating financial crime and the prevention of money laundering. Accordingly we may need to verify your identity and carry out appropriate security checks.

6. Company information

J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 288553. Registered address: 25 Bank St, Canary Wharf, London E14 5JP, United Kingdom.

JPMorgan Asset Management (Europe) Société à responsabilité limitée, has its registered offices at 6, route de Trèves, L-2633 Senningerberg, Luxembourg.

7. Legal information

We believe that the information contained on this Site is accurate as at the date of publication. We cannot guarantee the accuracy, suitability or completeness of any such information or the availability of the Site. We accept no liability for any data transmission errors such as data loss or damage or alteration of any kind. Accordingly JPMorgan Asset Management (UK) Limited excludes any liability for any loss and/or damage (direct or consequential) arising from the use of any part of this Site.

All copyright, patent, intellectual and other property in the information contained in this Site is held by JPMorgan Asset Management (UK) Limited, unless otherwise indicated. No rights of any kind are licensed or assigned or shall otherwise pass to persons accessing this information. You may download or print copies of the reports or information contained within this Site for your own private non-commercial use only, provided that you do not change any copyright, trade mark or other proprietary notices; all other copying, reproducing, transmitting, distributing or displaying of material on this Site (by any means and in whole or in part) is prohibited.

* US Person includes, but is not limited to, a person (including a partnership, corporation, limited liability company or similar entity) that is a citizen or a resident of the United States or is organised or incorporated under the laws of the United States. Certain restrictions also apply to any subsequent transfer of Shares in the United States or to US Persons. Should a Shareholder become a US Person and such US Person is not compulsory redeemed, such US Person may be subject to US withholding taxes and tax reporting.

Accessibility Statement

In the creation of this website, J.P. Morgan Asset Management (JPMAM) is committed to making the content accessible to the widest possible audience. Our aim is to ensure that web pages available on this site comply with Priority 1 and a number of Priority 2 items of the W3C Web Content Accessibility Guidelines and best practice recommendations as stated by the Web Accessibility Initiative.

Our goal of continuous improvement means that we regularly review pages and documents to upgrade any legacy content to comply with current accessibility standards.

Pages are created using recognised structure such as emphasis and page headers.

Design is controlled using stylesheets allowing for the control of font size and more.

Images that contain important information will have appropriate alternative text.

Text size can be controlled through your chosen web browser, please consult the browser help documentation for more information.

A site map is provided to assist with site navigation and structure.

Adobe Acrobat Portable Document Format (PDF) Files

If you are using assistive technologies and are unable to access the contents of PDF documents, Adobe Systems, Inc., provides a free translation service through their Adobe Access web pages which will translate PDF files to web pages (HTML documents).

For pages that are not viewed directly from the internet, Adobe Access has a free downloadable accessibility plug-in for use with the latest versions of the Adobe Acrobat Reader for virtually all operating systems. This plug-in allows access to PDF documents with assistive technologies. Please visit the Adobe Access web site for further information.

Browser compatibility

These pages are designed for modern web browsers, but should be accessible in all browsers. This includes simple text browsers and adaptive browsers. The pages may not appear the same in old browsers or browsers that do not follow internet standards, though the information should still be accessible.

Contact us

If you require any of the information available on this site in a different format, have any comments or suggestions to enhance your experience, or require assistance with a particular document or page, please contact us with your enquiry.

J.P. Morgan Asset Management’s website and/or mobile terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its terms, privacy and security policies to see how they apply to you. J.P. Morgan Asset Management isn’t responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the J.P. Morgan Asset Management name.

The US stock market is being supported by better-than-expected company profits, a pick-up in economic growth and prospects for interest rate cuts later in the year. Nevertheless, we believe it is important to stay mindful of the risks, using an active investment approach to tap into higher quality opportunities created by the current wide dispersion in valuation and performance across sectors.

The outlook for US stocks remains constructive

US stocks recorded a strong first quarter of 2024, with the S&P 500 index registering price gains of over 10% and 22 record highs in the three months to 31 March 20241. For investors that have so far stayed on the sidelines, many could be wondering if they have missed an attractive opportunity. Others may question if the rally is sustainable. In our view, we believe US stocks are in a sweet spot, supported by historical performance signals, a positive economic backdrop and robust corporate earnings growth.

1. History suggests strength leads to more strength

Historical data suggests that there is no clear advantage or disadvantage of investing in US stocks at record highs relative to any other time. Since 1970, the average 12-month price return of the S&P 500 index after reaching an all-time high has been 9.1%, while the average price return from investing on all other days stands at 8.7%2.

Historically, investing at all-time highs has not meaningfully impacted longer-term returns

Source: Haver Analytics, J.P. Morgan Asset Management. Data as of 06.02.2024.

2. Positive economic backdrop

The outlook for the US economy remains constructive. Despite fears of recession amid a sharp rise in interest rates and a short-lived regional banking crisis, the US economy still grew by more than 3% in the fourth quarter of 20233. Crucially, the US consumer has remained resilient, supported by record low unemployment and higher real wage growth as inflation has cooled. The wealth effect from rising asset prices, such as equities and housing, could continue to support consumer spending as wealthier consumers tend to save less and spend more. With consumption accounting for around 70% of US gross domestic product (GDP)4, a resilient consumer presents a solid foundation for continued economic growth, albeit probably at a slower pace from last year.

US consumers have remained resilient, supported by a low unemployment rate and rising wages

Source: Bureau of Labor Statistics, Federal Reserve Economic Data (FRED), J.P. Morgan Asset Management. Data as of 31.03.2024. Wage growth is calculated from the wages of private production and non-supervisory workers, seasonally adjusted. Private production and non-supervisory jobs represent just over 80% of total non-farm jobs.

Potential interest rate cuts later in the year could provide some additional tailwinds. although policymakers have recently trimmed rate cut projections for 2024 and 20255. Nevertheless, the avoidance of recession and a pick-up in economic activity, coupled with the potential for some monetary easing later this year, could present a constructive backdrop for US equities. In the 44 years since 1980, there have been 14 non-recession years when the Federal Reserve has cut interest rates at least once2. Price returns for the S&P 500 index were positive for 13 of those 14 years – or 93% of the time – with an average price gain of 15.6%2.

3. Corporate earnings paint a positive picture

The S&P 500 index is expected to record earnings-per-share growth of around 11%6 this year, which represents a clear acceleration from 2023’s more muted performance. Ebbing recession risks, moderating inflation and potential interest rate cuts could buoy earnings growth and, by extension, broaden equity returns following the technology-dominated rally in 2023 on the back of optimism about generative artificial intelligence (AI). A broader and more inclusive rally that covers a meaningful share of companies beyond just the largest tech names could lead to healthier and more sustainable gains for US stocks.

Earnings continue to paint a positive picture, with market consensus expecting double-digit growth in 2024 and 2025

Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Data as of 31.03.2024. Historical EPS levels are based on annual pro-forma earnings per share. 2024F and 2025F EPS growth are based on consensus analyst estimates for each calendar year. F: Forecast. Past performance is not indicative of future returns. Forecasts/ Estimates may or may not come to pass.

Take account of the risks with an active approach

While the backdrop for US equities appears constructive, investors should bear in mind the downside risks presented by a slowing global economy, a presidential election cycle, elevated geopolitical and supply chain risks, moderating but stickier inflation, and the economic impact of prolonged higher interest rates. These factors could trigger periodic bouts of volatility in the US equity market.

At the same time, not all companies are created equal, and the risks facing different sectors and industries could vary widely. Investors therefore should look to stay selective and discerning, with a focus on quality assets with sound fundamentals.

A rigorous, bottom-up, stock selection approach could be useful to separate the wheat from the chaff. Position sizing and active allocation will also matter to optimise longer-term outcomes as investment prospects can change quickly in fast-moving markets.

JPMorgan American Investment Trust | JAM

JAM employs a flexible, bottom-up approach to seek out high conviction growth and value ideas in a portfolio of approximately 40 stocks7. The portfolio’s value ideas are focused on quality franchises that exhibit consistent and sustainable cash flows, while growth ideas are focused on companies with robust yet underappreciated growth potential.

By combining these complementary investment styles – namely value and growth – JAM has the flexibility to seek out attractive opportunities from an expanded universe of US stocks that stretch well beyond the S&P 500 index7.

1. Source: Bloomberg, J.P. Morgan Asset Management. Data as of 31.03.2024.

2. Source: J.P. Morgan Asset Management. “Should investors be bullish or bearish on US equities?” Published 09.02.2024.

3. Source: US Bureau of Economic Analysis, J.P. Morgan Asset Management. Data as of 31.01.2024.

4. Source: US Bureau of Economic Analysis, FactSet, J.P. Morgan Asset Management. “Guide to the Markets (US) 2Q 2024”. Data as of 31.03.2024.

5. Source: Federal Reserve. “Summary of Economic Projections”. Published 20.03.2024.

6. Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Data as of 31.03.2024. Historical EPS levels are based on annual pro-forma earnings per share. 2024F and 2025F EPS growth are based on consensus analyst estimates for each calendar year.

7. Please refer to the fund’s offering documents for further details on its objectives. The manager seeks to achieve its stated objectives and there is no guarantee they will be met. Actual account allocations and characteristics may differ. Holdings, duration, allocations or exposure in actively portfolio managed portfolios are subject to change from time to time. Investments involve risks. Not all investments, strategies or ideas are suitable for all investors. Investors should make their own evaluation or seek independent advice and review offering documents carefully prior to making any investment.

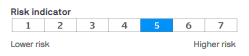

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period.

Investment objective

The Company aims to achieve capital growth from North American investments by outperformance of the Company's benchmark, the S&P500 Index, with net dividends reinvested, expressed in sterling terms. The Company emphasises capital growth rather than income and when appropriate may have exposure to smaller capitalisation companies. The Company's gearing policy is to operate within a range of 5% net cash to 20% geared in normal market conditions. Gearing may magnify gains or losses experienced by the Company.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained in English from JPMorgan Funds Limited or at www.jpmam.co.uk/investmenttrust. This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.