More than a hundred years of US financial market data consistently tells us that smaller companies outperform larger companies in the long run. But over the last decade, the opposite has been true, with large caps significantly outperforming. With US smaller companies expected to return to the ascendancy, we look at the reasons why it could now once again make sense to invest in the heart of America.

In the US, a thriving small cap sector is often cited as a key ingredient of the country’s long-term economic success. While smaller companies often come with higher associated risks, America’s small cap market is particularly entrepreneurial, diverse, and under-researched, —characteristics that have historically made it a rewarding market for those investors with long time horizons.

The Magnificent Seven effect

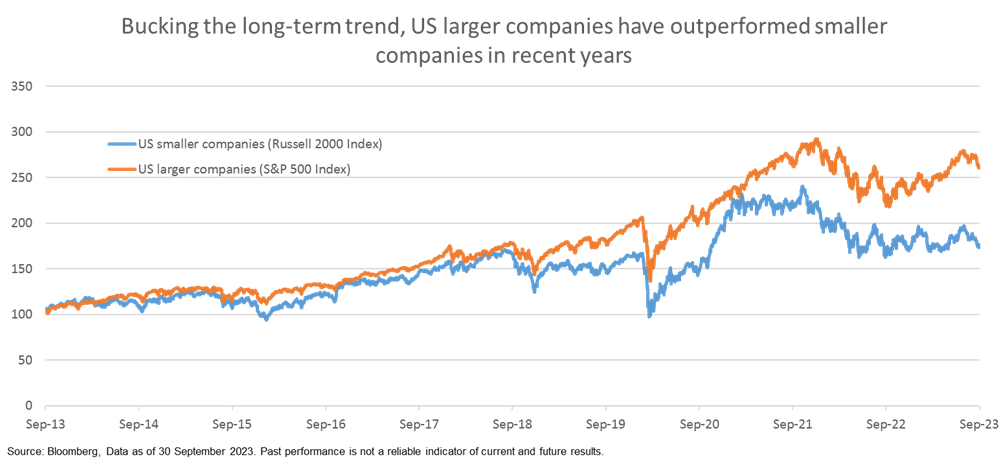

To understand the outlook for US smaller companies from here, it is helpful to explain the reasons why large caps have outperformed over the last 10 years. One major reason is that the US stock market has come to be dominated by a handful of increasingly large technology companies. Investors may remember the acronym “FAANG”, which stands for Facebook, Apple, Amazon, Netflix and Google. The term that has come to epitomise the phenomenon of large cap outperformance, particularly in the period leading up to and just after the Covid pandemic. In 2023, a similar trend with the Magnificent Seven, Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla was driving the majority of market returns. These seven businesses alone accounted for more than a quarter of the entire S&P 500 Index at the end of the third quarter 2023.

During this period, US small caps did well in absolute terms, with the Russell 2000 Index (a widely used benchmark for US smaller companies) delivering an annualized return of 5.6% in the ten years to 31 October 2023. But, as the chart below illustrates, they were somewhat in the shadow of the 11.2% annualized return in the S&P 500 Index as the effect of several mega cap stocks continued to unfold.

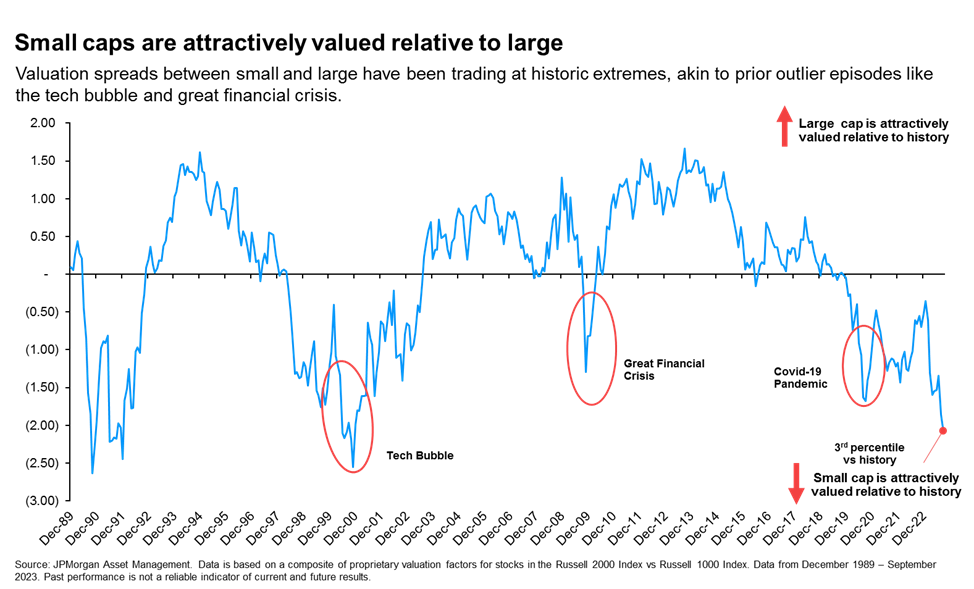

Small cap valuations are now supportive

While the dynamic of larger company outperformance continued so far in 2023, it might indicate a shift to a potentially better period for US smaller companies going forward. Having underperformed the S&P 500 Index in eight of the past 12 years, valuations in the Russell 2000 Index now appear attractive. In fact, they have only been cheaper 3% of the time over the last 33 years (based on J.P. Morgan Asset Management research). This valuation level is similar to prior periods, such as the tech bubble in the 1990s and the great financial crisis in 2008. Subsequent performance coming out of those periods was very favourable for US smaller companies for several years.

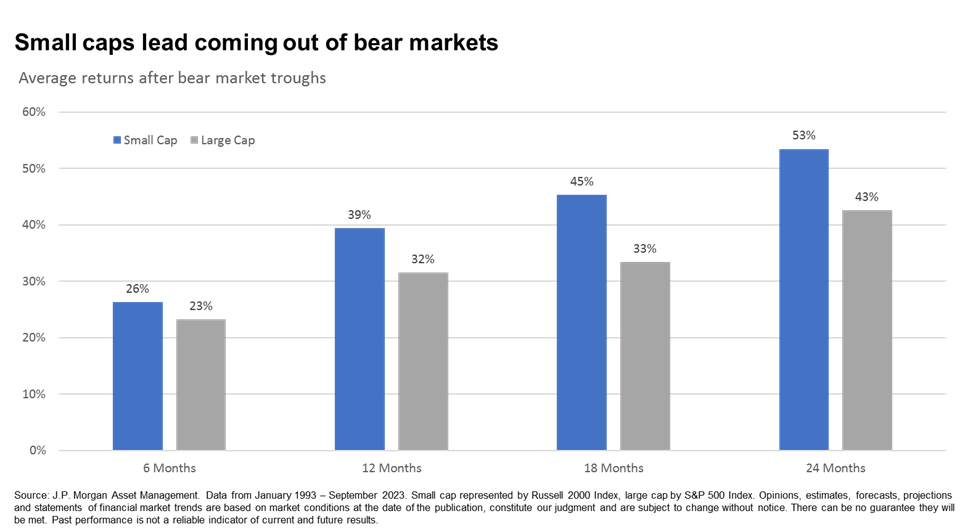

Smaller companies do well when markets turn

The promising backdrop for US small caps also includes an improving earnings picture in the face of elevated, but declining inflation coupled with higher interest rates. US smaller companies have often done well in such conditions.

Clearly, we still face some economic challenges, which should not be underestimated. The risk of a recession in the US in the next year may have receded somewhat in recent months as shelter, food and energy prices have declined, but higher interest rates continue to cause problems in some parts of the global economy.

Importantly, smaller companies tend to outperform as the US stock market emerges from a downturn. Once investors have some clarity about the health of the US economy, we could see the early stages of a rewarding small cap cycle.

Conclusion

The outlook for US smaller companies perhaps looks more encouraging now than it has for several years, particularly when viewed with the long-term horizons that ISA investors should apply. With valuations low and growth prospects tentatively improving, it may well be worth considering adding some exposure to US small caps within your ISA portfolio.

The JPMorgan US Smaller Companies Investment Trust plc offers an attractive way to access this opportunity. The trust is managed by a team of specialist investors with an average of 21 years’ industry experience between them, and a strong long-term track record in the US small cap market.

The managers look for well-managed, cash-generative businesses that enjoy an enduring competitive advantage and attractive growth prospects. These businesses represent the true spirit of the US economy, where underappreciated growth opportunities are abundant. That is why we believe an investment in the JPMorgan US Smaller Companies Investment Trust plc represents a rare opportunity to…

…invest in the heart of America.

The JPMorgan US Smaller Companies Investment Trust (JUSC) provides access to potentially fast growing smaller US stocks. The investment approach seeks out well-run companies with a record of attractive and sustainable profit.

Past performance is not a guide to current and future performance. The value of your investments and any income from them may fall as well as rise and you may not get back the full amount you invested.

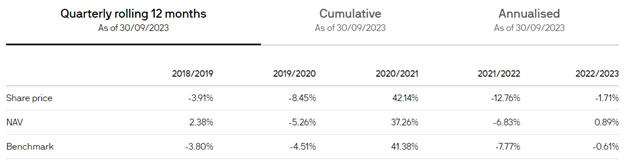

Source: J.P. Morgan Asset Management/Morningstar. Net asset value performance data has been calculated on a NAV to NAV basis, including ongoing charges and any applicable fees, with any income reinvested, in GBP. NAV is the cum income NAV with debt at fair value, diluted for treasury and/or subscription shares if applicable, with any income reinvested. Share price performance figures are calculated on a mid-market basis in GBP with income reinvested on the ex-dividend date.

The performance of the company's portfolio, or NAV performance, is not the same as share price performance and shareholders may not realise returns which are the same as NAV performance.

Benchmark source: The S&P 500 Index (£) (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and have been licensed for use by JP Morgan Chase Bank N.A. Copyright © 2023. S&P Dow Jones Indices LLC, a subsidiary of S&P Global, Inc., and/or its affiliates. All rights reserved. Comparison of the Company's performance is made with the benchmark. The benchmark is a recognised index of stocks which should not be taken as wholly representative of the Company's investment universe. The Company's investment strategy does not follow or track this index and therefore there may be a degree of divergence between its performance and that of the Company.

Indices do not include fees or operating expenses and you cannot invest in them.

*Past performance is not a reliable indicator of current and future results.

1Small caps lead coming out of bear markets. Source: J.P. Morgan Asset Management. Data from January 1993 – November 2022. Small cap represented by Russell 2000 Index, large cap by S&P 500 Index.

Investment Objective: The Company aims to provide investors with capital growth by investing in US smaller companies that have a sustainable competitive advantage. The Company focuses on owning equity stakes in businesses that the manager believes trade at a discount to intrinsic value, with strong management teams. The Company has the ability to use borrowing to gear the portfolio within a range of 5% net cash to 15% of net assets. Key Risks: Exchange rate changes may cause the value of underlying overseas investments to go down as well as up. External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions. This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down. This Company invests in smaller companies which may increase its risk profile. The share price may trade at a discount to the Net Asset Value of the Company. The single market in which the Company primarily invests, in this case US, may be subject to particular political and economic risks and, as a result, the Company may be more volatile than more broadly diversified companies.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not reliable indicators of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. Investment is subject to documentation. The Annual Reports and Financial Statements, AIFMD art. 23 Investor Disclosure Document and PRIIPs Key Information Document can be obtained in English from JPMorgan Funds Limited or at www.jpmam.co.uk/investmenttrust. This communication is issued by JPMorgan Asset Management (UK) Limited, which is authorised and regulated in the UK by the Financial Conduct Authority. Registered in England No: 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

Summary Risk Indicator:

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period.

095a230711185059