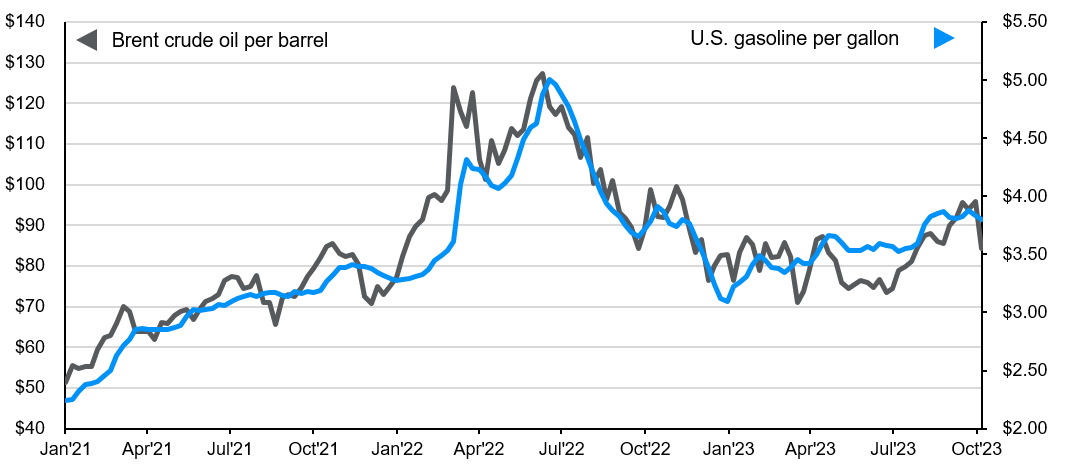

Oil prices are up sharply since hitting a recent low in June. By the end of September, Brent crude had risen from $72 per barrel to a 2023 high of $96, with the outbreak of violence in the Middle East triggering another spike in oil prices in early October.

Higher fuel and energy costs may not have an impact on the current “higher for longer” stance of central banks. However, if rising oil prices hit consumer spending, they may serve as a reminder to policymakers to be mindful of the downside risk to growth.

Reduced supply and rising demand have driven oil prices higher

The latest run up in oil prices reflect constraints on supply and rising demand. On the supply side, on 5 September Saudi Arabia extended its 1 million barrels per day cut in production for the rest of the year, alongside Russia’s 300,000 barrels per day reduction. The production cuts are aimed at lifting oil prices to support fiscal revenues. At the same time, the dramatic drop in the US strategic oil reserve – which has served as an additional buffer against external oil supply shocks in the past – has added to supply concerns.

On the demand side, meanwhile, tight oil supplies have been exacerbated by stronger-than-anticipated oil demand, which has grown sharply in 2023, driven by China. Global demand for oil expanded by 2.1million barrels per day in the first eight months of the year. Despite China’s lacklustre economic recovery, demand for transport-related fuel has been strong as domestic travel restrictions have been lifted.

More recently, the potential role of Iran and other Middle Eastern nations in the Israel-Hamas conflict has sparked further oil supply concerns. While Iran has so far denied direct knowledge of the attack on Israel, Tehran has been a supporter of Hamas. The oil market could potentially be impacted by the stronger enforcement of the ban on Iranian oil exports, or via disruption in the Strait of Hormuz, a critical shipping channel. While these risks appear low for now, they deserve monitoring as events continue to develop.

Some supply concerns have been eased as many oil producing countries – both members of the Organization of the Petroleum Exporting Countries (Opec) and non-Opec members – have steadily raised their own production. This supply response, and expectations for a possible slowdown in the global economy in the next 12 months, could help to cap oil prices. However, geopolitics is once again the source of uncertainty in the weeks and months ahead.

How may central banks react?

The rise in energy prices since June has prompted concerns that central banks may keep interest rates higher for longer to tame inflation. In the US, the Federal Reserve is indeed advocating a higher-for-longer interest rate policy, although higher energy prices may have less to do with this stance. Since hitting a high of $4.35 per gallon in June, the average US gasoline price has since settled at around $4.26, which is still about 3% lower than a year ago, and 22% lower than the June 2022 peak.

CRUDE OIL AND US GASOLINE PRICES

Energy prices are also unlikely to be influenced by monetary policy, since they are largely driven by the global supply and demand situation. Policymakers would instead need to take into account the possible drop in spending on discretionary items if households need to allocate more of their disposable income to gasoline and fuel. Hence, high oil prices could be seen as a tax on growth instead of a source of inflation.

Higher energy costs could, however, be more of a challenge for selected emerging market economies. Emerging market households typically spend a higher proportion of their income on fuel and food, so rising costs would likely have a greater impact on headline inflation and also have a greater negative impact on incomes. Trade deficits could also widen in oil-importing nations, which could place downward pressure on currencies and force central banks to raise rates to stabilise foreign exchange markets.

Investment implications

Conflict in the Middle East could push oil and energy prices up in the near term, which in turn would also push food prices higher given the knock-on effects on fertiliser prices and transportation costs. While the immediate impact would be reflected in headline rates of inflation around the world, the longer-term outcome would likely be felt by the consumer, in terms of lower discretionary spending, and by lower profit margins for companies in sectors that rely on commodities.

Fiscal support could also play an important role. With elections on the cards in a number of countries in 2024 (the US, Mexico, India, Indonesia, Taiwan and the UK to name a few), the increase in the cost of living is already high on the agenda of many voters. A renewed surge in fuel prices could prompt governments to either tap strategic reserves, or to try to dampen the impact on the general public via fiscal support where appropriate.

Overall, an uncertain outlook reinforces our emphasis on fixed income (government bonds and investment grade corporate debt), as well as high quality equities.

This is a marketing communication. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and may be subject to change without reference or notification to you.

The value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass.

J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy.

This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

094t231910152316