The EU TR is being integrated into the disclosure obligations set out by the EU SFDR. A firm is expected to reflect its minimum alignment to the EU TR alongside EU SFDR considerations. In addition, both Article 8 and Article 9 EU SFDR financial products need to disclose the degree to which they are committed to making sustainable investments, referencing both the EU SFDR and EU TR standards.

Under the EU SFDR, “sustainable investment” broadly means an investment in any economic activity that contributes to an environmental and/or social objective, provided that such investments do not significantly harm any of those objectives and that investee companies follow good governance practices.

Under the EU TR, a “sustainable investment” (being aligned to the EU TR) means specifically an investment in any economic activity that contributes to one of the six environmental objectives recognised by the regulation, on the condition that the investment meets the four-step due diligence standards outlined earlier.

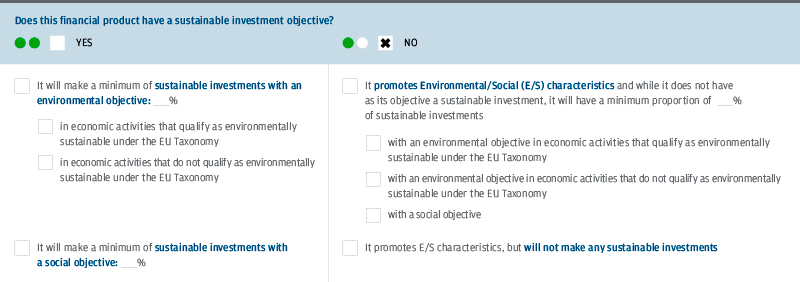

Integrating EU TR considerations into an EU SFDR Article 8 product

Source: Final Report on Draft Regulatory Technical Standards, Joint Committee of the European Supervisory Authorities, 22 October 2021.

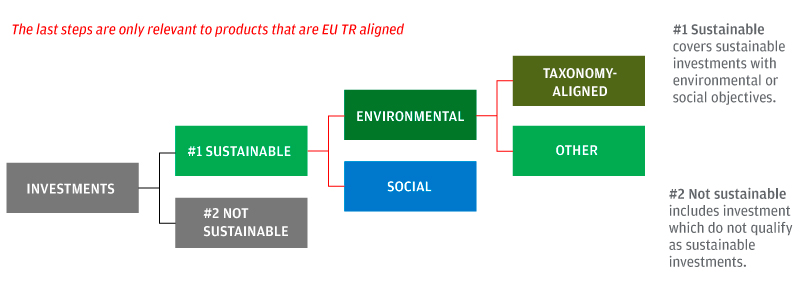

How the EU TR is considered in an EU SFDR Article 9 product

Source: Final Report on Draft Regulatory Technical Standards, Joint Committee of the European Supervisory Authorities, 22 October 2021.

Source: Final Report on Draft Regulatory Technical Standards, Joint Committee of the European Supervisory Authorities, 22 October 2021.

The Article 8 and Article 9 disclosures will provide investors with a detailed understanding of the sustainable investment commitments of financial products via precontractual (ex-ante) disclosure obligations, such as a prospectus. Investors will also be able to see how financial products fared in terms of those commitments via periodic reporting (ex-post) disclosure obligations.

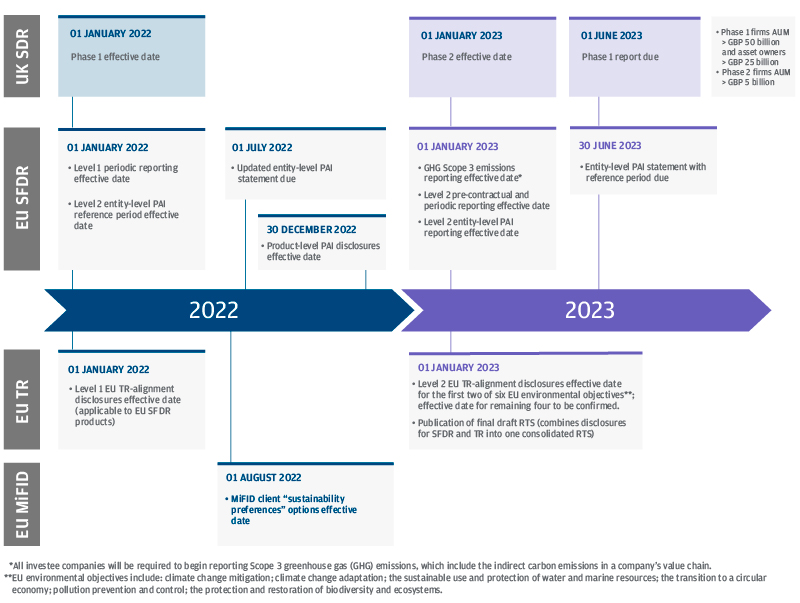

Several EU sustainable finance initiatives, in various stages of development, will likely incorporate elements of the EU TR, such as: