Week in review

- U.S. Federal Reserve kept policy rate unchanged at 3.50%-3.75%

- Bank of Japan raised policy rate by 25bps to 1.00%

- China retail sales and YTD FAI contracted 0.6% and 4.1% y/y in May

Week ahead

- U.S. PCE index

- China industrial profits

- Korea business and consumer confidence

Thought of the week

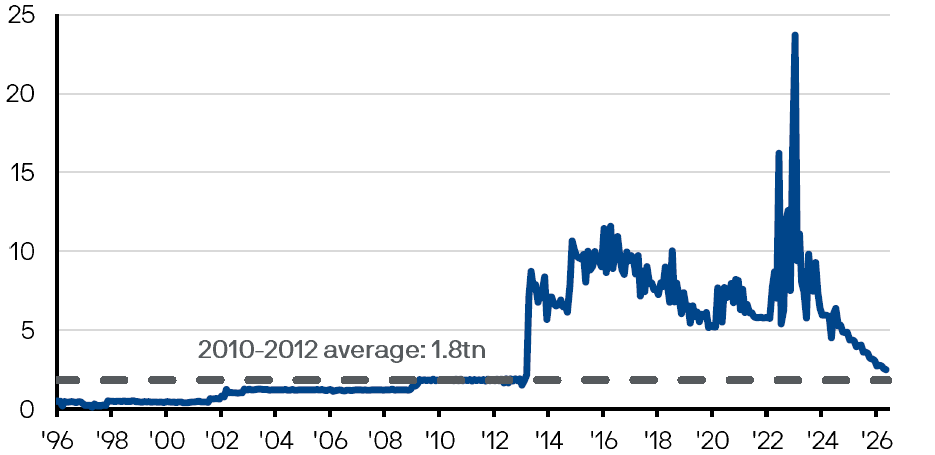

Half a year after the last rate hike, the BoJ has resumed monetary tightening and raised policy rate by 25bps to 1% last week. While the outcome was well anticipated, the decision likely suggests that the Board still leans more attentive towards inflation concerns over growth, especially as the risks of falling “behind the curve” is gradually building. More importantly, the BoJ has also decided to pause its Japanese Government Bond (JGB) tapering plan and keeping monthly purchases steady at JPY 2 trillion per month from April 2027. This shows that the Bank remains cautious in being too aggressive in tightening policy and is willing to trade balance sheet normalization for interest rate normalization. Although the BoJ still owns approximately JPY 530 trillion in JGBs, which could take years to run off, the new pace of JGB purchases could also be seen as similar to levels prior to the start of Abenomics in 2013, and so the decision could be interpreted as a balanced move rather than a dovish one.

BoJ monthly outright purchases of JGBs

JPY trillion

Source: Bank of Japan, FactSet, J.P. Morgan Asset Management. Data reflect most recently available as of 19/06/2026.

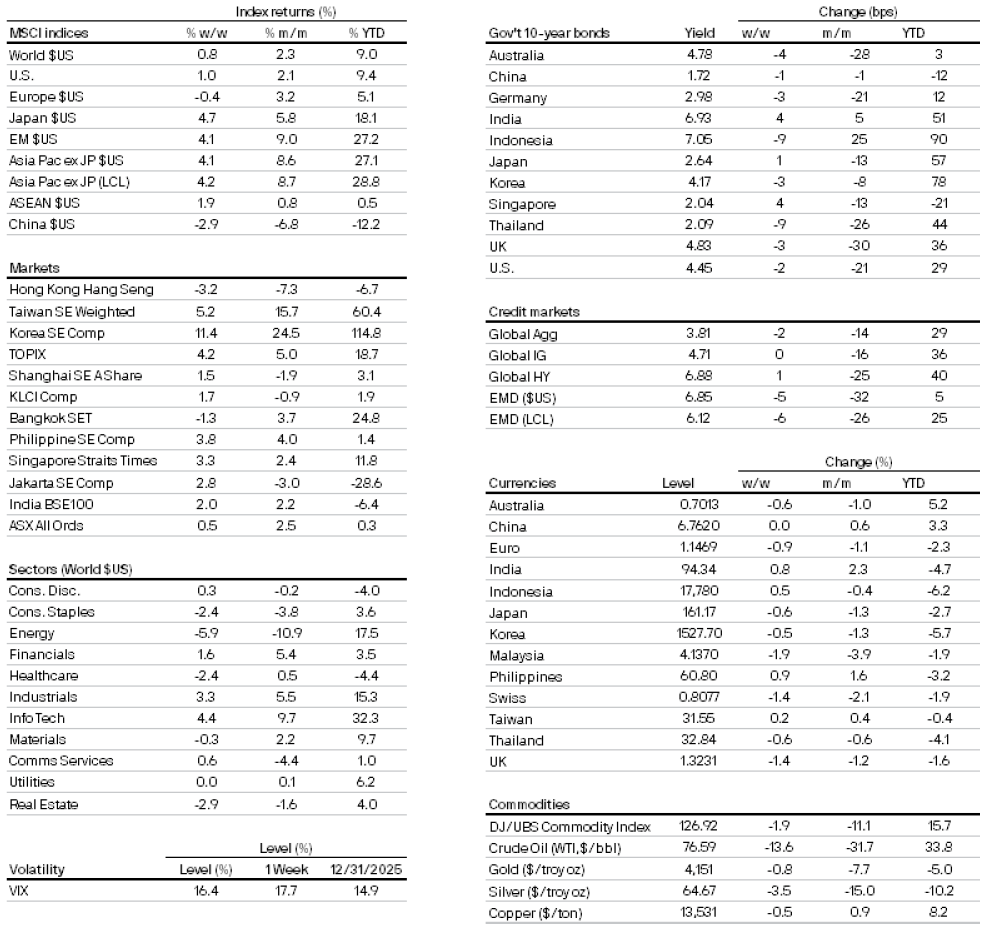

Market data

300a4900-f9d9-11e8-839f-fe2ee17e7f12

All returns in local currency unless stated otherwise.

Currencies’ return are based on foreign currencies per U.S. dollar. An appreciation of the foreign currency against the U.S. dollar would be positive and a depreciation of the foreign currency against the U.S. dollar would be negative.