In Brief

- On July 27, the Federal Open Market Committee (FOMC) raised its Federal Funds Rate target range by 75 basis points (bps) to 2.25% - 2.50%. There were no dissenters.

- The Federal Reserve (Fed) remains steadfast in its conviction to fight inflation. As a result, short-term rates continue to anticipate further tightening with a total of about 100 bps of additional rate increases priced in over the three remaining FOMC meetings this year.

- The Fed’s planned balance sheet reduction continues to run at a pace that we anticipate will have no near-term, material impact on short-term credit markets. Demand for short-dated investments remains high, illustrated by elevated Fed reverse repo balances above $2.1 trillion.

- Global Liquidity portfolios are well positioned to capture the uplift in overnight rates and stand to benefit from continued tightening by the FOMC.

July FOMC highlights

The FOMC unanimously decided to increase its Federal Funds target rate by 75 bps for the second consecutive meeting, which is the most aggressive tightening since the 1980s. The new target range is 2.25% - 2.50%. Interest on Reserve Balances (IORB) and the overnight Reverse Repo Rate (RRP) were also increased by equivalent amounts to 2.40% and 2.30%, respectively. The unanimous decision was notable as Esther George, who dissented for a smaller 50 bp increase in June, moved back in line with her peers.

Inflation remains the Fed’s top focus. During the press conference, the Fed Chair, Jerome Powell, made multiple references to fighting inflation, which has been running well above the Fed’s long-run goal of 2.00%. The Fed remains steadfast in its conviction to fight inflation, but its future path has not yet been defined and will depend on data. With 56 days between FOMC meetings, there will be a lot of data to digest, but the market will be especially focused on the Consumer Price Index (CPI) print that comes out August 10. Currently, Chair Powell has chosen not to guide the market towards a rate increase of 50 bps or 75 bps at the September meeting, and instead commented that another unusually large 75 bp rate hike will be data dependent. However, it’s possible the CPI number could sway markets, ergo the Fed, even more definitively in one direction. If the data dictates another 75 bp rate increase, at what point do unusually large 75 bp rate hikes become usually large? While the Fed may believe that 75 bps rate hikes are unusually large and want to move at a slower pace in the future, we believe the Fed will size further increases to fit the incoming data.

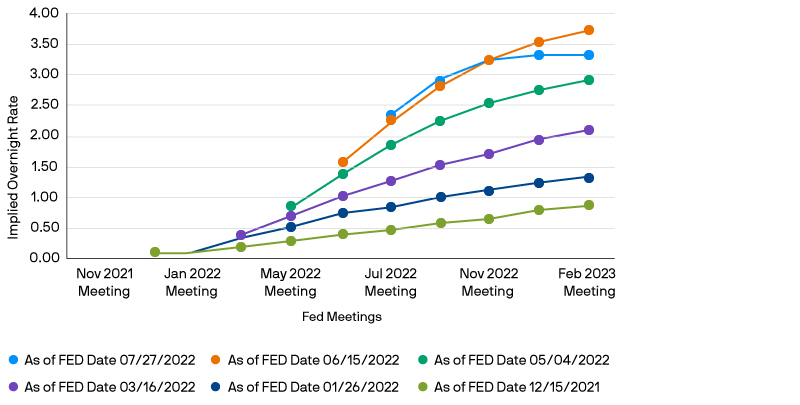

The market currently favors an increase of 50 bps at the September meeting and is calling for about 100 bps in additional tightening over the remaining three Fed meetings in 2022. Over the first half of the year, markets became increasingly hawkish, running ahead of the Fed’s own projections for the target range. However, market estimates for future Fed hikes have come down recently and forward curves have even begun to project cuts in 2023. The chart below (Exhibit 1) shows that for the first time, market expectations for future rate hikes are crossing below previous meeting expectations.

Exhibit 1: Fed Fund Futures implied overnight rate time series

Source: Bloomberg, as at July 27, 2022.

During the press conference, Chair Powell attempted to address market estimates by referencing the Fed’s June Summary of Economic Projections (SEP), which implied 2022 year-end rates of 3.25% - 3.50%, and suggesting that was still a reasonable estimate, along with the 50 bps in tightening projected by the SEP for 2023. The Fed has moved expeditiously towards neutral, and according to Chair Powell, rates are currently within the neutral range. Ultimately, the Fed still believes that it will be able to taper its rate hike path and guide markets to a soft landing.

The Fed chose to not make any adjustments to its quantitative tightening plan, and assets will continue to roll off its balance sheet at a pace of $47.5 billion a month ($30.0 billion in Treasuries and $17.5 billion in mortgages). We anticipate the current pace will have no near-term, material impact on short-term credit markets as demand for short-dated investments remains high, illustrated by elevated Fed RRP balances above $2.1 trillion.

Investors implications

We believe money market investors should continue to welcome higher monetary policy rates. The short average maturity of money market funds, due in part to the substantial positions held in overnight to one-week maturities, allows funds to quickly reset yields in line with market rates. As a result, Global Liquidity portfolios are well positioned to capture the uplift in overnight rates and stand to benefit from continued tightening by the FOMC.

This communication has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yield are not a reliable indicator of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited (ABN 55143832080) (AFSL 376919). For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2022 JPMorgan Chase & Co. All rights reserved.

09ja220108091339