Portfolio Manager, U.S. Managed Reserves, Global Liquidity

Geopolitical Tensions: Temporary Shocks, Lasting Economic Effects

The global economic landscape in 2026 is shaped by ongoing geopolitical tensions and shifting market dynamics. Recent developments in the Middle East have introduced new uncertainties, with military actions expected to be limited in duration but their economic and market implications likely to persist for several quarters. Oil futures suggest that price disruptions may normalize within a year, indicating that the immediate impact could be temporary. However, inflationary pressures—especially from higher energy costs—are anticipated to linger, affecting both consumer sentiment and broader economic growth.

Historical comparisons point to the tariff disputes of the previous year as a useful analogy. Those events triggered intense, short-term market volatility, including significant sell-offs in major equity indices and notable movements in fixed income spreads. The longer-term effect was a sustained increase in inflation, particularly for goods. This pattern may repeat: a burst of volatility followed by ongoing inflationary pressures and modest GDP detraction due to elevated oil prices.

Federal Reserve Policy

Monetary policy remains a central focus for investors. Despite the inflationary backdrop, the Federal Reserve’s next move is widely expected to be a rate cut. The Fed’s preferred inflation measure, core PCE, excludes volatile food and energy prices, allowing policymakers to concentrate on broader economic trends. With job creation slowing, unemployment rising, and wage growth declining, the Fed is likely to prioritize labor market health over short-term inflation spikes. However, the timeline for rate cuts has shifted. Instead of multiple cuts, expectations now center on a single cut, delayed to the latter part of the year. This adjustment reflects the need for policymakers to monitor the evolving impact of geopolitical events and inflation before taking further action.

Continuity in Fed Leadership

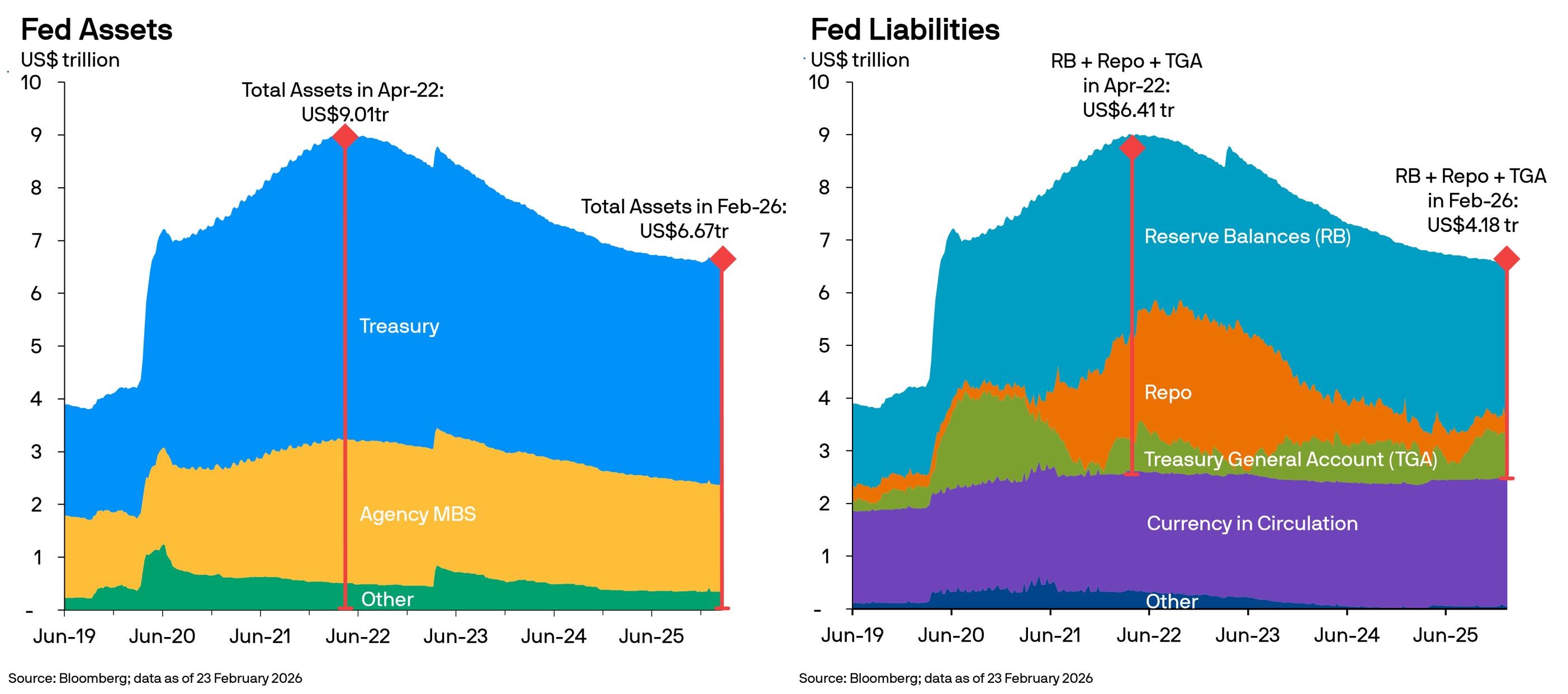

Looking ahead to potential changes in Federal Reserve leadership, the market consensus is that a new chair is unlikely to enact significant shifts in policy. Current economic constraints, including the size of the Fed’s balance sheet and liquidity conditions in the banking sector, limit the scope for drastic changes. The Fed’s balance sheet, particularly bank reserves, has already contracted considerably, and further reductions could strain liquidity. As a result, continuity is expected, with little difference in policy direction regardless of leadership changes.

Federal Reserve Policy

USD Money Market: Resilience and Growth

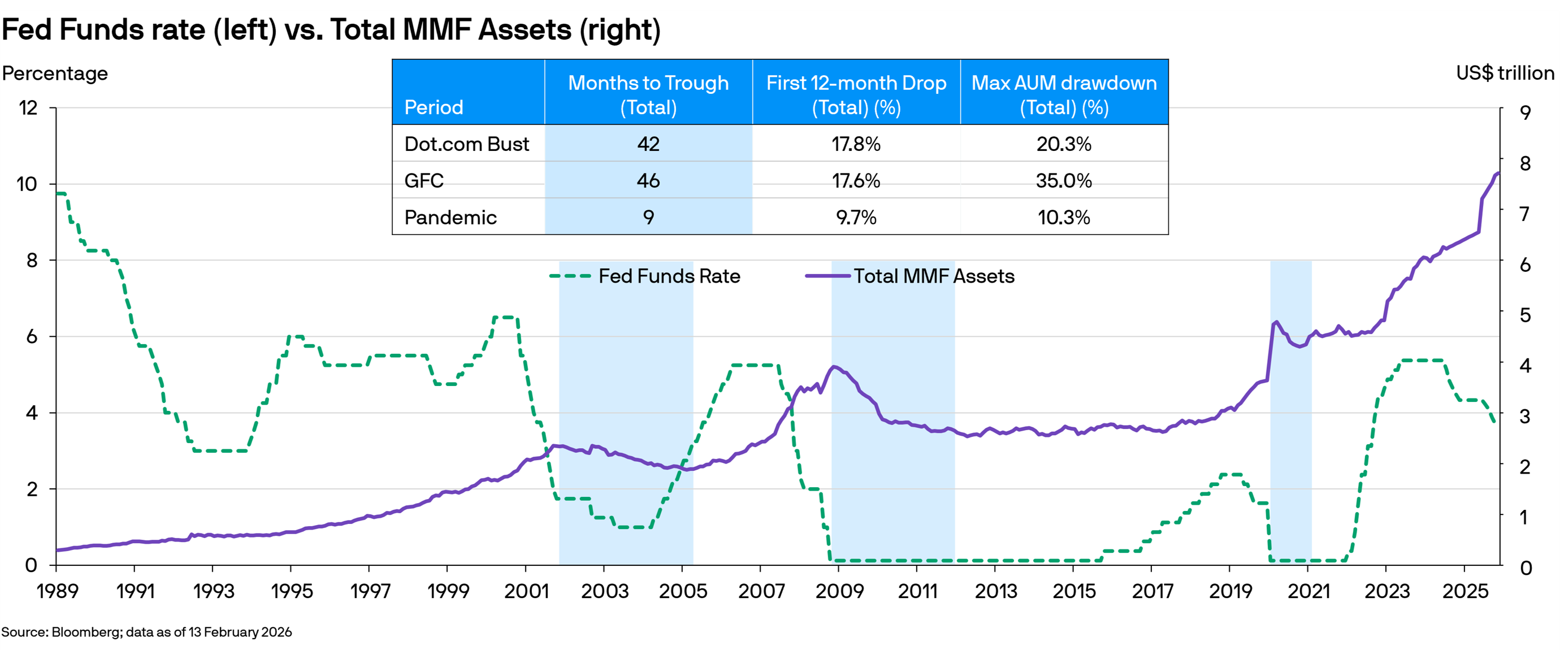

USD money market funds have demonstrated remarkable resilience, continuing to grow despite predictions of outflows. Historically, inflows occur not only when rates rise but also when the Fed initiates cuts, as money market funds present relative duration advantages over traditional deposits. Outflows typically happen only when real rates turn severely negative—a scenario not anticipated in 2026. Instead, modest inflows are expected, reinforcing the role of money market funds during periods of uncertainty.

Significant drawdowns in MMF AUMs are not driven by the act of cutting itself but by negative real rates. In fact, MMFs typically see inflows during periods of cuts.

Investment Implications

Against this backdrop, several strategies stand out for liquidity investment. With the Fed’s next move likely to be a cut, longer-duration securities present opportunities for both carry and price appreciation. The treasury market, with two- and three-year yields slightly above overnight rates, presents value for those willing to extend duration. This approach aligns with the expectation that rates will fall, enhancing returns for portfolios positioned accordingly. Investors may further seek return opportunities by taking on selective credit risk, particularly in high-quality, short-term instruments such as U.S. utilities or Canadian energy companies. These assets are insulated from Middle East-related risks. However, it is worth considering to avoid simultaneously extending duration and increasing credit risk, as this combination may introduce unnecessary volatility. Instead, focusing on one strategy at a time—either moving horizontally across credit or vertically in duration—could help manage risk.

Conclusion

The primary driver of money market fund outflows is severely negative real rates. As long as the Fed maintains modest action and avoids pushing real rates deeply negative, money market funds are likely to continue seeing inflows. The Federal Reserve is expected to maintain a cautious approach, with only modest rate cuts likely. Significant changes in Fed leadership are not anticipated to alter policy direction in the near term. Money market funds are poised for continued growth, supported by stable real rates and investor demand for liquid assets. Opportunities exist in both duration and credit selection, but one should avoid combining these strategies in the current environment.

In summary, the outlook for USD money market in 2026 is shaped by a mix of geopolitical uncertainty, cautious monetary policy, and market resilience. By focusing on duration, selective credit risk, and monitoring real rates, investors could position their portfolios to capture value and maintain relative stability amid ongoing market shifts.