In 2026, investors face a complex global investment landscape marked by heightened volatility, geopolitical uncertainty, and technological disruption. Amid portfolio rebalancing and changes to strategic asset allocations, private infrastructure allocations are rising in response to these concerns as investors seek diversification, inflation linkage, income and long-term return potential.

Momentum in private infrastructure continues to be supported by resilient asset-class performance through recent market cycles, and new investment opportunities driven by energy demand, energy security, and the energy transition (the “3Es”). The future investment opportunity remains significant, supported by a capital expenditure (“CapEx”) super cycle, a backlog of closed-end fund exits, and corporate carve-outs to recycle capital from operating assets to higher growth opportunities.

Infrastructure has long been a natural fit for insurers. Historically, however, capital treatment has often limited broader allocations, particularly where infrastructure equity attracted charges comparable to private equity. Across APAC, this is changing. Regulators are increasingly recognizing the lower-risk characteristics of qualifying infrastructure through reduced capital charges. This shift presents insurers the potential for meaningful capital relief, improved asset-liability matching, and portfolio diversification. Yet the pathways to qualification are far from uniform. Eligibility definitions, sector treatment, capital incentives and look-through requirements differ across Singapore’s RBC2, Korea’s K-ICS, Hong Kong’s RBC, and globally comparable standards such as the IAIS ICS. ICS is also relevant for markets such as Taiwan and Japan, although local implementation continues to evolve.

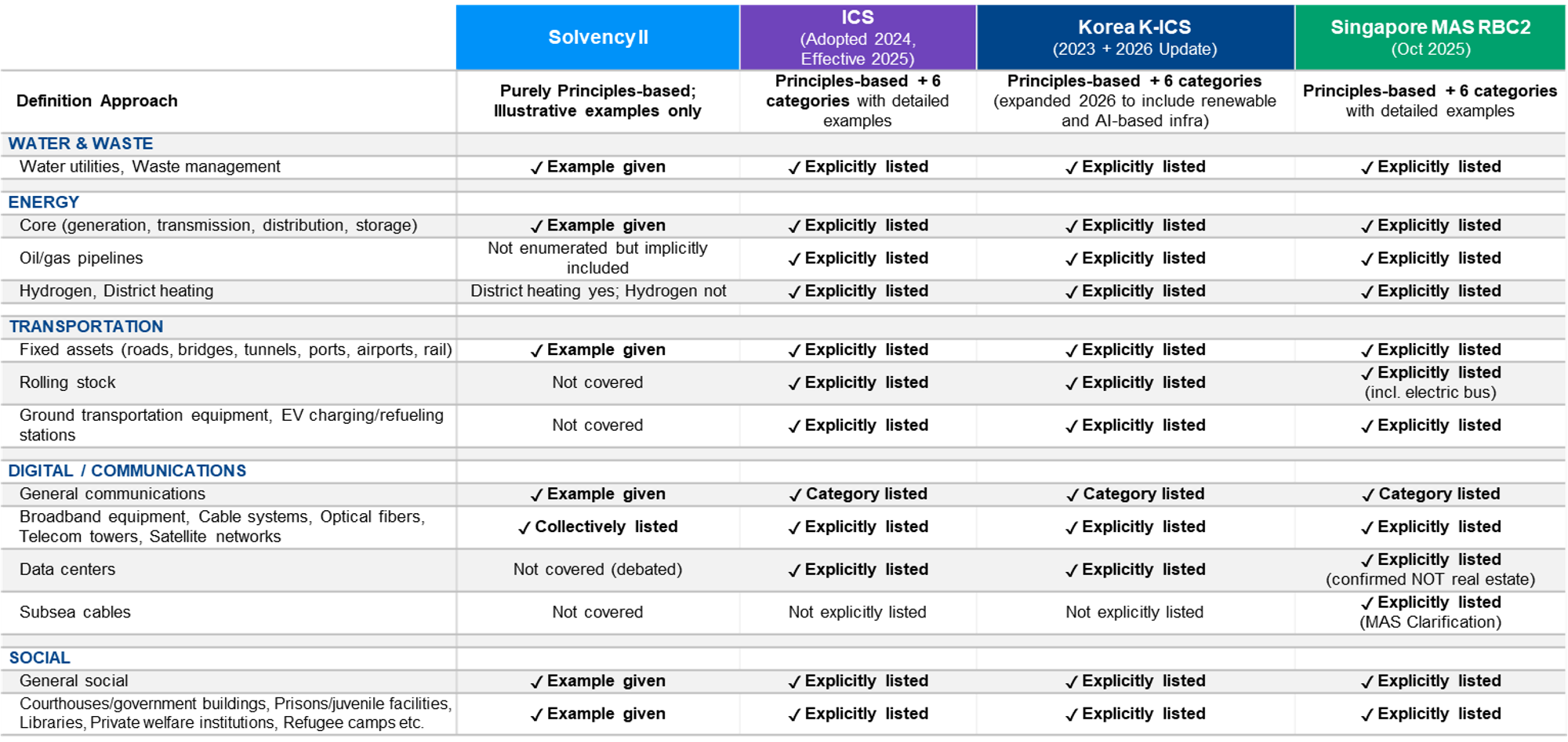

Eligibility: Similar Direction, Different Rulebook

Table 1 shows that “infrastructure” is not a universal regulatory category. ICS offers broad geographic flexibility and covers six categories, while Solvency II remains more principles-based and focused on EEA/OECD markets. Singapore provides clearer recognition of modern digital infrastructure, including data centers, EV charging and subsea cables, while Korea places greater emphasis on public-service linkage and expands in 2026 to include renewable and AI-based infrastructure. Sector scope is therefore critical: traditional water, energy and transport assets are generally well recognized, but digital infrastructure remains more uneven across regimes.

Table 1: Infrastructure investment eligibility by regime

Source: Korea FSC/FSS, MAS, Solvency II and IAIS regulatory materials, including Korea’s 2023 handbook and April 2026 measures, MAS RBC2 infrastructure treatment finalized October 28, 2025, Solvency II amendments adopted September 2025, and IAIS guidance.

Key Qualifying Criteria for Infrastructure Investments

The practical implication is that regulators are not rewarding the infrastructure label; they are rewarding evidence of lower risk. While specific rules vary across regimes, several criteria are consistently important in demonstrating the lower-risk profile that supports differentiated capital treatment.

- Revenue resilience: Regulated or long-term contracted cash flows, with performance that can remain stable through economic cycles.

- Risk mitigation: Stable regulation, enforceable contracts, relatively predictable legal and political environments, and prudent operational, financial and refinancing risk management.

- Long-term ownership and diversification: A long-term equity orientation, supported by diversification across assets, sectors and geographies.

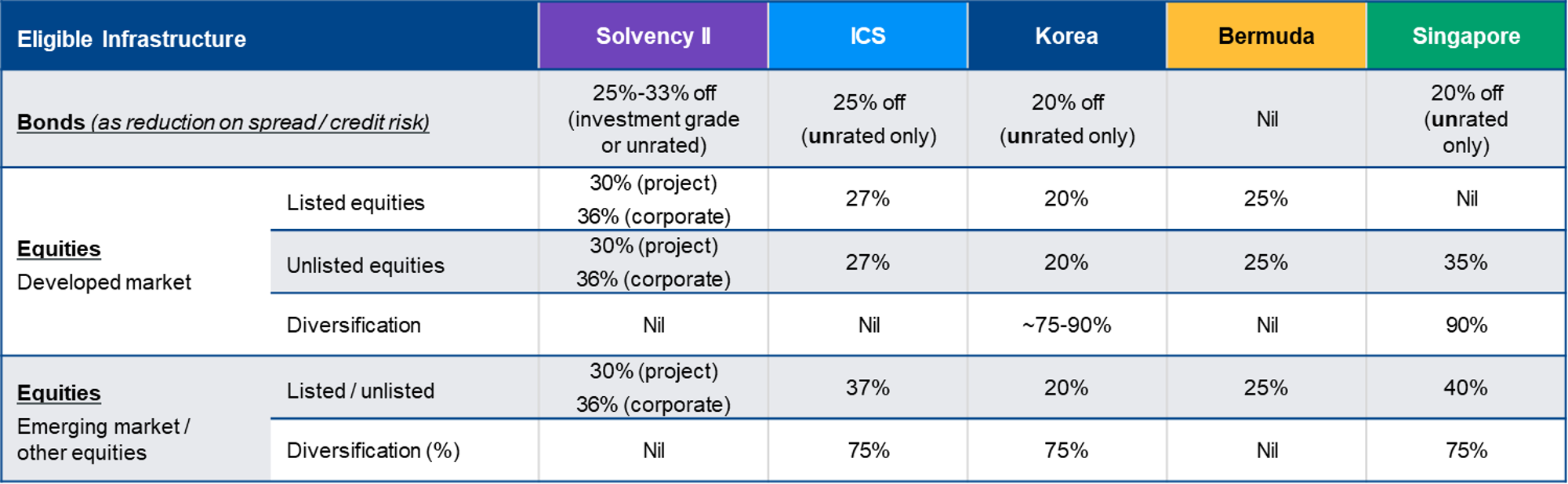

Capital Incentives: Debt, Equity and Diversification

Table 2 shows that capital incentives vary materially by regime and asset type. For eligible infrastructure debt, Solvency II provides a 25%–44% reduction in spread risk for qualifying investment-grade or unrated exposures. ICS provides a 25% discount in credit risk, but for unrated exposures only. Singapore provides a 20% reduction in spread risk, while Korea offers a more significant credit risk discount for unrated qualifying infrastructure debt.

Equity treatment differs even more. Korea is the most capital-efficient among the regimes shown, applying a 20% charge to eligible infrastructure equity across developed and emerging or other markets. ICS applies 27% for developed-market equities and 37% for emerging-market or other equities. Singapore applies 35% for developed-market unlisted equities and 40% for emerging-market or other equities. Solvency II distinguishes between project and corporate infrastructure. ICS, Korea and Singapore also provide diversification benefits, which can further reduce overall capital requirements.

Table 2: Global capital incentives for eligible infrastructure investments

Source: Regulatory sources including IAIS, MAS, Korea FSS, EIOPA, and BMA (as at Q1 2026). Interpretations by J.P. Morgan Asset Management as of May 2026

The capital-efficiency implication is significant. With reduced capital charges and, in some regimes, diversification benefits, qualifying infrastructure equity can begin to present capital-adjusted returns that are more comparable with real estate and public equity, while retaining distinctive characteristics such as predictable cash flows, diversification potential and inflation linkage.

Look-Through, Data and Governance

For insurers investing through funds, look-through is the operational bridge between regulatory eligibility and actual capital relief. Asset-level data may be required to evidence sector eligibility, revenue quality, jurisdictional exposure and risk protections. Project entities typically require asset- or project-level verification, while infrastructure corporates are often assessed at the entity or holding-company level where most revenues come from qualifying infrastructure activities.

Governance is equally important. Insurers remain responsible for solvency calculations, validation and regulatory compliance, while asset managers can support them with standardized data, eligibility assessments, and timely notification of material portfolio changes. Independent review can also play a useful role, particularly where insurers have limited in-house infrastructure expertise. External assessments can support pre-investment gap analysis, eligibility documentation and ongoing attestation, while giving supervisors greater confidence in early-stage implementation.

Conclusion

The evolution of qualifying infrastructure regimes marks an important step for APAC insurance markets. As capital treatment becomes less punitive, infrastructure equity has a clearer path to becoming a core allocation within long-term strategic asset allocation, alongside real estate, public equity and private credit. The benefit, however, will accrue most to investors and asset managers that can translate regulatory eligibility into evidence: predictable revenues, eligible jurisdictions, strong protections, disciplined risk management, reliable look-through and robust due diligence. Over time, this can deepen institutional capital pools for infrastructure, supporting both insurer portfolio resilience and the region’s long-term financing needs.