In brief

Overview: APAC growth holds up, but trade-offs are more challenging

Two forces, geopolitics and AI, have been the dominant drivers of APAC markets and economics in 2026. Elevated uncertainty stemming from the Middle East conflict has had clear economic consequences for the region: higher oil prices, tighter supply, and softer confidence. This creates a headwind to growth, especially in economies dependent on imported energy.

The counterweight, AI-related tech demand and investment, have kept growth across APAC more resilient than expected. Government intervention (via fuel tax waivers, subsidies, and strategic reserve releases) has also helped cushion consumers and businesses from the worst of higher energy prices.

For central banks, this mix is uncomfortable. Higher energy prices are pushing headline inflation up and increasing the risk of second-round effects, even as the longer-run impact is likely slower growth. That creates a difficult policy trade-off and raises the risk of a policy mistake in either direction. For now, most regional central banks are converging on “wait and see” data dependent stance. But this strategy is not risk free and could leave policy makers struggling to respond to fast moving geopolitical and market factors.

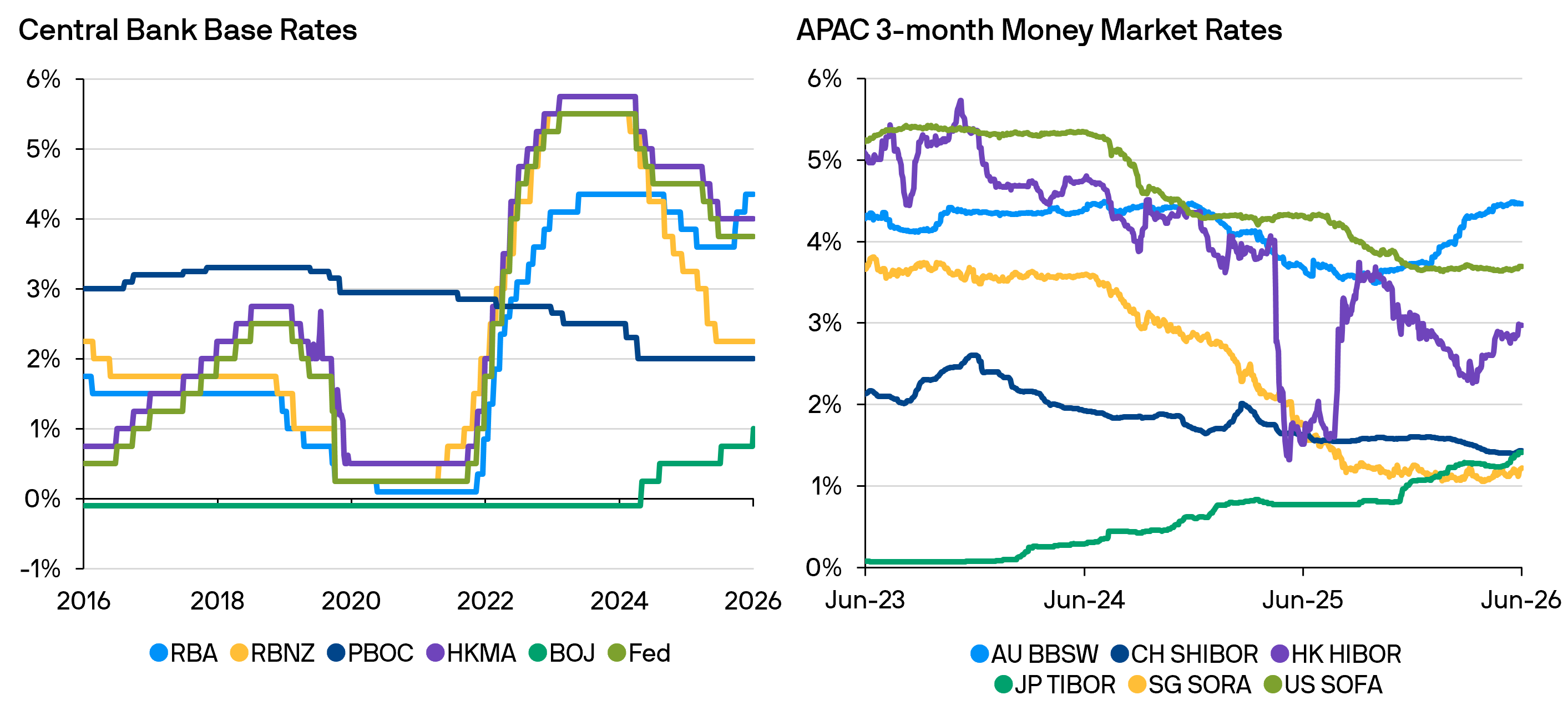

Source: Bloomberg, as at 19 June 2026.

Provided for information only to illustrate macro trends, not to be construed as offer, research or investment advice

Regional central bank trends

Australia entered the energy shock with sticky inflation, a tight labor market, and signs of an overheating economy. This has triggered three successive hikes by the Reserve Bank of Australia (RBA), back to the prior cycle high. Higher energy prices have increased the risk that inflation becomes more embedded, even if growth cools.

At the June meeting, the RBA held the cash rate at 4.35%. It paused to assess the cumulative impact of tightening and the oil-supply disruption, while stressing it would hike again if inflation risks intensified. With activity indicators softening and policy already restrictive, the RBA may be close to the peak, with scope to shift toward a hawkish hold if inflation moderates.

China’s headline growth looks robust, but the outlook remains mixed. The divergence between strong external demand and softer domestic momentum is clear. Exports have rebounded sharply, supporting industrial profits and manufacturing. Meanwhile, retail sales, investment, and credit demand remain weak amid still-soft property conditions.

Inflation has risen and producer prices are increasing. This reduces deflation risks without confirming broad-based domestic reflation. While real rates remain restrictive, the People’s Bank of China (PBOC) appears reluctant to let nominal rates fall too far. The implication is a continued dovish bias but with an emphasis on targeted tools and calibrated support rather than rate cuts, especially if near-term energy risks fade.

Hong Kong’s activity data has been notably stronger in 2026. First quarter growth rose at the fastest pace in three years, driven by robust exports, a recovery in tourism and a rebound in private consumption. Headline inflation has edged higher but remains relatively muted as lower food prices offset higher energy costs.

The key risks facing the Hong Kong Monetary Authority (HKMA) are higher local yields and persistent Middle East tensions. As markets unwind expectations for Fed cuts and reprice tightening risk, HIBOR yields have moved higher. Given the HKD peg constrains independent rate policy, the practical implication is continued sensitivity of domestic financial conditions to global rates and risk sentiment.

Japan is dealing with a cost-of-living squeeze. Higher prices but flat wages have weakened consumer and business confidence. Policymakers are balancing stubbornly high inflation against growth concerns and political sensitivity.

In June 2026, the Bank of Japan (BOJ) resumed its hiking cycle, increasing the overnight call rate to a three-decade high of 1.00%. The split decision underscored internal caution, but the rationale was clear: underlying inflation risks remain elevated while fiscal spending is increasing. Real rates are still negative and financial conditions remain too accommodative. The hawkish-but-cautious BOJ is likely to continue policy normalization but with heightened focus on market volatility.

Singapore’s growth has been supported by strong manufacturing and exports, while domestic activity is more muted, though still positive. Even so, the government retained its 2026 growth range, flagging downside risks from the Middle East conflict. While inflation has surprised to the downside, energy related shocks are weighing on real demand and could still trigger second round effects.

The Monetary Authority of Singapore (MAS) is likely to maintain a hawkish bias. With the conflict lasting longer than expected, the odds of further tightening have risen even if oil prices ease. Still, the base case is for policy to stay unchanged as MAS assesses inflation dynamics and the durability of the AI investment boom.

Conclusion: The end of easing

The second half of 2026 is shaping up as a regime shift for APAC central banks: from a gradual easing narrative to one defined by inflation vigilance, asymmetric energy risks, and uneven AI-driven growth.

Most central banks are opting for caution, the policy starting point matters. Economies entering the shock with more restrictive policy have more scope to wait and see; while those with neutral or accommodative settings face sharper credibility trade-offs. In any case, the direction is clear: the interest rate cutting cycle is over and if inflation accelerates, the next move may be hikes.

For regional cash investors, higher yields and a still upward sloping yield curve continue to offer higher current income and opportunities to tactically extend duration and lock in attractive yields. A disciplined and diversified investment approach remains essential amid geopolitical uncertainty and market volatility.

EMEA and U.S. outlook

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.