Marketing Communication

UK smaller companies’ performance has lagged in recent years. But many feel that current valuations and improving prospects offer an exceptional buying opportunity.

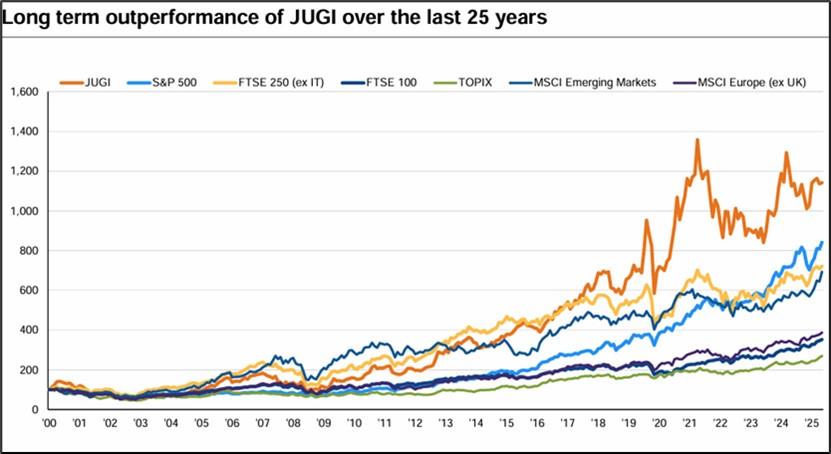

Many of the businesses set to become tomorrow’s household names begin their journey as small companies, serving niche markets. Yet by their nature, smaller companies tend to innovate, and grow more quickly than larger, mature businesses. This inherent vibrancy has seen UK smaller companies (as represented by the FTSE 250) outperform larger (FTSE 100) UK companies over the past 25 years. Their performance has been close to that of the S&P 500 and they have outpaced other major markets over the same period.1 This long-term outperformance of UK smaller companies may, however, surprise some investors who have watched the sector struggle in the face of high interest rates over the past three years, and underperform UK large caps and other markets with greater resilience to high rates.

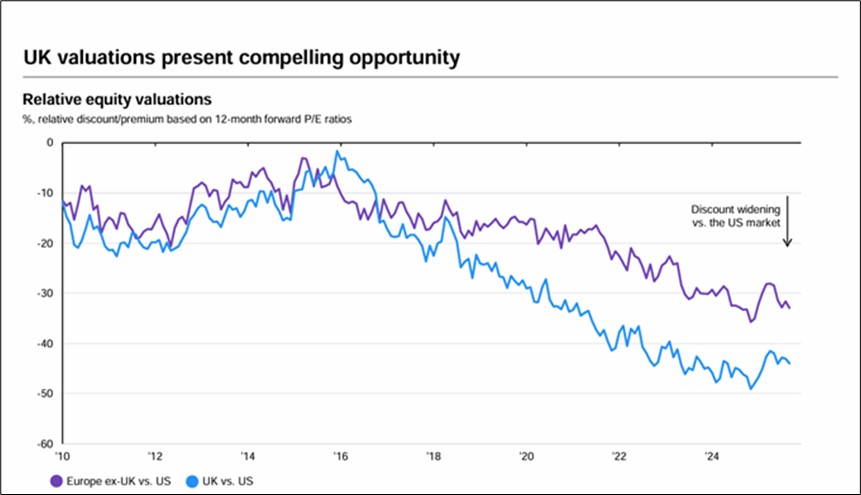

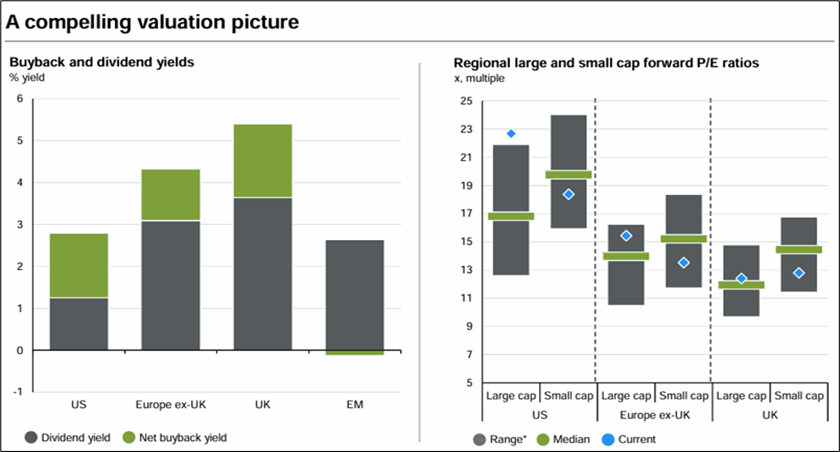

Despite their recent travails, if history is any guide, UK smaller companies are overdue a re-rating. In fact, one of the sector’s most experienced investors sees signs that this re-rating has already begun and looks set to gather momentum in 2026. Georgina Brittain is co-portfolio manager of JPMorgan UK Small Cap Growth & Income (JUGI). The most important factor underpinning her optimism is what she considers to be the ‘unprecedented’ value presently on offer in the entire UK market. UK shares are trading at wide discounts relative to their own history and compared to international markets.2 And after their underperformance of recent years, smaller UK companies are even cheaper.3 These extremely low valuations mean there are compelling bargains available among UK smaller companies.

JUGI: Growth potential alongside a regular income

JUGI is designed to provide investors with exposure to this area of the market. The trust offers a diversified portfolio of high-quality UK smaller companies that can otherwise be difficult for retail investors to access. It aims to provide shareholders with long-term capital growth, combined with a competitive, predictable income – JUGI targets a 4% yield on annual NAV, paid via quarterly dividends.

Active approach and long-term mindset

The trust’s portfolio managers are skilled at identifying investment opportunities as they emerge, and they are supported in their quest by JPMorgan Asset Management’s extensive team of experienced analysts. The team’s long-term mindset means they have the patience to allow the trust’s holdings to realise their full growth potential. And they are not afraid to back their views by adopting significant active positions relative to benchmark (the Numis Smaller Companies plus AIM Index), and by avoiding benchmark constituents they do not like.

This trademark, high conviction investment approach has proved effective recently, and over the longer term. Several of the portfolio’s largest active positions, in companies such as Lion Finance, a regional bank, Alpha Group International, a financial solutions business, and Morgan Sindall, an engineering and construction company, featured among the main contributors to returns in the year to end September 2025, while their decisions not to hold names such as John Wood Group, an energy services company, GlobalData, a consultancy firm, and troubled retailer WHSmith, also boosted performance over the period . And the portfolio manager’s willingness to give businesses time to grow has ensured that long-term performance has been impressive. The trust consistently ranks in the top quartile of its most directly comparable small cap peers, across three-, five- and 10-year periods.4

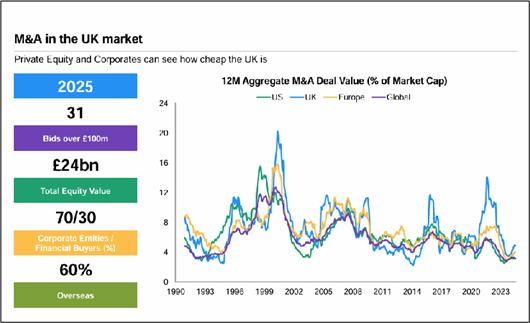

Domestic and international investors have started to notice the opportunities available in the UK market. Flows into UK equities began rising in 2023 and increased in 2025, due in part to investors rotating away from the US into other markets, notably the UK.5 Further evidence of rising interest in the UK market is the surge in mergers and acquisitions activity (M&A) over the past two years.6 Many of these transactions are being undertaken at significant premiums to their share prices. Smaller companies are natural targets for such takeover activity, and several of JUGI’s portfolio holdings have been sold at share price premiums of more than 50%. These included Renold, an engineering business specialising in power transmission, and two financial companies, Alpha Group International, a foreign exchange company, and Just Group, a retirement services provider. The trust’s manager expects this takeover trend to persist for the foreseeable future, with other portfolio holdings likely to attract equally profitable bids. Low valuations are also prompting UK-listed companies to buy back their own shares. These buybacks demonstrate managers’ confidence in their businesses, and their conviction that their share prices are unjustifiably low and thus represent sound investments which is also adding to the value of remaining shares.7

ISA changes encourage investment in equities rather than cash

The Government’s November 2025 budget included one policy change which actively encourages greater investment in equities. Effective from April 2027, the allowance for investment in cash ISAs for investors under 65 was cut to £12,000, while the full, £20,000 allowance was retained for stocks and shares ISAs. This change is clearly intended to support the UK stock market by incentivising investors to eschew the relatively low real returns generated by cash holdings in favour of the much higher long-term gains historically generated by equity investments.

Scope for improvement in the domestic economy

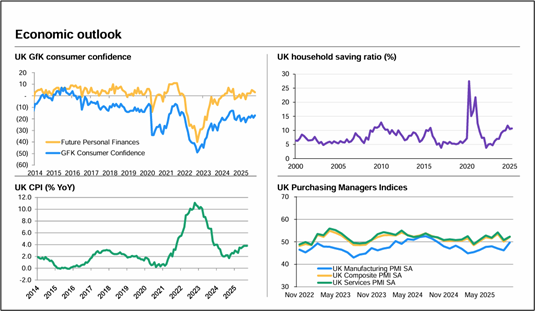

There is another factor that bodes particularly well for UK smaller companies. Unlike their larger counterparts which draw 80% of their revenues from abroad,8 UK smaller caps are dependent on the strength of the domestic economy for around 60% of their income – and the UK economy should be broadly supportive of these businesses in 2026. The Bank of England cut rates to 3.75% at its December 2025 meeting and is expected to implement further modest monetary easing in 2026,9 real wages are rising,10 and now the uncertainties surrounding the Government’s budget have been removed, there is scope for business and consumer sentiment to build on the small improvements seen in the final six months of 2025.11

Indeed, Brittain is looking towards 2026 with obvious relish. Her confidence in the prospects for the UK economy, UK equities and JUGI is illustrated by the portfolio’s current 10% gearing,12 which amplifies its exposure to market performance. Other investors seeking exposure to the exciting, but sometimes inaccessible, opportunities on offer amongst smaller UK companies, as well as an attractive, regular income, may be well-rewarded for following where such an experienced, insightful investor leads.

While reliance on the domestic market can present certain risks, it also means that UK smaller companies are well-positioned to benefit from any positive developments in the local economy.