Every size of company has its own attractions. Small businesses that get their product and story right have the potential for exponential growth, while blue-chip companies in the FTSE100 offer a bedrock of stability, diversity and reliable income streams.

But the ground between these two extremes is occupied by the mid-caps – medium-sized businesses, typically worth between £1 billion and £5 billion in the UK – which for many is an investment ‘sweet spot’.

These companies are often well-established and far less risky or vulnerable than their smaller counterparts, with relatively strong balance sheets and easier access to capital markets should they need to raise funds for further growth.

At the same time, they typically operate in faster-growth environments than many British large cap businesses, and they are still relatively unbureaucratic and nimble enough to continue rapid growth.

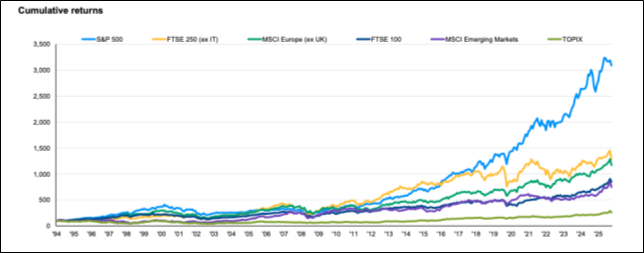

That’s reflected in plentiful research showing their capacity for long-term outperformance of both small and large companies. For instance, data1 shows that the UK mid-cap index, the FTSE 250 Index, has outperformed all other major markets except the US over the past 30 years.

Understanding the growth trajectory

The growth journey of an emergent business takes it through a series of stages. Evolving businesses move from the initial seed phase through startup and growth to become established companies. Later stages include expansion, maturity – which can last decades, and renewal or decline.

Each one has its own characteristics and challenges. From being a one-person band where the founder takes every decision and does everything, each new stage of a business with traction involves taking on new employees, building or adapting systems and establishing some kind of sustainable sales model.

As turnover grows and the workforce swells, management tends to become more ‘professionalised’ and less reliant exclusively on the founder. Operations have to be scaled up, made repeatable and sustainable. The business may seek institutional funding, diversify its output and may try to break into international markets.

Mid-cap-focused investors such as the team of The Mercantile Investment Trust (MRC) seek to identify those companies with real momentum and potential as they become more robust and established, but while they still have an exciting trajectory of growth ahead of them. The most successful journeys will culminate with entry into the FTSE 100 Index of the UK’s largest companies.

One impressive example of a longstanding holding in The Mercantile portfolio which did just that is Howdens Joinery*, the UK’s premier trade kitchen supplier. It was established in 19952 to sell kitchens, joinery and hardware specifically to trade customers through local outlets, and has expanded over the past 30 years to operate almost 900 depots in the UK and Europe.2 Howdens entered the FTSE 100 in March 20223,The Mercantile sold the stock in 2024 to repurpose the profits into more up-and-coming opportunities.

A continuing growth triumph is Warhammer manufacturer Games Workshop Group*, which joined the blue-chip index at the end of 2024 with a market capitalisation of more than £6 billion4. This highly profitable and efficiently run business is underpinned by a huge and loyal base of war-games hobbyists and has recently partnered with Amazon to develop films and TV series. The shares have generated total returns for The Mercantile of well over 1,400% since the initial purchase of shares in 20175, but it remains one of the portfolio’s largest holdings.

Similarly, the significant Mercantile holding in alternative asset manager ICG, a FTSE 100 constituent since 2020, has served it very well.

An eye for blue-chip potential

Of course, for managers Guy Anderson and Anthony Lynch the key is to pick up shares in potential blue-chip newcomers long before they get to the foothills of the FTSE 100. Among The Mercantile holdings with potential to be promoted in due course to the big league from the FTSE 250 Index are review platform Trustpilot* and online train booking service Trainline*.

The process of sorting prospective winners from the broader spectrum of mid and smaller companies is clearly very much about individual stock picking. So, what are the managers looking for in their hunt for the enterprises with the best chances of making it big?

Quality is imperative, and they consider factors such as a company’s profitability, sustainability of earnings and capital allocation, using metrics such as return on invested capital and return on earnings.

Portfolio choices often enjoy a position of dominance or leadership within relatively niche markets, helping them achieve robust profit margins and resilience in the face of competition.

It’s also important to have conviction that the outlook for the business is a positive and improving one, and that this is being reflected in broader expectations. Growth in earnings per share is a useful measure in this respect.

Dominant market

Finally, the team will look at metrics including earnings and free cash flow to assess the accuracy of the company’s valuation; the aim is to avoid overpayment and acquire shares when the business’s future prospects have not been fully recognised and priced in by the market.

The end result is a broad-based portfolio of high-quality UK businesses, selected for their attractive valuations and long-term growth potential.

While a focus on mid-cap companies can inevitably introduce greater volatility than investing in larger firms, it can offer a compelling balance for growth-oriented investors – providing exposure to the long-term potential of the UK market while avoiding some of the higher volatility often associated with smaller-cap strategies.

Within a broader income-focused portfolio, The Mercantile can provide both a useful long-term capital growth ‘kicker’ (which could be taken as income) and a reliable quarterly dividend flow to enhance the overall income stream.

Meanwhile, UK mid-cap valuations remain notably low compared to both historical levels and global alternatives, making this an attractive opportunity for long-term investors to dip a toe into the market.