This is a marketing communication

The global geopolitical and macroeconomic environment under the Trump regime has undoubtedly proved a challenging one for investors in recent months. But for disciplined bottom-up stock-pickers, a wealth of opportunities remains despite economic uncertainties.

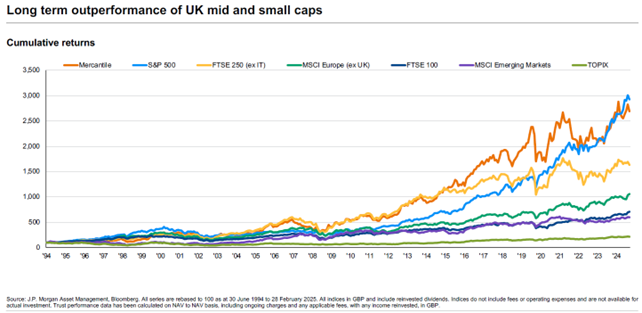

For Guy Anderson some of the richest pickings are available in the UK’s mid and smaller-cap territory where he and his team prospect.

Although they can be relatively volatile over the short term, on a longer-term perspective medium and smaller companies are inherently a more interesting and rewarding part of the market, he argues, simply because they have greater potential for growth than larger, longer-established businesses.

That’s inferred by a look at the performance of the FTSE 250 index compared with the FTSE 100, not that past performance can guarantee future results. Since June 1994, when MRC adopted a focus on this part of the market, the FTSE 250 has produced an annualised total return of around 10%, compared with around 6.5% for the blue chip index1.

MRC focuses firmly on selecting mid-cap and smaller UK stocks for long-term growth. However, explains Anderson: “We retain holdings in those companies as they move up through the market cap spectrum.” Currently, he adds, almost 20% of the portfolio comprises FTSE 100 businesses bought when they were much smaller.

Rigorous selection process

How does the team identify potential holdings from this large and diverse universe?

Fundamental analysis by JPMorgan’s expert small and mid-cap team is central to stock selection. That’s overlaid with a demanding programme of 400 to 500 company meetings a year, to assess each company’s growth prospects and plans for delivering them.

Anderson and his team then have a clear path to follow, with three key questions shaping the decision-making process.

First, is the company in question a high-quality business producing sustainable profits that can be reinvested to drive further growth? MRC’s return on invested capital – a useful measure of quality – stands at around 15%, compared with 10% for the benchmark2.

Secondly, is its outlook improving; in other words, is it well placed to do better than the market expects over the coming three to five years?

The team looks at expected earnings per share (EPS) to measure this momentum; currently, global macroeconomic challenges mean the EPS for the benchmark has declined by 3.5%2, but expected earnings for MRC’s portfolio are holding steady.

And thirdly, can it be bought at a price that suggests the market has not fully recognised its future prospects? Sensible valuations are critical if the team is to maximise returns, no matter how great the business, and the portfolio’s free cash flow yield can be utilised to check valuations are below the benchmark level.

Growing capital and dividends

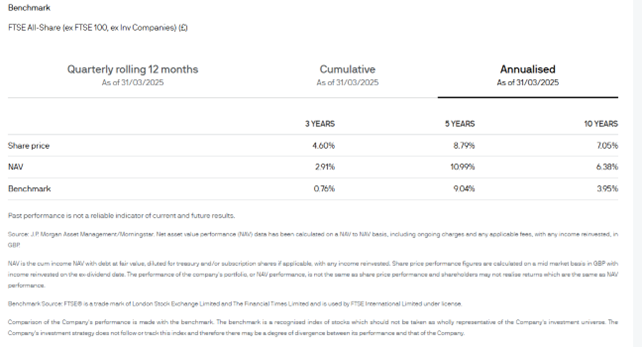

The focused and disciplined approach of the MRC team means that over 10 years, despite the challenges faced by the UK market as a whole since Brexit in 2016, the Trust has delivered annualised total returns of 7% – some 3% a year ahead of the benchmark FTSE All Share ex FTSE 100 comparator3.

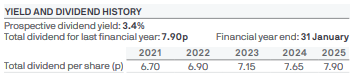

An added bonus for investors is the trust’s commitment to shareholder payouts and dividend growth over the long term. Although past performance doesn’t guarantee future results, currently MRC yields around 3.4%4, which Anderson sees as “a byproduct of the investment process, but an important component of potential returns for investors”.

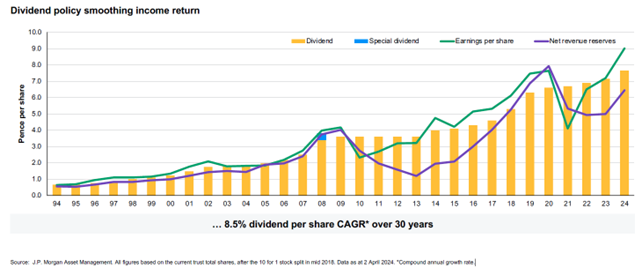

Typically, smaller and many mid-sized businesses use earnings to prioritise reinvestment that will deliver further growth, but the portfolio has produced a shareholder dividend that has grown by an annualised 8.5% over the past 30 years5.

Furthermore, there have been no payout cuts during that time, even during the 2008 financial crisis5. Indeed, the pandemic actually saw MRC increase its dividend, despite the difficulties faced by many portfolio holdings, with the trust’s capacity to draw on reserves standing it in very good stead.

Resilience is key

Looking ahead, the world seems to be in a hugely uncertain state at present, and both consumer and business confidence in the UK - which were both recovering – have taken something of a knock in the past six months. “Time will tell whether that will prove to be a blip or a more sustained downturn,” observes Anderson.

However, he emphasises that the team avoids over-exposure to companies dependent on a positive economic environment, and looks instead for “structurally strong businesses whose drivers ensure they can deliver attractive returns even in a soggier economic landscape”.

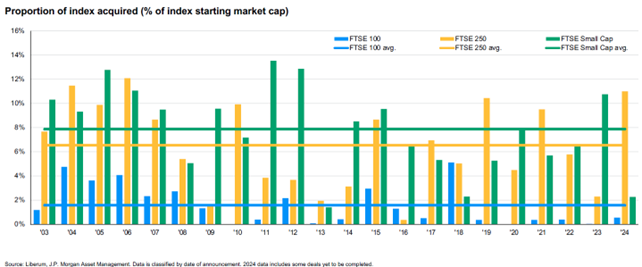

Of course, a major headwind for the UK stock market over the past five years and more has been its chronic unpopularity, which has resulted in a 20% derating for the FTSE 250 index over that time6.

Moreover, and unusually, mid and smaller-caps are even cheaper than large caps at the moment, reflecting current levels of economic turbulence.

It all amounts to an extraordinary “valuation opportunity”, says Anderson - a situation being reflected in unusually high levels of mergers and acquisitions of medium and smaller-cap companies, as other corporates snap up great deals. Fully 11% of the mid and smaller-cap arena was taken over in 2024, against a long-term average of around 6%7.

How has MRC responded to this wealth of affordable opportunities? The environment is undoubtedly tough, but as a stock-picker Anderson is feeling pretty positive: “We are finding more companies that we want to invest in than sell.”

As a consequence, the team is currently employing gearing (borrowing to invest) worth almost 15% of the net asset value⁸ - close to its highest ever level.

Always, though, that disciplined investment process leads the way, highlighting the strong businesses with compelling long-term opportunities on attractive valuations that are working so well for MRC.