Exploring the case for US equities, this article highlights the market’s scale, innovation and resilience, and why it continues to play an important role in diversified portfolios.

3 reasons why the US matters

Properly diversified portfolios need to include US stocks for three key reasons. First, scale; the US is by far the world’s largest equity market, with a market capitalisation exceeding US$70 trillion, more than three times the size of European developed markets and significantly bigger than China and Hong Kong.

Second, innovation: the US has long been at the forefront of every technological innovation since the commercialisation of the railways in the 1800s. And it is now a global leader in the rapid development and adoption of artificial intelligence (AI), which may prove to be the most significant technological advance in history.

Third, resilience: this combination of scale and innovation has historically helped US markets navigate periods of uncertainty. Over the past year, for example, US equities have weathered bouts of severe, tariff-driven volatility, to reach new highs. This ability to adapt – and keep delivering robust returns – is a particularly reassuring characteristic in these increasingly uncertain times.

JP Morgan American: targeting the best, high-quality opportunities

While the case for US equities is compelling, individual investors may baulk at the task of identifying the very best stocks in such a vast and rapidly evolving market. The solution - enlist a US specialist. JPMorgan American Investment Trust (JAM) is run by highly experienced managers who have spent their careers immersed in the US market. With more than £2 billion in assets under management¹, JAM is one of the biggest investment trusts in the AIC’s North American sector.

JAM comprises a concentrated, high-conviction portfolio of around 40 hand-picked holdings. There is much debate about the relative merits of investing in growth or value stocks, but JAM’s strategy seeks to capture the best of both worlds, by targeting the best, high-quality opportunities from the entire market, at attractive prices, rather than adhere rigidly to a particular investment style. This approach gives JAM’s managers a broader opportunity set than many of its peers. It also means the portfolio is well diversified across sectors, with exposure to enduring growth franchises, as well as to areas with lower expectations but nonetheless solid businesses, such as financials, health care and energy.

JAM’s managers are supported in their search for the most appealing opportunities by J.P. Morgan Asset Management’s very significant research resources, including a network of around 40 US-based research analysts and investment specialists – expertise that individual investors simply cannot replicate.

And JAM remains one of the most competitively priced US focused actively managed funds available to UK investors, in either closed-ended or open-ended form: At 0.35%¹ its ongoing charge is the lowest among its peers in the AIC’s North America sector by a significant margin².

Why capital growth matters at all stages of life

Whilst JAM’s primary objective is capital growth, some investors, especially retirees who rely on regular income, may question its relevance. However, there are good reasons why capital growth should remain a key consideration, regardless of an investor’s stage of life.

Most importantly, a growing capital base means growing income over time – essential for protecting income streams from the ravages of inflation. Investors may also need to draw on capital to fund larger planned purchases such as a new car, as well as unexpected costs such as home repairs and healthcare bills. Capital growth will cover such expenditures, while also providing an ongoing income stream. And many investors will of course wish to pass assets on to their children.

JAM’s track record of consistent performance

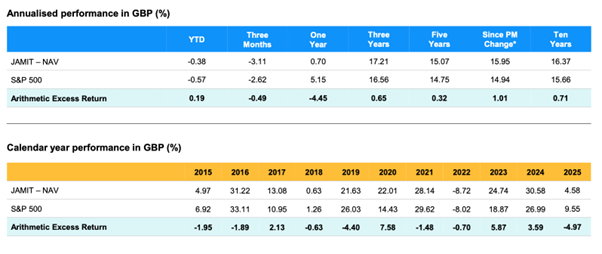

JAM’s focus on capital growth has delivered strong long-term performance. While returns have lagged in the past year – mainly reflecting a US market driven by a handful of AI-related stocks - the Trust has outpaced its benchmark over the three-, five- and 10-year periods ended 28 February 2026, with an average annualised return of 16.4% on a Net Asset Value basis over the 10-year period³, compared to a benchmark return of 15.7%.

Such consistency has earned the trust a top 10 ranking in the AIC’s ‘ISA millionaires’ research⁴ which identifies trusts which have generated returns of more than £1 million for investors who have fully utilised their ISA allowances (with dividends reinvested) over the past 25 years.

While past performance is not a guide to future returns, JAM’s managers note that periods of relative underperformance have historically been followed by stronger relative returns, as the Trust’s focus on high-quality growth companies plays out over the long term.

Investment case supported by market fundamentals

The Trust’s managers remain confident about the prospects for US equities. While recent events in the Middle East have raised fresh uncertainties regarding the global economic outlook, the team expects the same dynamism, resilience and adaptability that has underpinned the US market in the past to remain supportive. J.P. Morgan’s analysts anticipate double digit earnings growth for the S&P 500 index over 2026 and 2027.

And looking further ahead, they believe American businesses are likely to remain at the forefront of the AI revolution and other cutting-edge technologies. Such ongoing exposure to innovation should serve to propel growth and earnings over the long term, reinforcing the case for maintaining a meaningful stake in this most vibrant of markets, as part of a broadly diversified portfolio.

Sources:

1 J.P. Morgan Asset Management, as at 16 March 2026

2 AIC, as at 16 March 2026: https://www.theaic.co.uk/aic/find-compare-investment-companies?sec=NA&sortid=Name&desc=false

3 J.P. Morgan Asset Management, as at 28 February 2026. Figures over 1 year are annualised. Performance figures are those of the JPM American Investment Trust using cum income net asset value per share, with debt at fair value. The S&P 500 is based on the total return index, net of 15% withholding tax. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested. Past performance is not a reliable indicator of current and future results. *From 31 May 2019.

Annualised and calendar year performance as at 31 January 2026.

4 AIC, Which investment trusts would have made you an ISA millionaire? 25 February 2026

Summary Risk Indicator

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period.

Investment Objective: The Company aims to achieve capital growth from North American investments by outperformance of the Company's benchmark, the S&P500 Index, with net dividends reinvested, expressed in sterling terms. The Company emphasises capital growth rather than income and when appropriate may have exposure to smaller capitalisation companies. The Company's gearing policy is to operate within a range of 5% net cash to 20% geared in normal market conditions. Gearing may magnify gains or losses experienced by the Company.

Risk Profile:

- Exchange rate changes may cause the value of underlying overseas investments to go down as well as up.

- External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions.

- This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down.

- This Company may also invest in smaller companies which may increase its risk profile.

- The share price may trade at a discount to the Net Asset Value of the Company.

- The single market in which the Company primarily invests, in this case the US, may be subject to particular political and economic risks and, as a result, the Company may be more volatile than more broadly diversified companies.