Following the introduction of JMGI's enhanced income policy, Portfolio Manager Austin Forey explains why the Trust remains focused on the same long-term investment process that has guided the portfolio for decades.

JPMorgan Emerging Markets Growth & Income plc (JMGI) attracted industry attention last year when its board announced the move to an enhanced income policy.

That’s welcome news for income-seeking investors, particularly those looking to access a portfolio of high-quality companies listed in emerging markets worldwide whilst still receiving an annual dividend, currently targets an annual dividend of 4% of the Trust’s net asset value* (as defined by the Trust’s distribution policy).

But as Portfolio Manager Austin Forey emphasises, this change has no implications for the way JMGI is managed.

“We’re deploying the same investment process we’ve used for several decades now,” he stresses. “The board has been very clear that it doesn’t want us to narrow the investment universe by focusing on dividend-paying stocks in order to deliver this income.”

Instead, the shareholders’ payout comes from a mixture of ‘natural’ dividend income and capital growth. Paying dividends from capital can reduce the Trust’s NAV, which may limit future capital growth.

Business as usual

It’s therefore business as usual for the management team. Their aim is to identify and hold around 50 of the best growth-focused businesses across the region - those capable of delivering compound growth over the long term, regardless of whether or not they pay a dividend.

It’s a simple philosophy, says Forey. “A company that can reinvest capital and grow its earnings consistently, not just for a year or two but for five, 10, even decades, will produce a much better long-term outcome for shareholders, so that’s the nub of what we try to do.”

But to generate the best returns from such companies, it’s important to pay a sensible price for them, so Forey and his colleagues are always weighing the balance between the value a company is creating, the price of its shares and the extent to which the share price encapsulates the value.

They use various measures to try and assess the quality and potential of a business, but one key element of the process is to understand its competitive advantage and the strength of that advantage.

As Forey explains: “Ultimately, if you have a company that does something better than its competitors, it’s likely eventually to be a much more rewarding investment.”

He gives the example of Taiwan Semiconductor Manufacturing Co (TSMC), now one of the world’s leading producer of advanced semiconductor chips and JMGI’s largest holding1.

“Back when we bought it, it wasn’t such a well-known or large company. But it’s one of the few emerging market businesses to reach truly global-class operations and dominate its market around the world. No one else has come close to being able to replicate its success.”

JMGI’s portfolio typically consists of around 50 stocks, though it can creep up a little if the team finds attractive smaller businesses with growth potential. The team can take such opportunities, even though smaller companies tend to be less liquid, because the investment trust’s ‘closed-ended’ structure means there’s no pressure to have to be able to meet investors’ fluctuating cash demands.

However, adds Forey, “we’re not going to put as much money into a tiny company as we could in a much bigger, more liquid one. So, if that happens the number of stocks will rise slightly.”

Performance upturn

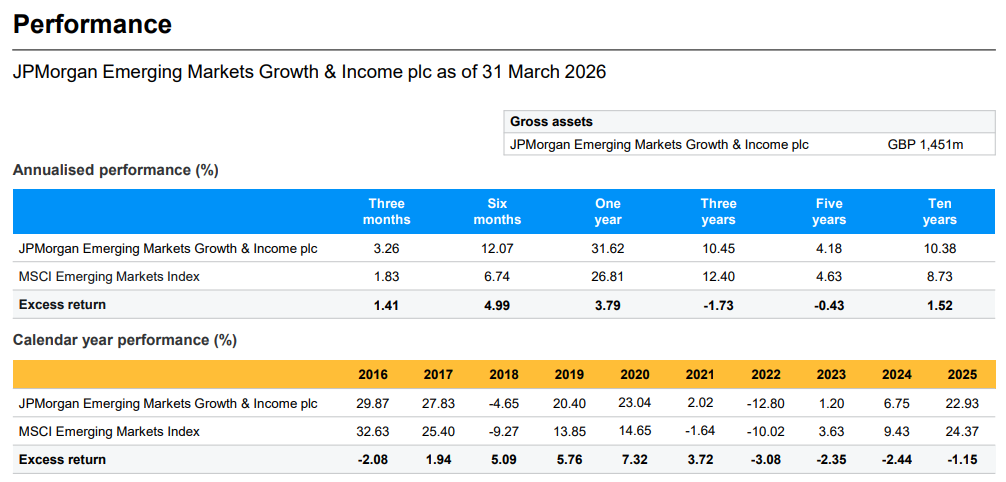

JMGI has been enjoying strong performance recently after several difficult years. Over one year to 31 March 2026, the Trust has outperformed the benchmark MSCI Emerging Markets index2.

Forey says much of the Trust’s challenges over the last few years were rooted in the “exceptionally good” years of 2019 and 2020. “The portfolio was full of businesses that were performing well in their own right, but the market was valuing them more and more highly too – so a lot of the correction of the last four years was that valuation premium coming out of them.”

The good news is that the portfolio’s valuation is now back to where it historically was. “We’re not taking excessive valuation risk anymore and we’d like to think we have achieved that without giving up any of the underlying quality of the businesses we own,” he adds.

Indeed, this is proving to be a good time to buy into interesting parts of the market that the portfolio has not owned for a long time.

The team has taken some profit from its technology holdings, as they have done so well and they consider it important not to end up with a heavy skew to any particular sector. That cash has been redeployed into industrial businesses around emerging markets, “which have led us to a bigger weighting there than we’ve had before.”

Contrarian thinking

A particular coup was Forey’s purchase of shares in longstanding Brazilian oil producer Petrobras at the end of 2025. This was the Trust’s first purchase of an oil company for a decade and the thinking behind this was twofold, he explains.

“First, it has pretty reasonable economics and pays an enormous dividend; the dividend is expected to be an important component of total return”, although it is not guaranteed .

But there was also an element of contrarian thinking. “At the end of last year everyone had given up on oil and the price was right down, in contrast to various other commodities where prices were rising. It was priced for nothing ever improving, so we saw an asymmetrical opportunity, and Petrobras was an interesting and solid way to play it."

- It’s a decision that has contributed positively so far, though outcomes can change quickly given market and geopolitical risks and what has unfolded in 2026 and will help to boost the Trust’s natural income as it embraces its new enhanced dividend policy and remains focused on delivering long-term value for shareholders.

The companies mentioned are for illustrative purposes only, their inclusion is no recommendation to buy or sell.

*Dividend paid by the product may exceed the gains of the product, resulting in erosion of the capital invested. It may not be possible to maintain dividend payments indefinitely and the value of your investment could ultimately be reduced to zero. Dividend payments are not guaranteed.

1 As at 30 April 2026.

2 As at 31 March 2026. J.P. Morgan Asset Management. MSCI. Performance data has been calculated on a NAV Offer net of fees basis in GBP. NAV is the cum income NAV with debt at fair value, diluted for treasury and/or subscription shares if applicable, with any income reinvested. Excess return is calculated geometrically. Performance less than 1 year is not annualised. Inception: July 2010 Past performance is not a reliable indicator of current and future results.

JPMorgan Emerging Markets Growth & Income plc

Summary Risk Indicator

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period.

Investment Objective:

This Company aims to maximise total returns from Emerging Markets and provides investors with a diversified portfolio of shares in companies which the Manager believe offer the most attractive opportunities for growth. The Company can hold up to 10% cash or utilise gearing of up to 20% of net assets where appropriate.

Risk Profile:

- Exchange rate changes may cause the value of underlying overseas investments to go down as well as up.

- Investments in emerging markets may involve a higher element of risk due to political and economic instability and underdeveloped markets and systems. Shares may also be traded less frequently than those on established markets. This means that there may be difficulty in both buying and selling shares and individual share prices may be subject to short-term price fluctuations.

- Where permitted, a Company may invest in other investment funds that utilise gearing (borrowing) which will exaggerate market movements both up and down.

- External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions.

- This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down.

- This Company may also invest in smaller companies which may increase its risk profile.

- The share price may trade at a discount to the Net Asset Value of the Company.

- The Company may invest in China A-Shares through the Shanghai-Hong Kong Stock Connect program which is subject to regulatory change, quota limitations and also operational constraints which may result in increased counterparty risk.