Whilst investors may enjoy the certainty that cash ISAs provide when looking to invest for the long term, there is a risk attached to cash. Over the long term, interest on savings accounts tends not to keep pace with inflation. And that means your cash loses value in real terms. In this article we discuss the merits of taking some investment risk (within a Stocks and Shares ISA) and what factors there might be to consider.

Investment risk and investment return are two sides of the same coin. You won’t see a return on your money unless you put it to work in some way – but if you do so, there is always the chance that something will go wrong and you could lose some or all of it.

However, it’s misconceived to favour the security of cash when planning for your financial future. Sure, saving into a cash ISA or taxable savings account delivers modest returns as recompense for lending to your provider; and if you choose a fixed rate account you even know exactly what those returns will be.

But on a longer view there is a risk attached to cash. Although top interest rates are currently higher than inflation, over the long term, interest on savings accounts tends not to keep pace with inflation. And that means your cash loses value in real terms.

In contrast, when you buy a stocks and shares ISA, you’re effectively backing the future fortunes of companies. There is a greater risk of loss because individual companies can and do fail, but as the annual Barclays Equity Gilt Study1 reveals, history shows that equity investment comfortably outpaces both cash returns (as well as other less risky alternatives such as bonds) and inflation over the decades.

The data shows that over the past 20 years, cash lost almost 32% of its value in real terms – even when interest is added along the way. In other words, £1,000 held in cash from 2005 would have the spending power of just over £680 by 20251.

Over the same 20-year period, the picture looks very different for those who invested. An illustrative portfolio of UK equity investments increased in value by 77% in real terms, turning £1,000 into £1,7701.

Thinking specifically about the relative merits of cash and stocks and shares ISAs, work by Unbiased2 found that over the last 10 years, the average annual return on a stocks and shares ISA has been 6.8%, compared to just 1.8% for a lower risk cash ISA2.

Looking on a short-term basis, over the year to 30 November 2025 the average stocks and shares ISA rose by 15.2%, outpacing the 3.7% rise in value of a cash ISA. However, it is vital to remember that you can’t always count on the stock market and there have been other, recent years when you would have lost money in the average stocks and shares ISA. Simply put, there’s no guarantee that investments will increase in value as they will always be subject to fluctuating market conditions.

Looking beyond capital growth

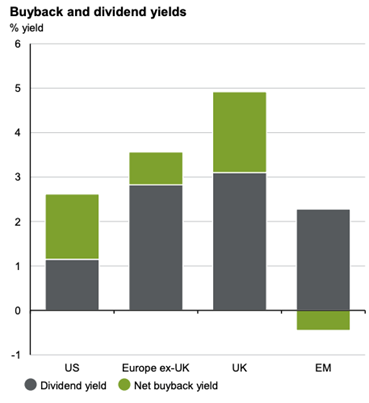

Even if equity price returns are muted against a difficult economic and geopolitical backdrop, total returns can be boosted by an increasingly robust income culture from dividend yields and share buybacks.

For the UK, which leads the global field in this respect, recent data shows combined net dividend and buyback yield at almost 5%. Europe follows at around 3.5%, while the US trails at approximately 2.5%.3

So, to achieve real financial returns you have to accept some risk, or lack of certainty. It’s worth highlighting that investment risk comes in a number of forms beyond the control of individual companies.

For instance, rising interest rates are more painful for young businesses that are borrowing to grow than for more established peers; currency movements may impact the bottom line of companies doing a lot of international trade; high inflation can cause problems for those unable to pass rising costs through to their customers; and a stagnant or struggling economy with declining demand makes it harder for many companies to prosper.

All of which might leave many people wondering how they could possibly sleep at night if they took such a gamble with their money, particularly at times of economic uncertainty and market volatility. But while you’re never going to eliminate investment risk, the good news for anyone who wants to see their money working harder for them is that there are effective ways to manage and mitigate those uncertainties.

Ways to manage risk

The first consideration is around timescales. Historically, the general long-term trend of stock markets is upwards – but it’s by no means a straight line. For that reason, it’s a very bad idea to put money into equities if you might need it within the next few years, because over that timeframe markets may well fluctuate, and with them the value of your investments.

Over decades though, equity investments have the capacity to reward investors in a way that cash cannot, despite what can be pretty painful shorter-term setbacks.

The Barclays Equity Gilt Study figures1 bear that out: those 20-year real gains were made over a period that encompassed several major market shocks including the Global Financial Crisis, Brexit and the COVID-19 pandemic.

A second key principle is that of diversification across a range of investments that respond in different ways to macroeconomic or specific market issues - so although part of your portfolio may struggle, the overall impact is less extreme than if you had all your eggs in one basket.

This can be achieved by spreading your investments not just across a number of companies within a single market, but across different industrial sectors, company sizes, geographical regions and management styles.

Investment trusts run by professional fund managers and held within an ISA wrapper offer a simple and tax-efficient way to access different parts of the equity universe.

Equally importantly, though, diversification should also involve a mix of asset classes – not just shares and short-term cash, but also fixed income investments (bonds), property, maybe private equity or infrastructure.

The idea is that the potentially volatile equity element is partially counterbalanced by other types of asset whose behaviour is not closely correlated or is even negatively correlated to that of equities.

Bonds, for example, deliver more predictable returns and show less volatility than shares, and also often do relatively well when equity markets are falling. As part of a well-diversified portfolio they can help to offset overall losses.

But other factors including your age and your personal feelings about risk also come into play here. If you have decades before you plan to use your investment, and you’re not unduly troubled by the short-term ‘noise’ of market ups and downs, you can afford to hold a higher percentage of equities. As you get older, investment security typically becomes increasingly relevant and the equity element decreases.

Building a risk comfortable mindset

Ultimately, provided you have time and a well-diversified portfolio of high-quality investments on your side, learning to be comfortable with investment risk is a matter of simple discipline.

On the one hand that involves regular portfolio check-ups to make sure your holdings still reflect your timescale and risk appetite, and that they have not become imbalanced (and therefore vulnerable to a correction) because one type of investment has done much better than others.

On the other, it means resisting the temptation to peek frequently, meddle, buy and sell excessively, or panic and run when markets fall. Investing is for the long term, and over the long term investment risk – if properly managed – can be your friend.

If you’re looking for ideas, the JPMorgan range of investment trusts provides rich pickings, with highly experienced managers operating across leading markets worldwide and a focus on hunting down robust, high-quality companies that are well placed to prosper through good times and bad.