High growth potential, rapid digitalisation, structural reform, and improving corporate quality continue to reinforce India’s powerful investment case.

This is a marketing communication

With its recent adoption of the 4% enhanced dividend policy, JPMorgan Indian Growth & Income (JIGI, formerly JPMorgan Indian Investment Trust) appears well-placed to reward both new and existing investors in the months and years to come.

There are several strands to JIGI’s attractions for shareholders. One obvious one is the dividend target of at least 4% of net asset value, paid quarterly* - although not guaranteed it provides the prospect of steady returns, regardless of equity market vagaries.

But the trust’s biggest allure is the exposure it provides to India’s extraordinary growth and continuing macroeconomic success story.

A compelling economic backdrop

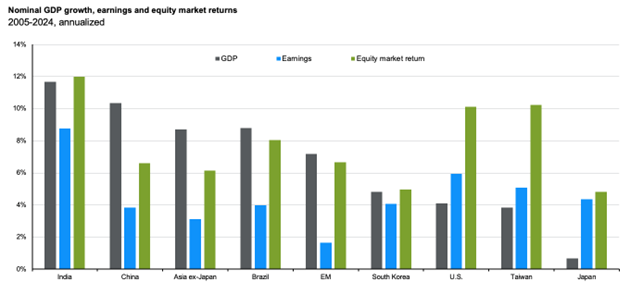

As Claire Peck, an investment specialist on JIGI, observes, India has one of the world’s fastest-growing economies in terms of GDP growth, at almost 12% nominal (meaning it is not adjusted for inflation) -annualised between 2005 and 2024¹.

Looking ahead, moreover, there’s every indication that the subcontinent will retain pole position. JIGI co-portfolio manager Amit Mehta believes that 6% real economic growth (10-11% nominal) is “well underpinned” for some years to come. “I’m pretty confident that the economic pillars of high rates of economic growth remain in place,” he commented in the 2025 AGM presentation.

Crucially for equity investors, corporate earnings growth has also been ahead of the pack over the past 20 years, averaging more than 8% a year¹.

“It’s that combination of high growth and high returns which is important, because that has translated into high stock market returns, even better than US equities over the last 20 years,” Peck explains.

Structural reform in action

This dynamism has been driven by the far-reaching structural reforms introduced by the current government since it came to power in 2014. These have laid the foundations for the sustainability of the country’s macroeconomic growth and company productivity gains.

Peck points to several key strands, but perhaps most notably India’s Aadhaar system – the world’s largest biometric digital identity system. This now extends to almost the entire 1.4 billion population, enabling streamlined and fraud-resistant access to government services and financial services.

To put its impact into context, she gives the example of bank account penetration, “which has risen from 35% in 2011 to around 80% in 2024”².

At the same time, India’s wider economy is becoming increasingly digitalised and is moving away from its previously heavily informal basis towards a more formal corporate footing.

Such ‘formalisation’ provides the government with a broader base for raising revenue through taxation. Indeed, a second key element of the reforms has been the introduction of the Goods and Services Tax (GST), which has underpinned extensive infrastructure investment.

Peck highlights a further factor, in the shape of India's UPI instant payment system: “As a consequence, India has the world’s largest market share of digital payments, at 46%²,” she says.

The trend towards a more formal economy has also led to the ‘financialisation’ of savings, away from traditional asset choices such as gold or real estate and towards the equity markets.

A record USD 3 billion³ is currently flowing into the markets per month from Indian investors’ Systematic (regular) Investment Plans. Such reliable investment flows themselves help to improve market resilience, Peck notes.

Fertile hunting ground for stock pickers

At a corporate level, this favourable economic backdrop provides “a fertile hunting ground for stock pickers like us”, she adds.

Various factors play a part, including the depth and choice offered by the Indian market, the relative maturity of its listed companies in an emerging market context, and the huge scope for gains in productivity across many industries and basic services.

“The market doesn’t give enough credit to management alpha – the ability of the many high-quality management teams there to take advantage of these inefficiencies,” Peck comments. “it’s another way to add value to a portfolio.”

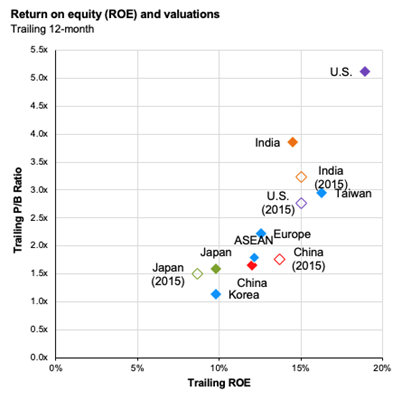

The upshot is that in terms of returns on equity, Indian companies are typically among the most profitable emerging market businesses and indeed not far behind the US⁴.

They also lead in regard to quality. When assessing businesses, JPMorgan analysts use a four-category classification system ranging from ‘challenged’ up to ‘premium’. As Peck reports: “India stands out as having the highest percentage of premium-classified companies of any emerging market.”

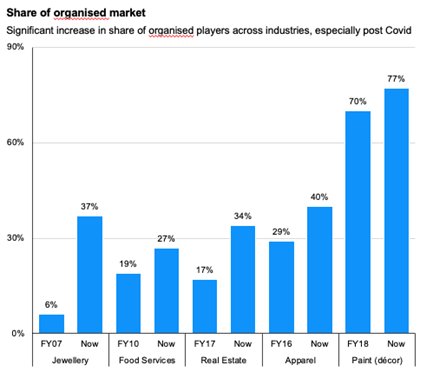

Economic formalisation across the broad spectrum of consumer-focused industries over recent years (spurred on by the introduction of GST) is also helping to enrich the choice available to stock-pickers, as more companies list on the stock exchange. A good example is the real estate sector, which has seen the market share of listed businesses double from 17% in 2017 to 34% now⁵.

JIGI: Taking advantage of the world’s most powerful growth engine

As bottom-up stock pickers, the JIGI team tap into these structural growth opportunities through four main themes.

Lifestyle upgrades are very much in evidence across the subcontinent as living standards rise: Peck forecasts there will be an additional 114 million middle-income and 50 million higher-income households by 20305.

Increasing demand for premium goods and services is an obvious outcome of that trend, and the portfolio taps into it via holdings such as leading online travel agency Make My Trip.

Financial deepening is another ongoing trend, as growing numbers of Indians take advantage of investment and banking services. Again, there is enormous potential for expansion: Peck points out that assets under management in India’s mutual fund industry currently amount to just 20% of Indian GDP, compared with 59% in the UK and a whopping 124% in the US. JIGI’s portfolio includes the likes of top Indian asset manager HDFC6.

Its fixed asset creation theme focuses on the industrial companies benefiting from the government’s huge infrastructure investment plans on the back of the GST, for example through Blue Star, one of the largest cooling businesses in the country.

Finally, catering for the outsourcing and offshoring technology requirements of western businesses is a longstanding industry for India, with increasing diversification to other areas such as healthcare. “It’s a field still very rich in opportunities for us,” observes Peck.

There are of course specific risks attached to any single-country investment trust, and especially those focusing on emerging markets, which are by definition less mature and more volatile than their developed counterparts.

Macroeconomic headwinds currently on the JIGI team’s radar include the highly uncertain global trade environment, particularly the 50% tariffs on Indian exports to the US that were imposed in 2025. Additionally, India’s private investment cycle has picked up more slowly than expected, while corporate valuations, although less frothy than they were a year ago, remain elevated.

Nonetheless, for the JIGI team there remains a wealth of reasons why India remains a wonderful market for long-term investors looking for a robust portfolio of quality and growth investments.

With the backing of 18 expert analysts both on the ground in India and in London, plus the rich resources of the wider J.P. Morgan Asset Management global research platform to draw on, not to mention the added benefit of a regular dividend, JIGI is well positioned to seek strong and sustainable returns over the long term.

* Dividend paid by the product may exceed the gains of the product, resulting in erosion of the capital invested. It may not be possible to maintain dividend payments indefinitely and the value of your investment could ultimately be reduced to zero. Dividend payments are not guaranteed.

Sources:

1 Source: FactSet, MSCI, World Bank, J.P. Morgan Asset Management. Earnings and equity market returns are represented by each market’s respective MSCI index. Nominal GDP growth, equity returns and earnings growth are calculated in local currency except for Asia ex-Japan and emerging markets, which is in U.S. dollars. GDP for Asia ex-Japan is calculated by adding up nominal GDP in USD for all the 10 markets which are tracked by MSCI Asia ex-Japan. GDP for EM is calculated by adding up nominal GDP in USD for all the 24 markets which are tracked by MSCI EM. Data are as of April 30, 2025.

2 J.P. Morgan Asset Management, Riding India’s growth wave, August 2025:

3 Reuters, How long can homegrown investors hold up India’s equity market? 6 February 2025: https://www.reuters.com/world/india/how-long-can-homegrown-investors-hold-up-indias-equity-market-2025-02-06/

4 FactSet, MSCI, J.P. Morgan Asset Management. Data are based on respective MSCI data, except U.S., which is represented by the S&P 500 Index. Filled diamonds represent latest data while unfilled diamonds represent historical comparisons. Guide to the Markets – Asia. Data reflect most recently available as of June 30, 2025.

5 BoFA. Data as of May 2025.

6 Boston Consulting Group (BCG) “The New Indian: The Many Facets of a Changing Consumer” (2023)

7 Source: IMF, IIFA, RBI, CRISIL Intelligence. Note: AUM data as of September 2024 for all countries; only open-ended funds have been considered. Includes equity, debt and others, GDP taken from IMF (Gross Domestic Product at current prices). Penetration calculated as Mutual Fund AUM divided by GDP, for India the value is calculated as Mutual Fund AUM to GDP (at current prices).

The securities above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

Past performance is not a reliable indicator of current and future results.

Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met.

Image source: Shutterstock

Summary Risk Indicator

The risk indicator assumes you keep the product for 5 year(s). The risk of the product may be significantly higher if held for less than the recommended holding period.

Investment Objective: Aims to provide capital growth from Indian investments by outperforming the MSCI India Index. The Company will invest in a diversified portfolio of quoted Indian companies and companies that earn a material part of their revenues from India. The Company will not invest in other countries of the Indian sub continent including Sri Lanka. The Company has the ability to use borrowing to gear the portfolio to up to 15% of net assets where appropriate.

Risk Profile:

- Exchange rate changes may cause the value of underlying overseas investments to go down as well as up.

- Investments in emerging markets may involve a higher element of risk due to political and economic instability and underdeveloped markets and systems. Shares may also be traded less frequently than those on established markets. This means that there may be difficulty in both buying and selling shares and individual share prices may be subject to short-term price fluctuations.

- External factors may cause an entire asset class to decline in value. Prices and values of all shares or all bonds and income could decline at the same time, or fluctuate in response to the performance of individual companies and general market conditions.

- This Company may utilise gearing (borrowing) which will exaggerate market movements both up and down.

- This Company may also invest in smaller companies which may increase its risk profile.

- The share price may trade at a discount to the Net Asset Value of the Company.

- The single market in which the Company primarily invests, in this case India, may be subject to particular political and economic risks and, as a result, the Company may be more volatile than more broadly diversified companies.