Head of International Liquidity Fund Management

In Brief

- Central banks face a dilemma as the Middle East conflict and closure of the Strait of Hormuz drive oil prices higher and supply lower, fueling inflation and threatening growth.

- Most central banks are adopting a “wait and see” approach, wary of hiking rates into a slowdown but alert to inflation’s second- round effects, although this could leave them vulnerable to being overtaken by events as the situation evolves.

- Policy responses have varied based on starting positions: the US and UK start from a slightly restrictive stance, the EU is neutral, and Australia remains loose, shaping their reaction to the crisis.

How central banks are navigating the Middle East crisis and oil shock

The ongoing conflict in the Middle East and the closure of the Strait of Hormuz have sent shockwaves through global energy markets. Oil prices have surged to multi-decade highs, while supply disruptions threaten to ripple across economies worldwide.

Central banks now face a complex challenge: higher energy costs are pushing inflation up, with potential second-round effects on food and broader prices, and even third-round impacts on wages. Yet, the longer-term consequence of elevated prices and constrained supply is slower economic growth.

For now, central banks are emphasizing data dependency. They are holding interest rates steady and emphasizing flexibility as they wait for clearer signals before acting. The risk remains that prolonged uncertainty could leave them caught in the headlights, hesitant to act decisively.

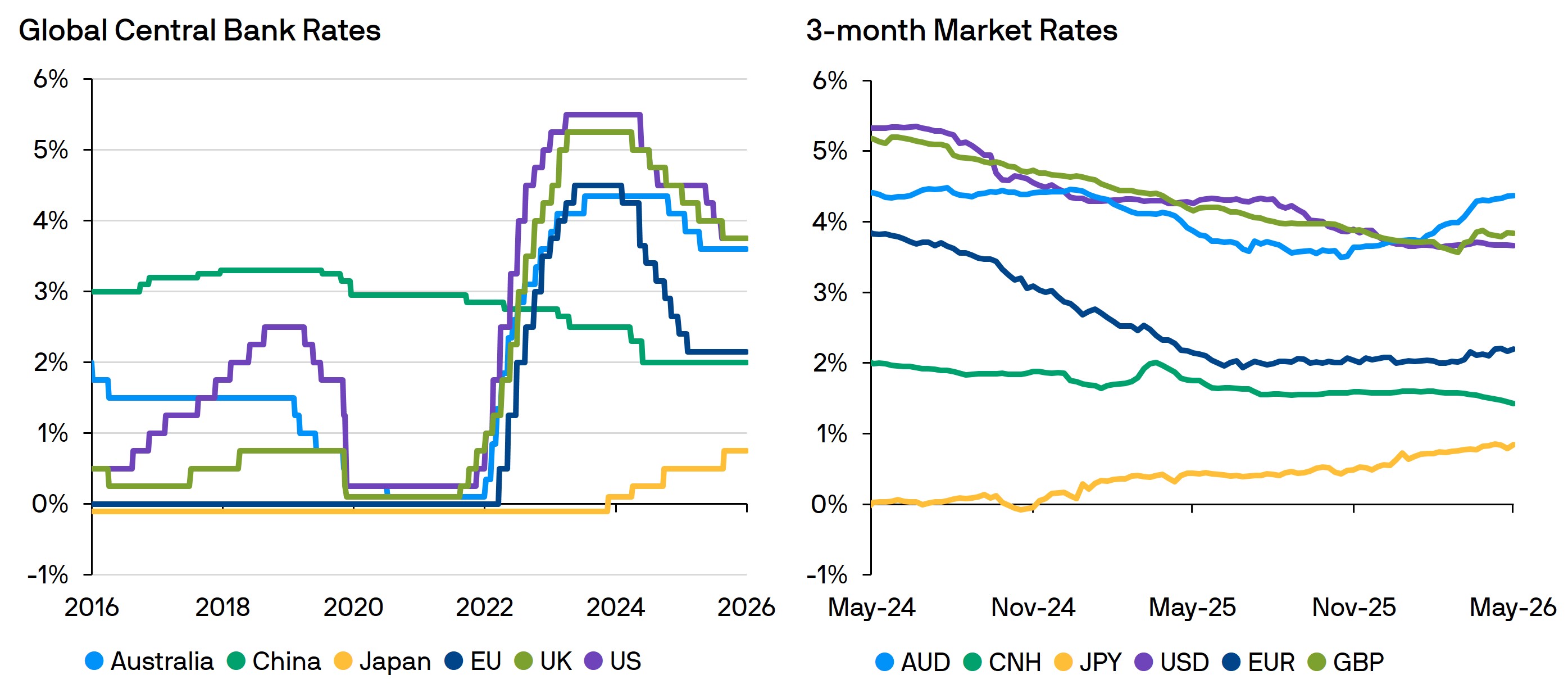

Key central bank outlooks

United States: At its latest meeting, the Federal Reserve (Fed) held rates steady, with a hawkish tilt. as it debated shifting from an easing to a neutral stance. Its statement noted persistent inflation, mainly from higher energy prices, and a labor market that remains stable but subdued. The probability of rate cuts has been unwound. Market pricing now implies a slight chance of hikes, reflecting the Fed’s reluctance to commit to a rate path amid uncertainty. The slightly restrictive stance gives the Fed some flexibility. Rate cuts remain the most likely next step.

European Union: The European Central Bank (ECB) also kept rates unchanged at its most recent meeting. It emphasized a data-dependent, meeting-by-meeting approach. The conflict has created significant upside risks to inflation and downside risks to growth, due to Europe’s dependence on imported energy. Headline inflation is rising, while core inflation is edging down and growth is slowing. The ECB’s neutral starting point allows flexibility, but policymakers are cautious and are seeking more evidence on second-round effects before moving. Markets are pricing in two to three hikes by year-end, and while the ECB is non-committal, early rate hikes are increasingly likely.

United Kingdom: The Bank of England (BoE) held rates in late April. It emphasizes a readiness to act if second-round effects on prices and wages become persistent. Given significant uncertainty, the BoE indicated potential scenarios ranging from inflation peaking at 3.6% to a severe case where inflation peaks at 6.2% and remains elevated. All scenarios imply rate hikes are likely, but the BoE’s slightly restrictive stance and weaker demand suggest less tightening than markets imply.

Singapore: The Monetary Authority of Singapore (MAS) pivoted hawkish at its early April meeting. It increased the S$NEER appreciation rate to counter imported inflation from energy shocks. Growth is robust but expected to moderate, and inflation forecasts have been raised. The MAS’s tightening bias is tempered by caution, given downside risks to growth. This suggests the timing and pace of further hikes remains uncertain.

Australia: The Reserve Bank of Australia (RBA) has raised the Overnight Cash Rate (OCR) at three consecutive meetings, returning rates to their previous cycle high of 4.35%. This decisive action was driven by a material pickup in inflation, fueled by persistent capacity pressures and sharply elevated fuel prices stemming from the ongoing conflict in the Middle East. Risks are tilted to the upside, and RBA’s guidance remaining hawkish amid signs of second-round impacts and rising inflation expectations. With rates returning to restrictive territory, if inflation pressures abate, the earlier and rapid pace of tightening could allow the RBA to return to steady hold.

China: The People’s Bank of China (PBOC) entered 2026 with a dovish bias, with investors anticipating rate cuts to support growth and reduce deflation. First quarter growth met government targets, driven by resilient exports and tentative stabilization in the property market. This helped offset subdued domestic demand. Meanwhile, inflation turned positive, easing deflation concerns. China remains more insulated from the Middle East conflict and higher energy prices than most markets, though uncertainty around external demand persists. Although the PBOC maintains a dovish stance and real rates remain restrictive, further rate cuts are unlikely as growth remains on track.

Japan: After raising base rates to a multi-decade high of 0.75% by the end of 2025, the Bank of Japan (BOJ) kept rates unchanged at its latest meeting. This decision was due to concerns about the Middle East conflict’s impact on growth. But the hawkish 6-3 split, with three members voting for a hike, underscores the bank’s dilemma. Consumer confidence is plunging amid renewed cost of living worries, despite government subsidies and oil releases from the strategic reserve that are temporarily suppressing prices. Inflation remains stubbornly above target, and real rates are still negative. The BOJ is likely to continue normalizing interest rates at upcoming meetings.

Fig 1: Rates are on the move

Source: BOE, BOJ, ECB, Fed, PBOC, RBA, Bloomberg, J.P. Morgan Asset Management; data as of 6 May 2026.

Implications: Hike first, cut later?

Central banks are caught in a bind: hiking rates risks choking off growth, but failing to act could let inflation spiral. Most are opting for caution, holding rates steady and signaling flexibility. The starting point—restrictive in the US, UK and China, neutral in the EU, loose in Japan and Australia—shapes their response. All are watching for second- and third-round effects. If inflation persists, expect more hikes in 2026; if growth slows sharply, cuts could follow in 2027. For investors, this means volatility and uncertainty: defensive positioning, liquidity, and tactical duration extensions are key as central banks navigate the crossfire of geopolitics and economics.