Explore the key characteristics of money market funds

Money market funds are highly regulated, actively managed pooled mutual funds that invest in diversified portfolios of short-term, high-quality debt instruments, with the aim of preserving capital, providing a high degree of liquidity and generating competitive returns relative to other cash equivalents.

They are structured as independent corporate entities, with boards of directors to safeguard the interests of individual shareholders, while assets are ring-fenced and held remotely from the asset manager’s own balance sheet.

Capital preservation

Money market funds primarily invest in a diversified range of short-tenor, high-quality securities to protect capital, which is of paramount importance to liquidity investors.

Leading money market fund managers will also conduct their own credit analysis in addition to considering ratings from independent credit rating agencies. A manager’s in-house credit analysis capability is an important point for investors to consider when choosing a money market fund.

Liquidity

Money market fund investors require a high level of liquidity and therefore money market funds typically offer same day (T+0) or next day (T+1) access.

This level of liquidity is particularly helpful for treasury teams when the ability to accurately predict cash flows is difficult.

Money market fund portfolio managers are able to offer this facility by maintaining high levels of daily and weekly liquid assets while investing in securities that are easily liquidated, if necessary.

In addition to daily liquidity, money market funds may also have later cut-off times than some alternative cash investment options, meaning that treasury departments have more time during the day to make decisions regarding the company’s liquidity needs.

Diversification

While it doesn’t guarantee positive returns or eliminate risk of capital loss, diversification is critical to preserving capital, generating returns and ensuring liquidity.

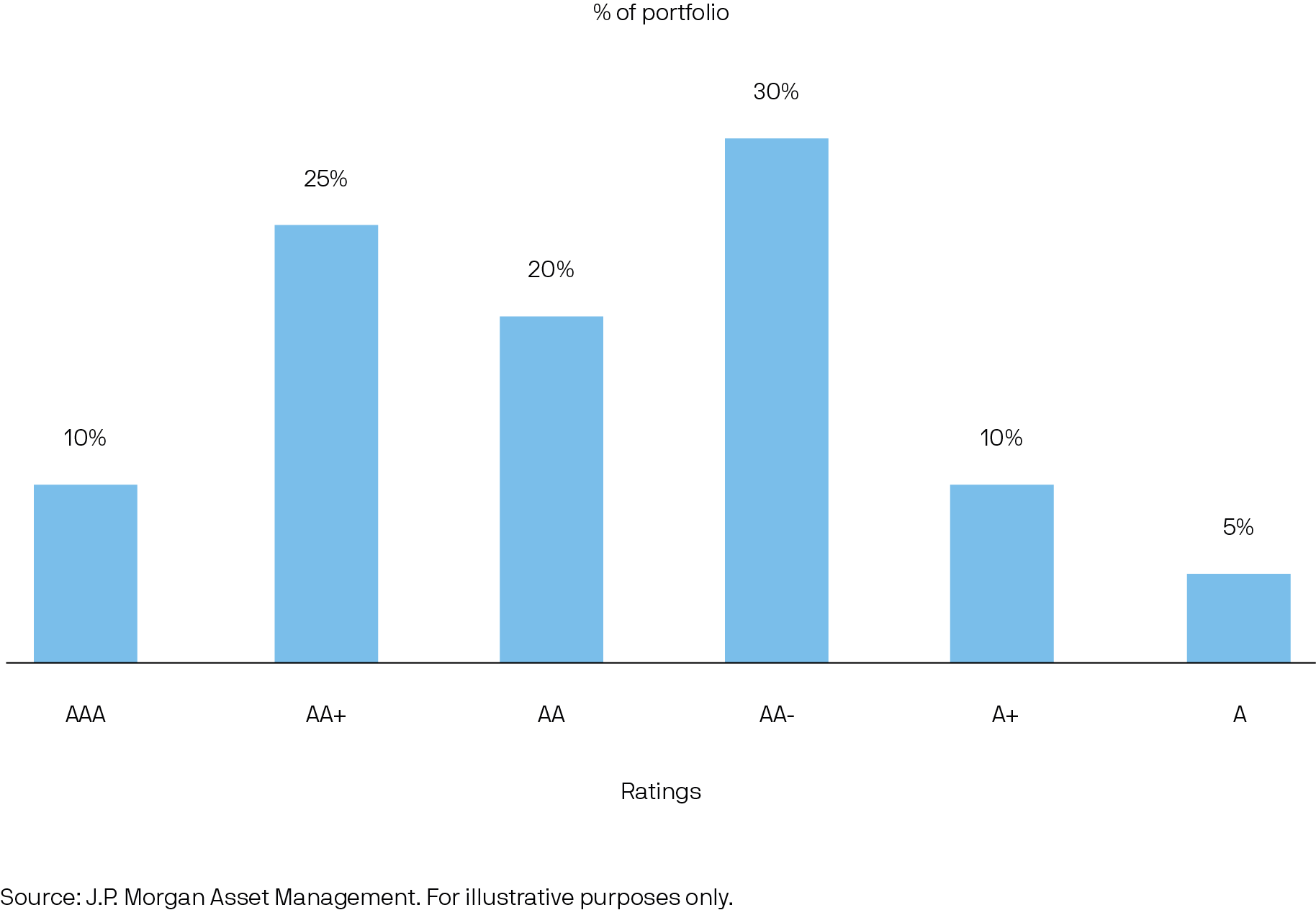

Money market funds hold a highly diversified range of securities from a wide range of issuers and maturities and focus on securities with the highest short-term credit ratings available, allowing investors to participate in a more diverse portfolio than they could achieve individually.

For example, a money market fund is generally permitted to hold no more than 5% in a single issuer (there are exceptions for repurchase agreements and overnight bank deposits, as well as for government securities).

Active fund management

Active fund management is essential to ensuring the key objectives of a money market fund — capital preservation, liquidity and return maximisation — can be achieved.

Money market fund portfolio managers will actively adjust the fund’s exposure to different issuers and sectors depending on their credit outlook. Active managers will also adjust the maturity of investments and the duration of the fund to reflect interest rate views and the expected cash inflows and outflows of the fund.

For example, in times of market volatility or uncertainty, the amount of liquidity held will typically be increased.

A money market fund can free treasury professionals from the business of evaluating counterparties and trading securities — while offering a high degree of transparency. As a result, money market fund providers have become even more transparent about their underlying investments and usually provide holding reports detailing the underlying securities on a monthly or more frequent basis.

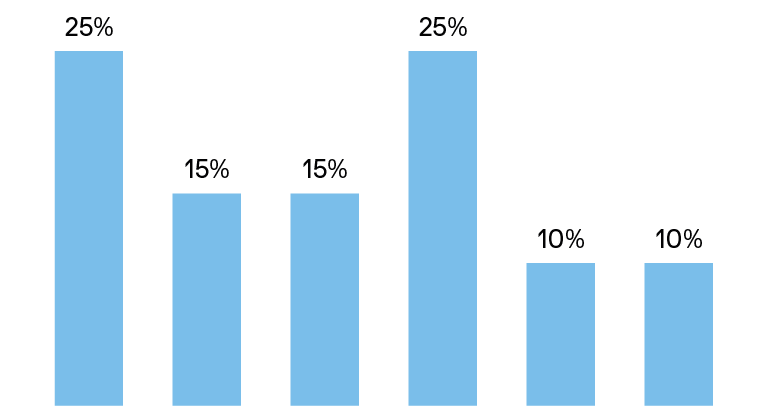

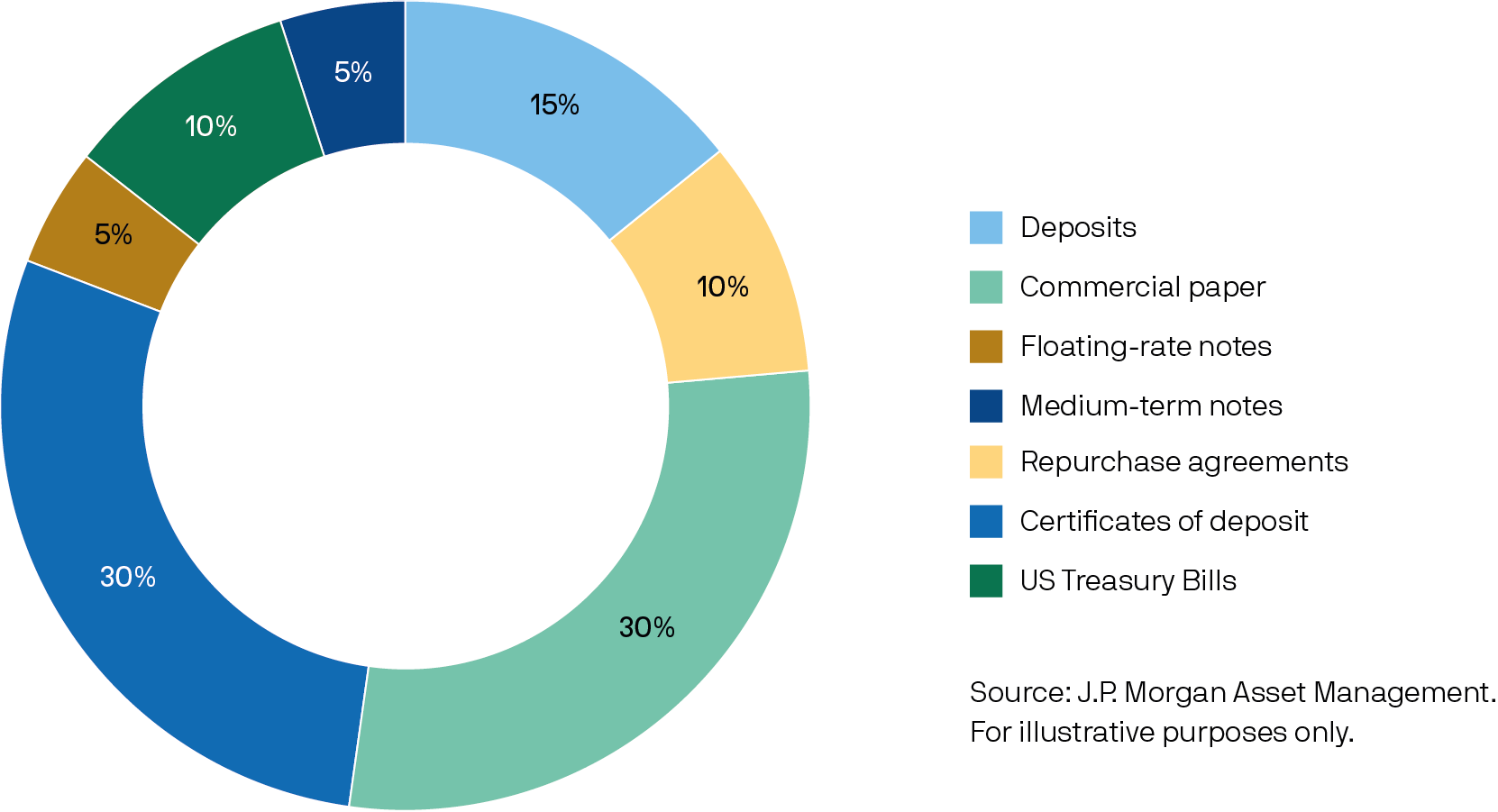

A typical money market fund portfolio

Money market funds aim to provide liquid homes for cash investments by holding highly diversified portfolios of short-term debt instruments from a broad range of highly-rated issuers, including governments, financial institutions and high quality corporations.

Typical money market fund securities

Money market funds may hold multiple types of short-term securities (usually with less than one-month maturity). Typically, these securities could include commercial paper, certificates of deposit, floating rate notes, medium-term notes, repurchase agreements (repos), agency securities, and government bonds or Treasury bills.

| Commercial Paper (CP) | Certificate of Deposit (CD) | Government bills | Floating-rate notes (FRNs) | Repurchase agreements (Repos) | Asset-backed commercial paper (ABCP) | Medium-term notes (MTNs) | |

|---|---|---|---|---|---|---|---|

| Summary | Tradable promissory notes | Similar to term bank deposits and can be traded on the secondary market | Short-term fixed interest securities often known as Treasury bills in the US | Securities that rest their rate of interest periodically | Agreement between two parties to sell and repurchase a security with interest. MMFs typically do reverse repos, lending cash and taking in collateral | A bankruptcy remote special purpose entity which issues commercial paper and uses the proceeds to acquire a portfolio of assets, such as receivables, securities and loans | Securities that are issued with fixed interest rates |

| Features | Highly liquid Allows diversification across different industries Wide range of maturities allows terms to be targeted precisely | Highly liquid – issuing bank often willing to repurchase before maturity | Liquid and highly active market Sovereign issuer Wide range of maturities Low risk reflected in low yield | Attractive when interest rate outlook is uncertain Variable rate makes them less exposed to interest rate risks | Negotiated individually so interest and term can be highly tailored MMFs usually only have government debt as collateral, which is typically priced at a discount for additional security Ultra-short duration funds can do non-traditional repos | Backed by collateral or financial assets, such as trade receivables (bills) Contains liquidity and credit support features designed to cover asset / liability mismatches between the underlying collateral cash flow and the ABCP, as well as the credit performance of the collateral | Highly liquid Allows diversification across different industries Wide range of maturities |

| Maturity | Overnight to one year (typically <95days) | One day to two years | Four weeks to one year | Typically one year or greater | Overnight to one year, typically overnight | One day to two years | Typically one year or greater |

| Issued by | Corporate and financial institutions, agencies and supranationals | Banks | Governments | Corporate and financial institutions, agencies and supranationals | Financial institutions | Special purpose vehicle established by a highly-rated financial institution | Corporates, financial institutions, agencies and supranationals |

| Interest rate | Fixed | Fixed* | Fixed | Variable | Fixed | Fixed | Fixed |

| Interest paid | At maturity** | At maturity | At maturity** | During term | At maturity** | At maturity** | During the term or at maturity** |

* Certificates of Deposit can be issued as fixed or floating and with coupon or at a discount. ** Via the security being issued at a discount to face value. Source: J.P. Morgan Asset Management. For illustrative purposes only. These investment examples are included solely to illustrate the investment process and strategies which may be utilized by the Fund. Please note that these investments are not necessarily representative of future investments that the Fund will make.

The importance of correct benchmark selection

The vast majority of asset managers invest portfolios vs. a benchmark, which helps managers understand how they will be judged and organisations understand how managers are performing. Therefore, selecting the correct benchmark is a critical decision. Fixed income investors have a large range of indices available, but the choices for liquidity and ultra-short duration investors are significantly more limited, amplifying the challenge of assessing the risk and return of these strategies. Nevertheless, correctly identifying key investment goals and carefully selecting an appropriate benchmark can help minimise these limitations.

-

Matching the benchmark to the investment strategy

-

What makes a good benchmark?

-

Challenges for liquidity and ultra-short duration investors

-

Using a Treasury Bill-based index as a liquidity benchmark

-

Conclusion

Matching the benchmark to the investment strategy

Once an organisation has chosen an appropriate portfolio strategy that fits its investment objective and investment policy, the next step is considering a benchmark in line with the strategy’s long-term goals (Exhibit 1).

Exhibit 1: An appropriate benchmark helps investors work towards long-term goals

Source: J.P. Morgan Asset Management. Data as of 31 July 2025. For illustrative purposes only.

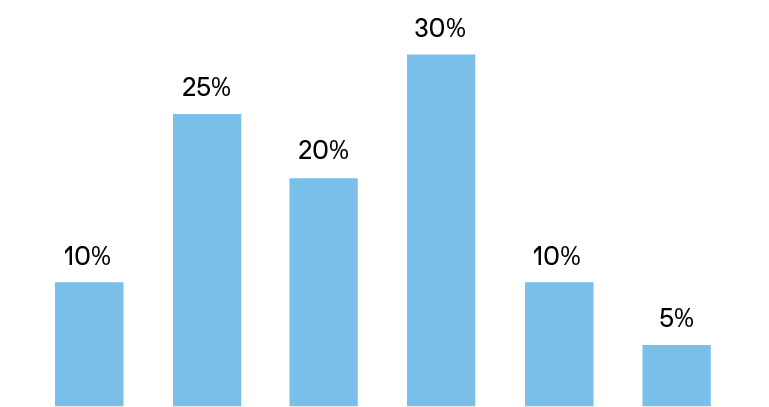

Selecting an appropriate benchmark is critical for several reasons. First, a benchmark helps investors separate risks and returns into manageable objectives (Exhibit 2). Second, a benchmark also allows fund managers to understand how their performance and risk allocations will be assessed; thirdly it provides investors with a method for measuring performance. Finally, having a benchmark also establishes a neutral position for the portfolio manager, which is still in-line with an investor’s long-term goals.

Exhibit 2: Benchmarks help separate returns and risks into manageable objectives

Source: J.P. Morgan Asset Management. For illustrative purposes only.

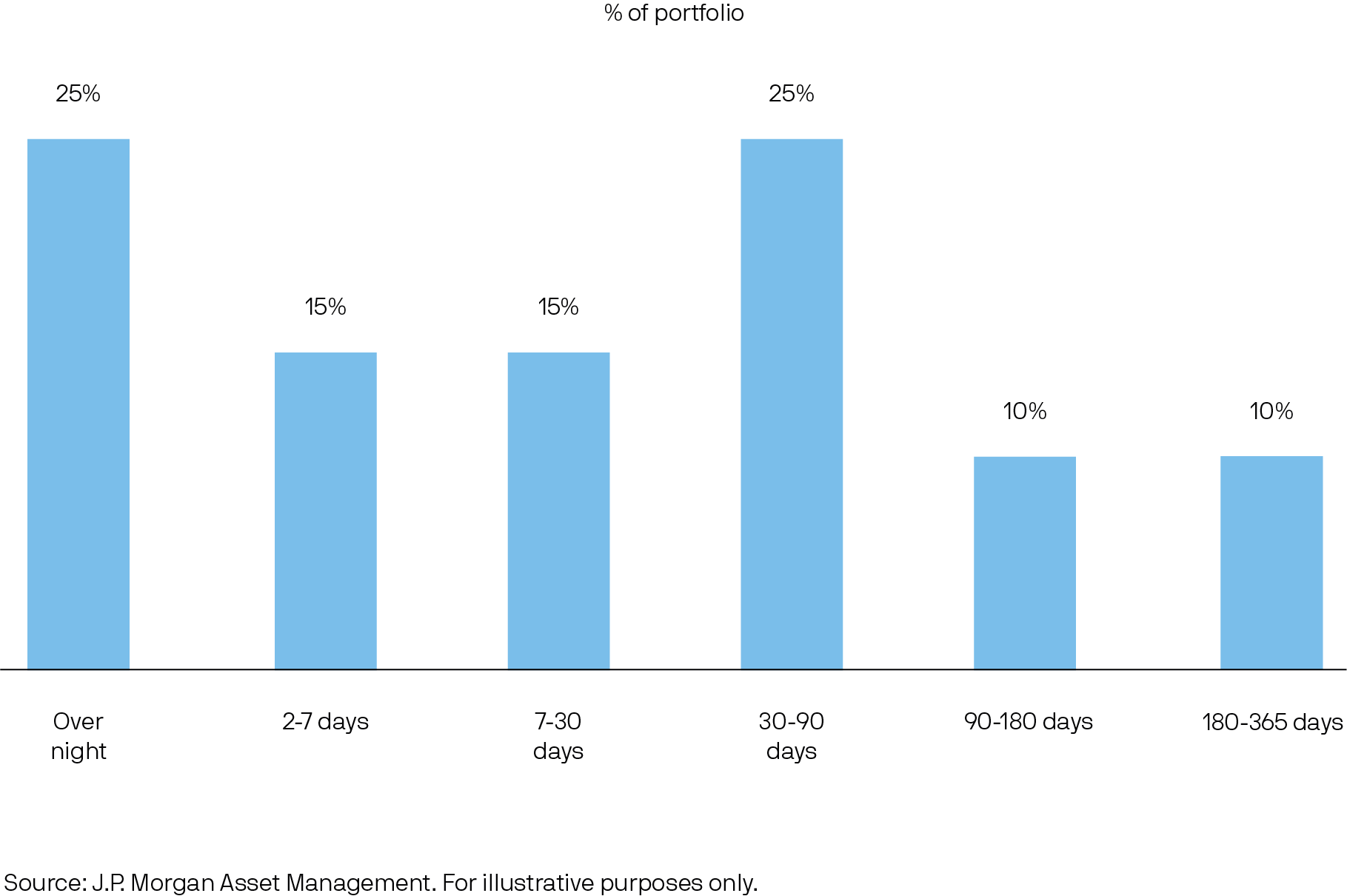

Key factors when selecting an appropriate benchmark include the investor’s risk tolerance and return objective. The characteristics of the benchmark, including duration, maximum and minimum maturities, credit quality and range of issuers, should be aligned with the investor’s guidelines (Exhibit 3).

Exhibit 3: Properly aligning the benchmark and guidelines is important to ensure effective investment:

Source: J.P. Morgan Asset Management. Data as of 31 July 2025. For illustrative purposes only.

What makes a good benchmark?

The most useful indices are consistent, comprehensive, relevant, replicable and measurable. Bond indices achieve these characteristics with clear rules that determine which securities can be included – typically based on the debt outstanding, credit rating, time to maturity and issuer type. A well-constructed benchmark can help to closely align market movements and key drivers of a portfolio’s performance (Exhibit 4).

Exhibit 4: A well-constructed bond benchmark can help align portfolio returns with market movements

Source: J.P. Morgan Asset Management. Data as of 31 July 2023.

Bond indices are typically provided by brokers or securities pricing providers, both of which can efficiently monitor and accurately price the securities in the index. An active portfolio manager can then underweight or overweight duration, sectors and issuers vs. the benchmark in an effort to manage risk and/or improve returns.

The number of bond market indices has increased dramatically over the past decade as bond markets increase in size and the desire for customised benchmarks has grown. Investors have a wide range of appropriate indices to choose from – either pre-existing or customised – to closely match their risk and return goals.

Challenges for liquidity and ultra-short duration investors

For money market investors, the potential range of benchmarks is significantly smaller due to several factors. First, many brokers are reluctant to price and trade shorter-term securities which are likely to be held to maturity by investors and have much shorter tenors – necessitating more frequent benchmark rebalancing. Second, short-term security issuance is dominated by money market instruments like commercial paper (CP) and certificates of deposit (CD), where data on issuance, pricing and liquidity may be scarcer.

These factors imply that fixed income indices with average maturities of less than one year are dominated by deposit rate indices, interest rate indices and Treasury Bill indices. Moreover, the majority of these indices may not exist outside of the US due to a lack of liquidity, limited number of suitable data points and lack of broker engagement.

While simple to use and readily available, indices based on deposit rates and interest rates are limited by their inability to capture credit, duration and other fixed income risks, making them unsuitable benchmarks, especially during periods of volatile interest rates (Exhibit 5) and credit spread. Deposit rates are also dependent on specific bank funding costs which may not be representative of broader market conditions. These costs can also be impacted by seasonal, regulatory and local market factors. By combining multiple bank fund rates or using actual trade data, interest rate indices (e.g., SOFR, LIBOR, etc.) seek to mitigate the idiosyncratic characteristics of deposit rates. However, both these benchmarks suffer similar disadvantages – they are unable to capture capital gains and losses, which can magnify tracking error during periods of interest rate and credit spread volatility.

Exhibit 5: Indices based on deposit rates and interest rates only capture return due to yield, while failing to capture capital gains and losses

Source: J.P. Morgan Asset Management. Data as of 31 July 2023.

Using a Treasury Bill-based index as a liquidity benchmark

Treasury Bill-based indices are a better alternative. Treasury Bills are available in most local currency markets and are typically regarded as the most liquid and highest-quality debt, which also contributes to accurate and fair pricing. Meanwhile, in contrast to deposit and interest rate indices, Treasury Bill indices – which are based on actual securities – more accurately replicate the impact of both yield and changes in yield.

While Treasury Bill indices do not capture credit risk, fortunately, the impact of credit spread movements is relatively limited for money market investments given their focus on very short tenor and high credit quality issuers.

Exhibit 6: Treasury Bill indices capture key drivers of return including yield and duration, with longer-maturity returns exhibiting more volatility during periods of interest rates instability

Source: J.P. Morgan Asset Management. Data as of 31 July 2023.

Conclusion:

Selecting a suitable benchmark is critical step towards achieving long-term strategic investing goals. Although, the choice of benchmarks is more limited for liquidity and ultra-short duration investors, choosing a benchmark that accurately captures key drivers of return is important to fairly analyse risks, returns and the performance of investment managers.