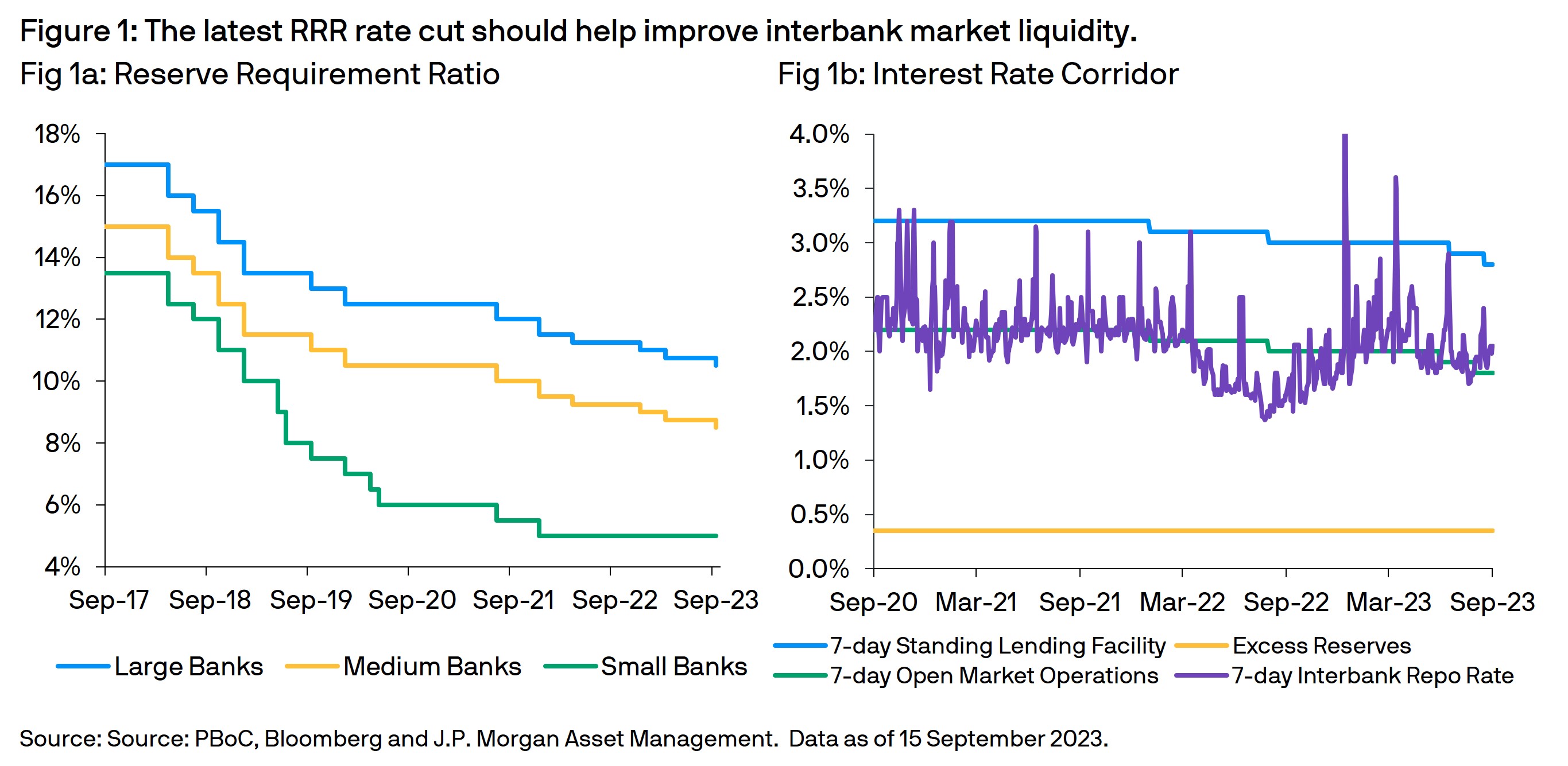

On 14 September 2023, the People’s Bank of China (PBoC) announced a broad based 25bps Reserve Requirement Ratio (RRR) rate cut. Despite the probability of an RRR cut was widely anticipated, the timing was unexpected as was the shortness of the notice period, with the cut effective from 15 September. This was the second RRR cut in 2023 and will release additional liquidity into the banking system, while reducing commercial bank funding costs. In the accompanying statement, the PBoC confirmed the rate cut would help “maintain liquidity at a reasonably adequate level and credit growth at a reasonable pace to facilitate both quantity and quality improvement of the economy".

Technical and fundamental support:

The RRR rate cut will reduce the weighted average RRR rate from 7.60% to a new record low 7.40%. For large and medium banks, their RRR will decline to 10.50% and 8.50% respectively; while small banks’ ratios will remain unchanged at the RRR floor of 5.00%. Fundamentally, the cut should release approximately CNY500bn of additional, long-term liquidity and reduce bank funding costs. Technically, the extra liquidity should help ease tight funding conditions in the intra-bank markets and ensure adequate funds to absorb the planned increase in government bond issuance.

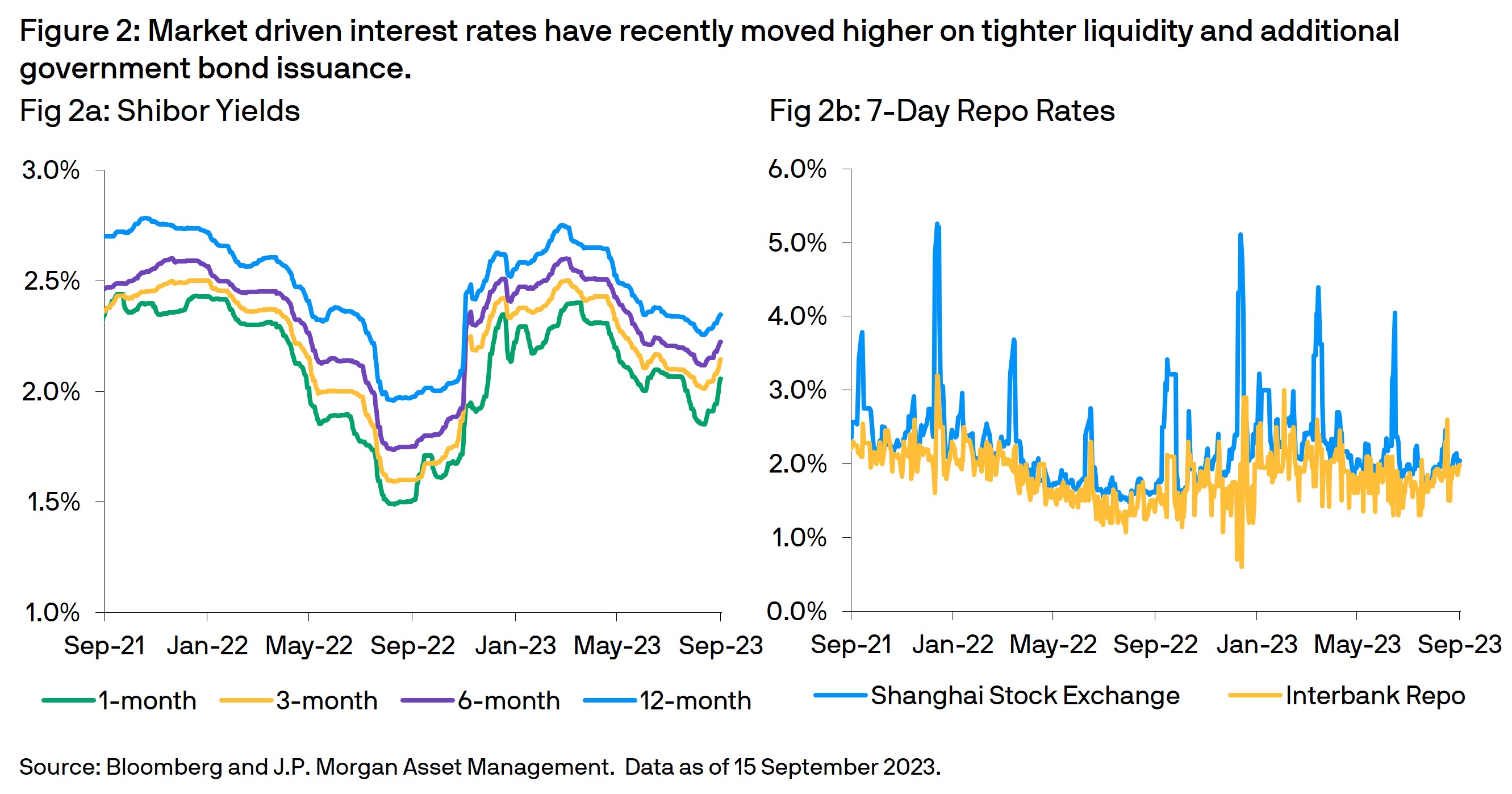

Following the rate cut, the currency strengthened versus the USD and bond yields were broadly unchanged. Meanwhile, repo and SHIBOR yields, which had recently moved higher on tighter interbank liquidity conditions, declined slightly. Subsequently, on 15 September, the PBoC left the one-year Medium Term Lending Facility (MLF) rate unchanged at 2.50% after cutting it in August - although they did increase the MLF issuance size to CNY591bn, providing an additional CNY191bn of liquidity.

Outlook

Beyond the liquidity benefits, the PBoC will anticipate the rate cut sending a strong dovish policy signal – boosting market confidence. The authorities will be increasingly hopeful that they can steady the housing market following a recent flurry of support measures for the property sector. The government’s increasingly apparent goal is to stabilize economy sufficiently, in order to achieve their economic growth target while not avoiding over stimulating growth or boosting leverage. However, investors remain uncertain on the longer-term efficacy of these measures – with opinion split if the PBoC will need to provide additional monetary policy support or it has reached the end of its interest rate cutting cycle.

For RMB cash investors, interest rates are expected to remain at current low levels for the foreseeable future. However, a diversified strategy across different investment options and tenors – including liquidity and ultra-short duration strategies – remains one of the high conviction options that present a relatively attractive return opportunities while balancing the needs for liquidity and security.

096t231509033301

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.