At their latest monetary policy meeting, the Reserve Bank of Australia (RBA) cut base rates and announced the introduction a traditional quantitative easing (QE) program “to support job creation and the recovery of the Australian economy from the pandemic”.

Widely signalled by the central bank ahead of the meeting, the announcement was in-line with market and our expectations. Still, this was by far the most wide-ranging monetary policy actions by the RBA – with significant implications for the AUD interest rates and investors.

A PACKAGE OF MEASURES

The RBA lowered its overnight cash rate, 3-year government bond yield curve control (YCC) target, and term funding facility rate from 0.25% to 0.1%. Interest paid on excess reserves (ES balances) is also reduced from 0.10% to 0.0%.

In addition, the bank introduced a traditional QE program. It is committed to buy from the secondary market a total of AUD 100bn of government and semi-government bonds with maturities of 5-10 years over the next 6-months. The purchase is likely around AUD 5bn per week in addition to other purchases under the YCC program, which currently totals approximately AUD 63bn.

Recent economic data has shown signs of improvement. With the Covid-19 pandemic under control and Victoria re-opening, the RBA believes “the economic recovery is under way”. The central bank raising economic forecasts and is predicting positive third quarter economic growth. However, with the pace of growth projected to be slow, additional action was still deemed necessary.

PIVOT TO EMPLOYMENT

The central bank reiterated that previous monetary policy measures (announced in March) improved market liquidity while reducing the cost of funding. The latest measures should further reduce the cost of funding, contribute to a lower exchange rate and support asset prices.

Most importantly, the new measures will complement the Federal Government’s fiscal support package to support jobs and growth. In its monetary policy statement, the RBA confirmed that jobs were an “important national priority”. The RBA solidified its dovish policy stance, promised to monitor the effectiveness of the QE program and committed to “do more if necessary”.

The RBA has firmly switched its focus from inflation to employment as the driver of monetary policy. Given employment is a lagging indicator of economic growth, it could be several years before Australia reaches full employment, which in turns triggers the next central bank rate hiking cycle.

IMPACTS OF QE

After the meeting, the RBA Governor Philip Lowe repeated the central bank’s reluctance to implement negative interest rates. With base rates already at their lower bound, this implies the QE program is not the central bank’s primary policy tool.

After completing the first stage of QE purchases in six months’ time, the RBA’s balance sheet will have tripled since the beginning of 2020 with the central bank holding approximately 15% of Australian government debt outstanding (in comparison, the Federal Reserve owns 20% of US government debt).

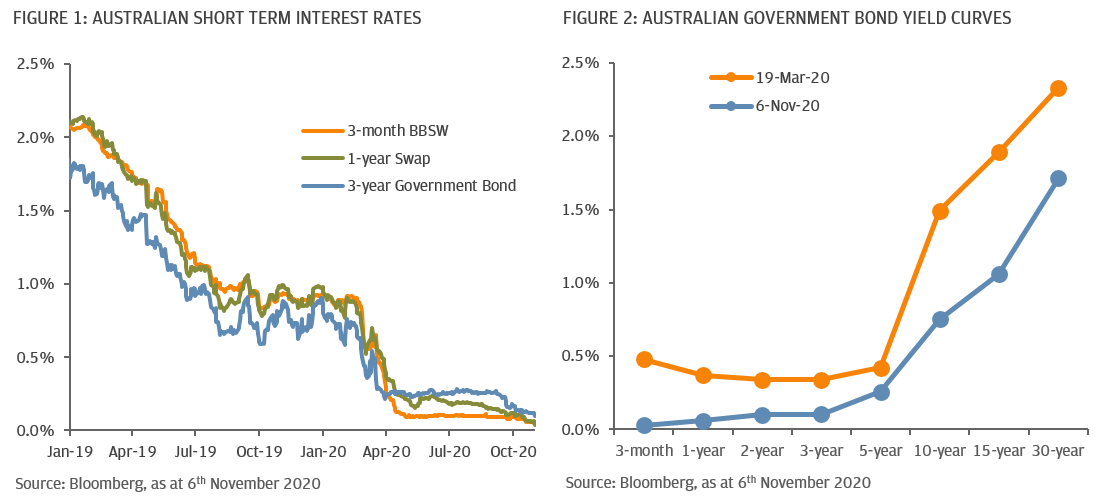

IMPACTS ON MARKET RATES

Short term rates had already priced in the rate cuts with 1- to 6- month BBSW yields falling over the past few weeks before hitting record lows of 0.02% to 0.03% (Fig 1) after the RBA announcement. Government bond yields have also declined with 3-year bond yielding 0.11%, close to the new YCC target; while the longer term curve has flattened (Fig 2). Finally, cash rates have fallen towards 0%, in line with the new interest rate on excess reserves.

Key indicators to monitor will include the USD/AUD FX rate and the USD/AUD 10-year government bond spread. The AUD has been one of the weakest performing majors over the past few weeks – during a period of US$ weakness. Although it was broadly unchanged following the RBA announcement, its future trend will depend on the actions of global central banks and future RBA QE decisions.

With Australian rates already at record lows, the actual benefit of these small, additional rate cuts is minimal. However, the RBA appears more focused on boosting confidence and ensuring monetary policy appears aligned with the very stimulatory fiscal measures announced in the latest Federal budget. Governor Lowe also wants to avoid lagging the dovish actions of other major central banks – which are fundamentally impacting traditional monetary policy and global interest rates.