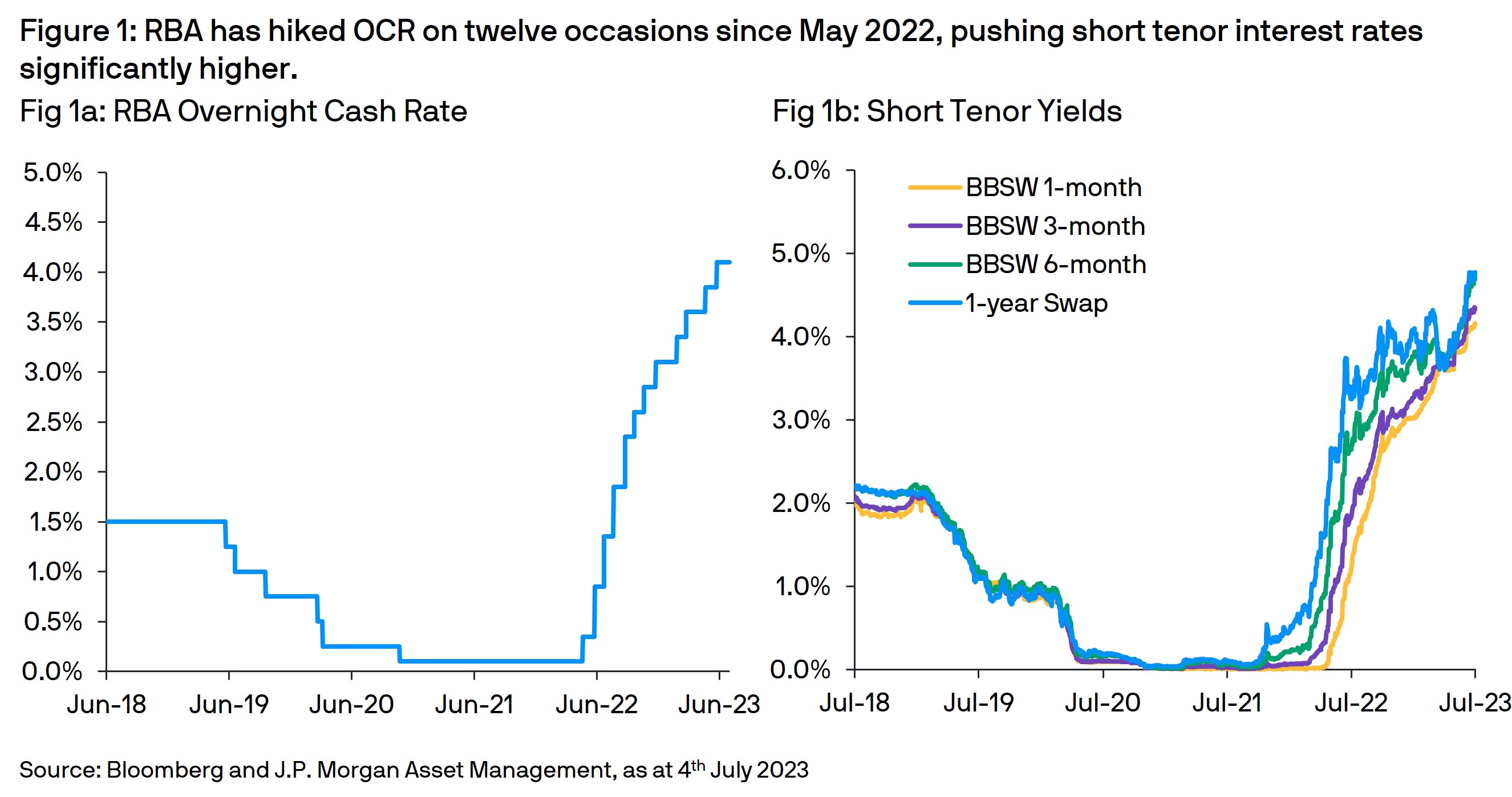

At its monetary policy meeting on the 4th of July, the Reserve Bank of Australia (RBA) left the overnight cash rate (OCR) unchanged at 4.10%. This represents the second pause in the central bank’s current hiking cycle, with the previous intermission this April followed by two subsequent hikes in May and June. While retaining a hawkish bias, the RBA justified its decision by noting that the OCR rate had already increased by 400bps since May 2022 and uncertainty had risen - therefore, a pause will allow more time to “assess the impact of the increase in interest rates to date and the economic outlook”.

Peak versus entrenched inflation

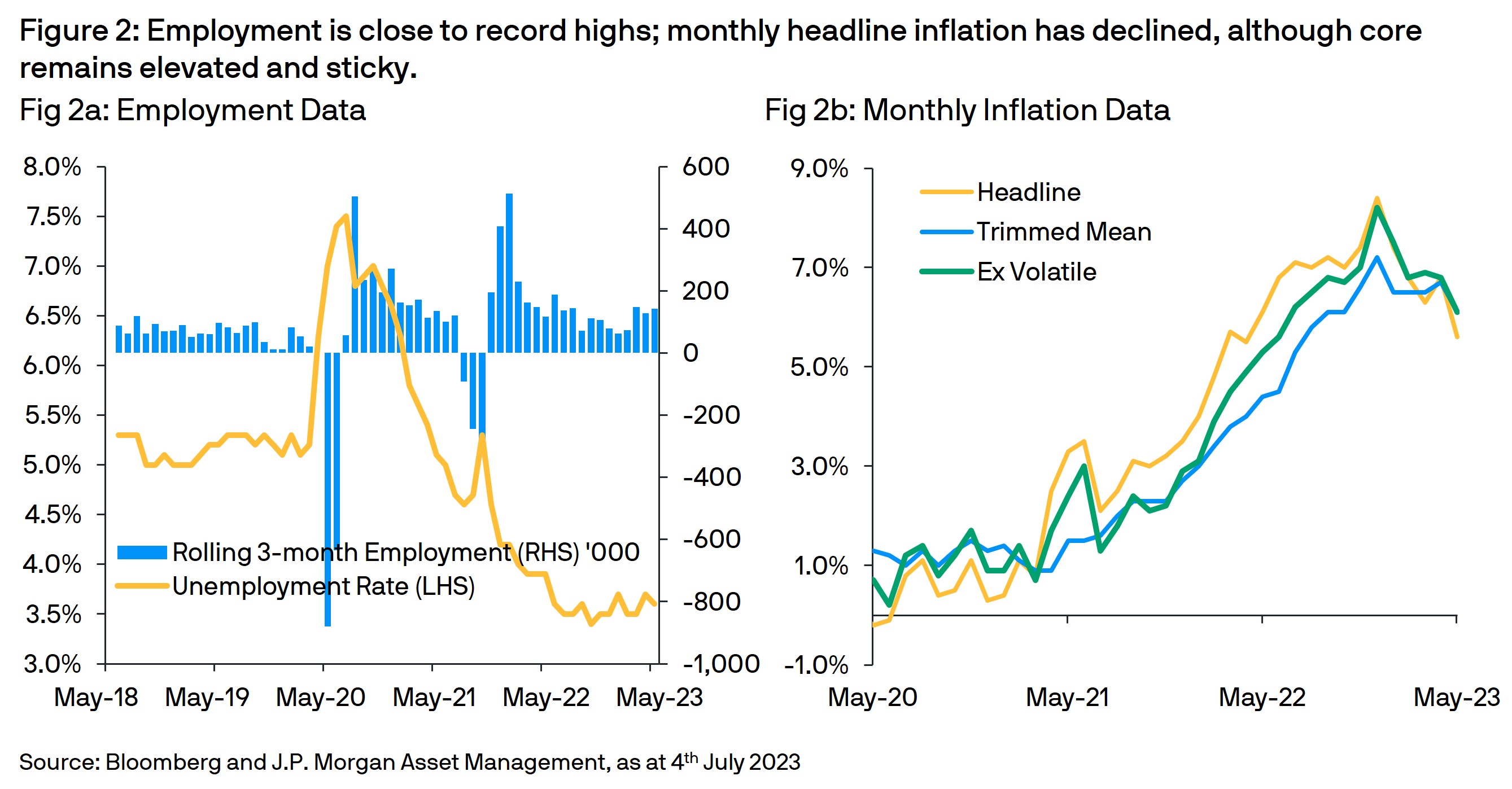

The RBA observed that “growth in the Australian economy has slowed”, with first quarter GDP moderating to 0.2%y/y as slower global growth and faltering Chinese demand weigh on exports, while higher interest rates and cost-of-living challenges impact domestic consumption. The central bank also suggests that “inflation has passed its peak”, with the latest monthly headline inflation recorded a welcome decline to 5.6%y/y (Fig 2b), the lowest reading in thirteen months and significantly lower than the December zenith of 8.4%y/y. The RBA believes these two factors demonstrate that “higher interest rates are working... and will continue to do so”, providing it confidence to hold interest rates steady.

Nevertheless, recent data has been stronger than expected with retail sales exhibiting surprising strength and the unemployment rate returning to a near 50-year low on strong employment hiring (Fig 2a). The property market has also recorded an unanticipated rebound; as construction, home loans and house prices all recover from their first quarter lows. Meanwhile, the monthly trimmed mean inflation number only slipped slightly to 6.1%y/y, while inflation excluding volatile items remains elevated at 6.5%y/y (Fig 2b). With both readings still elevated, the RBA acknowledged the risks of high inflation becoming “entrenched in people’s expectations”, which “would be very costly to reduce later”.

Market impact

The RBA’s decision to pause rates was not entirely unexpected with 14 out of 27 analysts polled by Bloomberg predicting a pause while markets were only pricing in approximately a 30% chance of a rate hike. Nevertheless, following the central bank’s decision, the currency did weaken slightly and bond yields declined modestly across the curve. However, markets continue to expect more rate hikes, with a 70% probability of of two additional rate increases priced in by December 2023.

Outlook:

The RBA remains optimistic that its monetary policy decisions will allow the economy to grow while also ensuring that inflation returns to the 2-3% target range within a reasonable period. Yet, it also acknowledges that “inflation is still too high and will remain so for some time yet” - exacerbating the risk “that expectations of ongoing high inflation will contribute to larger increases in both prices and wages”. Recognizing these dangers, the central bank affirmed its “determination to return inflation to target” and suggested that “some further tightening of monetary policy may be required”, dependent on future developments in the global economy, household spending, inflation, and labor market. We believe the next quarterly inflation report and Statement on Monetary Policy (due in late July and early August respectively) will be key to determining the trajectory of future rate hikes.

For AUD cash investors, the current high interest rates and upward sloping yield curve present relatively attractive investment opportunities for liquidity and reserve cash balances. However, high inflation, a hawkish central bank and a focus on data dependent decision-making suggest interest rates are likely to remain volatile, implying investors could consider pursing a cautious and diversified approach to cash investing.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

This information is generic in nature provided to illustrate macro trends based on current market conditions that are subject to change from time to time. This generic information does not take into account any investor’s specific circumstances or objectives and should not be construed as offer, research or investment advice.

09fm230407082931