In a recent session at the Global Liquidity Investment Forum, held in Singapore and Hong Kong, portfolio managers Kyongsoo Noh and Aidan Shevlin explored strategies for managing volatility in the global money market. In these uncertain economic times, understanding the Federal Reserve's monetary policy, the impact of global and domestic financial conditions on the Asia-Pacific (APAC) region, and strategic investment approaches for liquidity investors is crucial.

Navigating Global Economic Uncertainty

The U.S. economy is experiencing slower but still positive growth, while uncertainty and volatility have been magnified due to the government’s foreign and trade policy announcements. Fortunately, analyzing GDP components—consumption, government expenditures, investments, and net exports—provides a reliable framework for understanding economic conditions. The U.S. consumer sector remains solid, with low unemployment and moderate wage growth, while external factors like rebuilding investment following the recent wildfires in Los Angeles should positively impact the investment component of GDP.

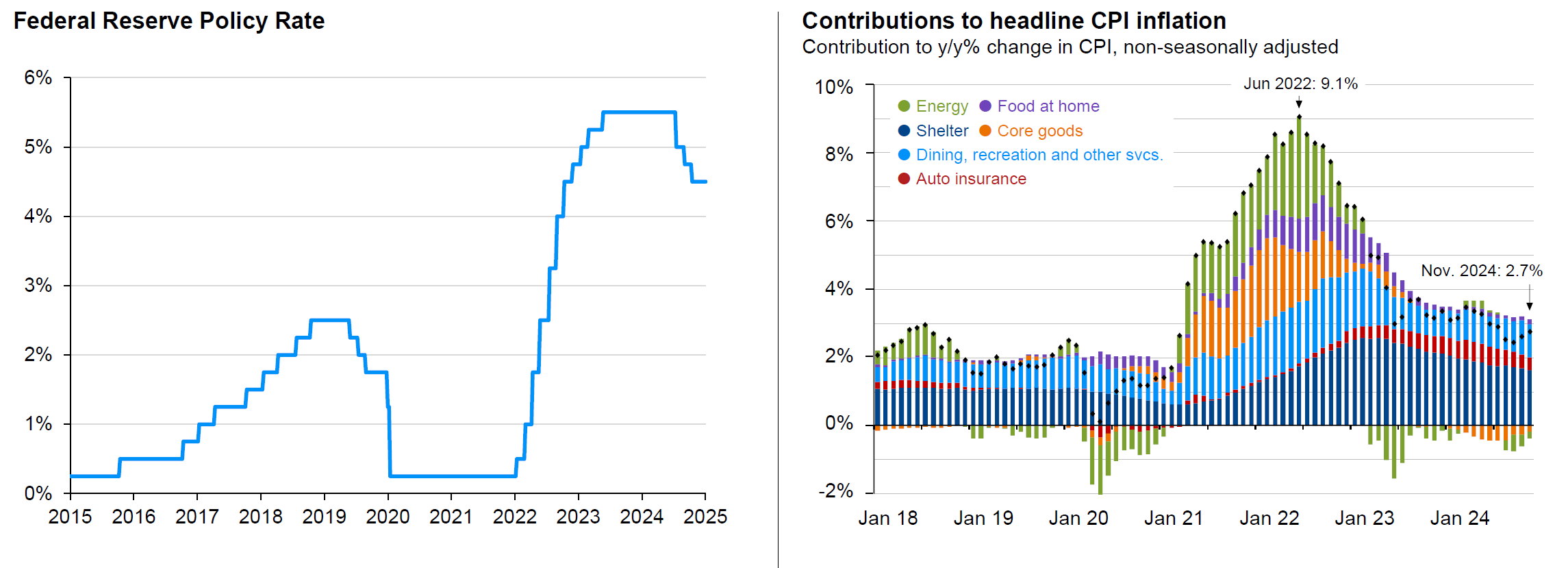

Conversely, government policy announcements require more careful interpretation. While tax cuts and deregulation are potential positives, their effects may not materialize until 2026. Meanwhile, policies like government expenditure cuts, immigration restrictions, and tariffs could pose growth headwinds. It is believed that the net impact of these factors could potentially reduce U.S. GDP growth to around 1.5% for the year, while the impact of tariffs may increase U.S. inflation to around 3% for 20251. Given the Federal Reserve's (Fed) dual focus on maintaining maximum employment and stable prices, rates are expected to remain unchanged in the near term to ensure inflation is contained.

”The Fed may resume its rate cutting trajectory, potentially reducing rates by one or two times, in the second half of 2025 to support growth.” – Kyongsoo Noh

Fig 1: Federal Reserve has paused following 100bps of rate cuts due to slowing progress on returning inflation to target.

(LHS) Source: Bloomberg: data as of 12 March 2025. (RHS) Source: BLS, FactSet, J.P. Morgan Asset Management. Contributions mirror the BLS methodology on Table 7 of the CPI report. Values may not sum to headline CPI figures due to rounding and underlying calculations. “Shelter” includes owners’ equivalent rent, rent of primary residence and home insurance. “Food at home” includes alcoholic beverages. Guide to the Markets – U.S. Data are as of December 31, 2024.

Divergent Monetary Policies in APAC

APAC economic growth has slowed, as robust exports were offset by restrictive monetary policies and softer domestic demand. Fortunately, inflation began declining in 2024, a trend expected to continue into 2025, easing cost-of-living pressures and supporting domestic consumption.

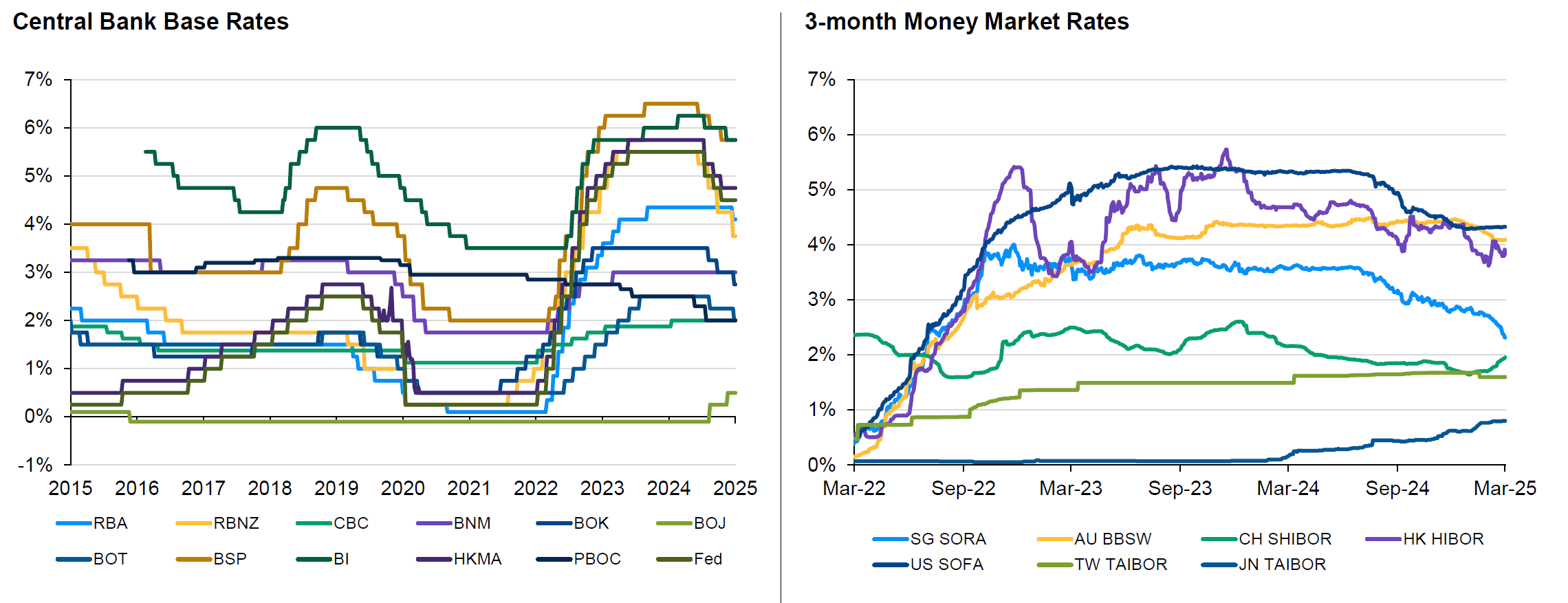

Historically, APAC central banks have tended to follow the Fed's lead. Since regional base rates peaked last summer and the Fed began its cutting cycle in September 2024, several APAC central banks have followed suit by reducing interest rates. However, not all central banks have done so.

Two distinct trends are now emerging. In markets like New Zealand, Korea, and Singapore, rapid inflation declines and economic growth threats from volatile trade policies have prompted accelerated rate cuts as central banks shift their focus from curbing inflation to supporting growth. Conversely, in Australia, Indonesia, Taiwan and Malaysia, central banks remain cautious, opting for a gradual approach to rate cuts due to persistent inflation concerns and robust demand.

Meanwhile, Japan and China present unique cases. The Bank of Japan has raised interest rates to an 18-year high, driven by improved economic growth and rising inflation. Meanwhile, the People's Bank of China has pivoted to a dovish stance but refrained from cutting rates, focusing instead on currency stability amidst slower economic growth and escalating trade tensions.

Fig 2: APAC central banks have started cutting rates, market yields have declined in anticipation of additional rate cuts.

Source: Bloomberg, data as at 12 March 2025

Reserve Bank of Australia (RBA), Reserve Bank of New Zealand (RBNZ), Central Bank of the Republic of China (CBC), Bank Negara Malaysia (BNM), Bank of Korea (BOK), Bank of Japan (BoJ), Bank of Thailand (BOT), Bangko Sentral ng Pilipinas (BSP), Bank Indonesia (BI), Hong Kong Monetary Authority (HKMA), People’s Bank of China (PBOC), Federal Reserve (Fed); Singapore (SG), Australia (AU), China (CH), Hong Kong (HK), United States (US), Taiwan (TW), Japan (JP)

As we navigate through 2025, APAC central banks face complex domestic and international dynamics. Slower growth, moderating inflation and escalating trade tensions suggest many central banks may reduce base rates more swiftly than anticipated to promote growth. High real rates provide room for supportive cuts, and recent actions have enhanced their credibility, giving them the ability and confidence to cut if necessary.

”Lingering inflation concerns and worries about currency weakness and capital flight may prevent rapid policy changes.” – Aidan Shevlin

Conclusion: Balancing Yield and Risk in Uncertain Times

It is believed that future central bank actions will lean towards rate cuts as global economic growth slows and inflation moderates. However, interest rates are expected to remain elevated by recent standards, with the Fed's cutting cycle likely to be shallow and APAC central banks cutting gradually.

The implications of these potential central bank actions on interest rates are significant. In an environment of high policy uncertainty and volatility, strategies offering higher carry and lower volatility become relatively attractive. The front end of the yield curves, with their high yields and lower duration, provides an excellent balance between yield and risk, making them an appealing option for investors. Reducing exposure to more volatile segments, such as longer-duration bonds and lower-rated securities, may also help mitigate risk.

Strategically positioning portfolios and opportunistically extending duration would allow investors to navigate policy uncertainty, while capitalizing on higher yield opportunity while minimizing exposure to volatility. By focusing on their core investment principles of liquidity, security and yield, investors can continue to navigate the uncertainties of 2025 with confidence.