In brief:

- The recent, aggressive Fed interest rate tightening policy, combined with Hong Kong’s weak economic outlook, moribund Chinese growth and subdued local market sentiment, has pushed the HKD towards the weak side of its convertibility. The HIBOR-LIBOR spread has also widened the most since 2019.

- The magnitude of HKMA’s recent interventions has been unprecedented, buying HKD213bn (USD27bn) in the past three months alone. This is partly due to the Aggregate Balance hitting a record high before this hiking cycle and a weak local economy.

- The HKD is likely to continue trading on the weak side of its convertibility. This suggests more intervention could be needed, which will further reduce the Aggregate Balance, potentially triggering a spike in the HIBOR rates and normalizing the HIBOR-LIBOR spread.

The recent, aggressive Federal Reserve (Fed) interest rate tightening policy, combined with Hong Kong’s weak economic outlook, moribund Chinese growth and subdued local market sentiment, has pushed the HKD towards the weak side of convertibility. The currency has remained close to HKD7.85 versus the USD for the past four months despite record intervention by the Hong Kong Monetary Authority (HKMA) to defend Hong Kong’s Linked Exchange Rate System (LERS). The current, wide HIBOR-LIBOR spread and still ample local HKD market liquidity continue to weigh on the currency, which has significant implications for HKD investors.

Aggressive Fed, rapid hikes:

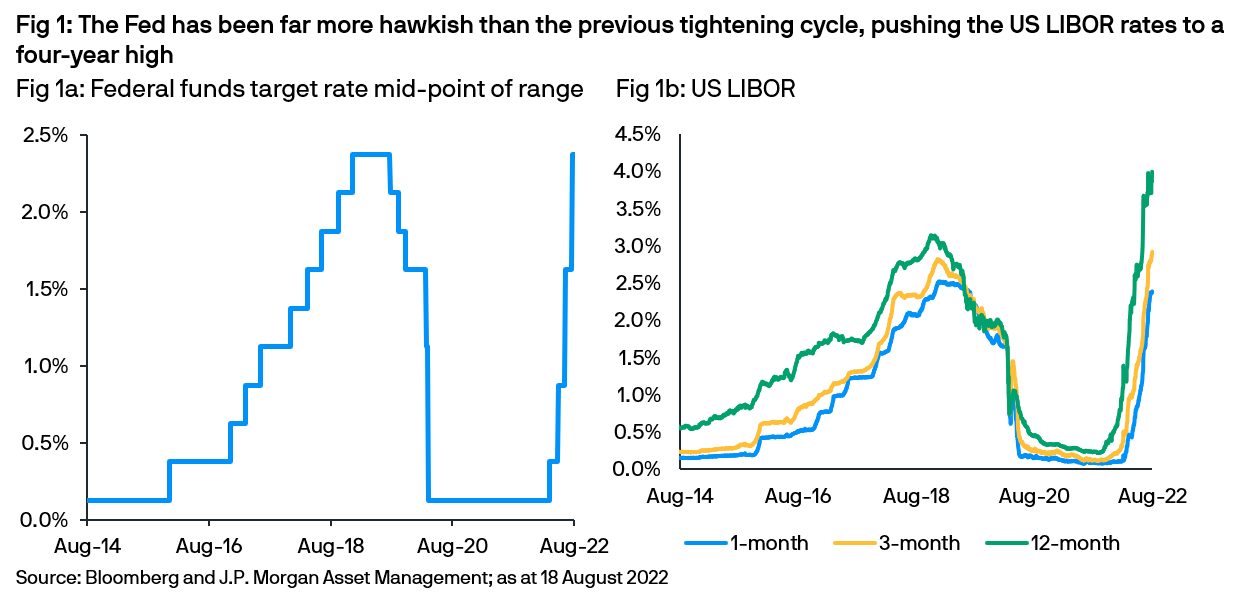

In its previous tightening cycle, the Fed hiked rates by a total of 225bps leisurely over nine meetings spanning a period of three years. In contrast, this year alone, the Fed has achieved the same result in merely five months. Meanwhile, the market expects additional rate hikes into early 2023, highlighting the Fed’s hawkish stance as it seeks to regain its inflation fighting credentials (Fig 1a).

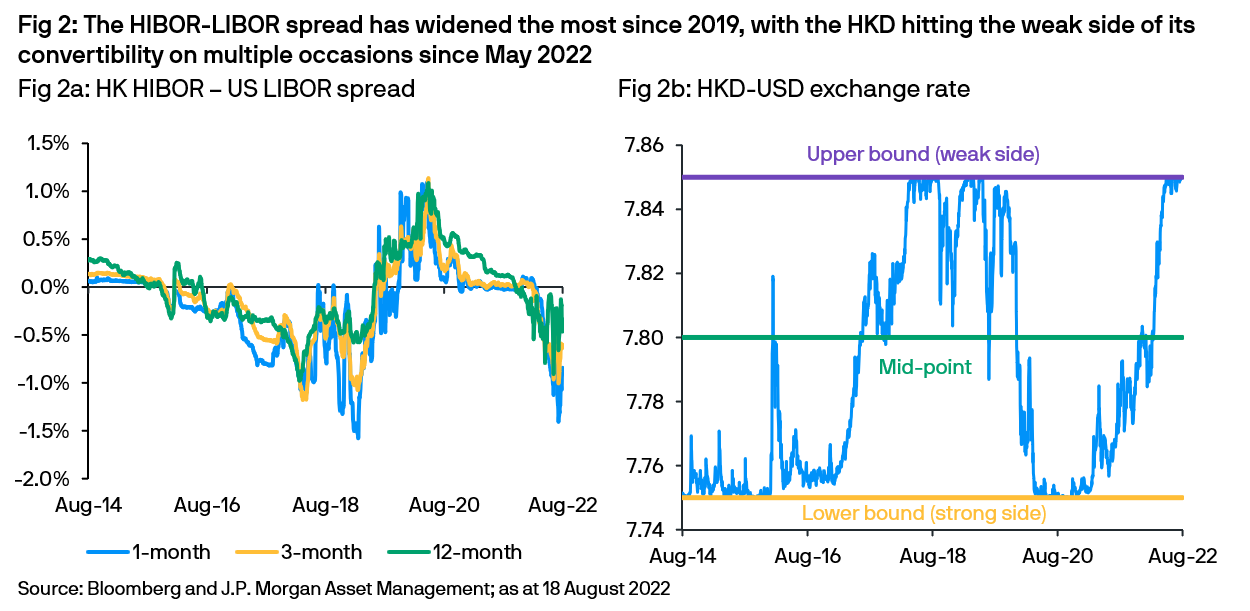

The rapid rate hikes and the expectations of further tightening has pushed US LIBOR rates to a multi-year high (Fig 1b), while sharply steepening the curve. Contrarily, HK HIBOR rates have lagged behind due to ample liquidity in the local banking system. The HKMA’s Aggregate Balance, where commercial banks keep their clearing balances with the HKMA, increased to a historical high of HKD457bn in 2020. The increase was due to significant capital inflows caused by strong demand for Chinese assets, blockbuster local initial public offerings and a dovish Fed. With HKD liquidity remained abundant at the start of 2022 as the Fed pivoted to a hawkish monetary policy stance, the HIBOR-LIBOR spread widened to a three-year high (Fig 2a).

The existing elevated interest rate differential has also incentivized arbitrage trades – where investors borrow HKD at lower rates and invest in USD to earn higher US rates – weakening the local currency. Together with the Fed’s commitment to expedite reduction of their balance sheet, the trade-weighted USD index has jumped to a 20-year high. This has further weakened the HKD as market participants naturally pivoted into USD by selling HKD, ultimately driving the HKD to hit the weak side of its convertibility in May 2022 (Fig 2b).

HKMA’s interventions:

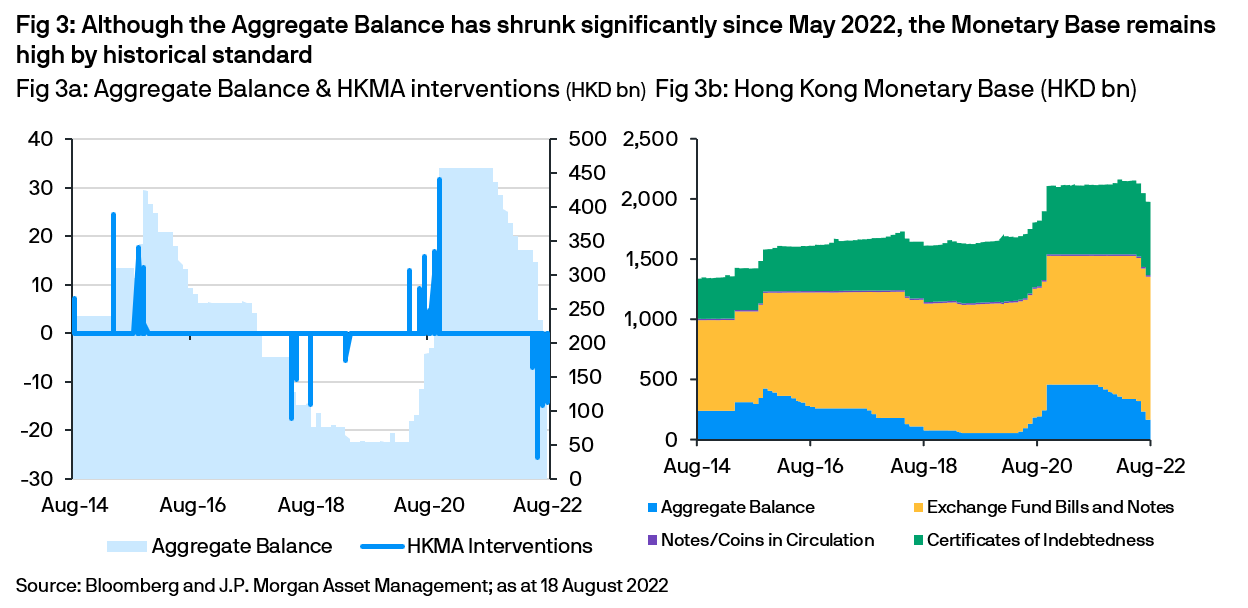

As the HKD hit the weak side of its trading band, the HKMA automatically intervened to defend the LERS, selling USD and buying HKD to manage downside risks of the 39-year old peg. The magnitude of recent purchases has been unprecedented. The HKMA bought HKD213bn (USD27bn) in the past three months, compared to HKD126bn (USD16bn) only during the previous period of HKD weakness between March 2018 to December 2019 (Fig 3a).

The rationale behind such astronomical purchases is partly due to the lower issuance of Exchange Fund Bills and Notes by the HKMA (Fig 3b), which were used to soak up excess liquidity in the interbank market historically. Lacking this liquidity sterilization, the Aggregate Balance hit at a record high before this hiking cycle. Also, the local economy is in a much weaker position – battered by stringent Covid lockdown measures, a deteriorating external outlook and a muted Chinese recovery – all contributing to capital outflow momentum. The Hong Kong government has revised down its full year 2022 GDP forecast twice in the past three months, with Hong Kong’ economy potentially contracting for the third time in a row since 2019.

Implications to HKD investors:

Under such volatile markets, we believe the HKD peg is the high conviction solution for Hong Kong, while the HKMA’s massive foreign exchange reserves cover over 100% of the Monetary Base, lending credibility to its commitment to defend the LERS. Nevertheless, the HKD is likely to continue trading on the weak side of its convertibility despite extraordinary interventions by the HKMA. This suggests more intervention could be needed, which will further reduce the Aggregate Balance, potentially triggering a spike in the HIBOR rates and normalizing the HIBOR-LIBOR spread.

As local rates continue to edge higher, we believe HKD cash investors should remain nimble and diversify across tenor to reduce capital loss opportunities. Meanwhile the volatility of the local currency is poised to persist in the short- to medium- term.

Diversification does not guarantee positive returns or eliminate risk of loss.