Underpinned by the Linked Exchange Rate System (LERS), Hong Kong’s interbank offered rate (HIBOR) has largely shadowed its US counterpart (LIBOR). However, escalating political and trade tensions, strong international demand for HKD and increasing connection with China, have weakened this historic and apparently immutable connection – with significant implications for HKD cash investors.

AN IMPORTANT SYSTEM

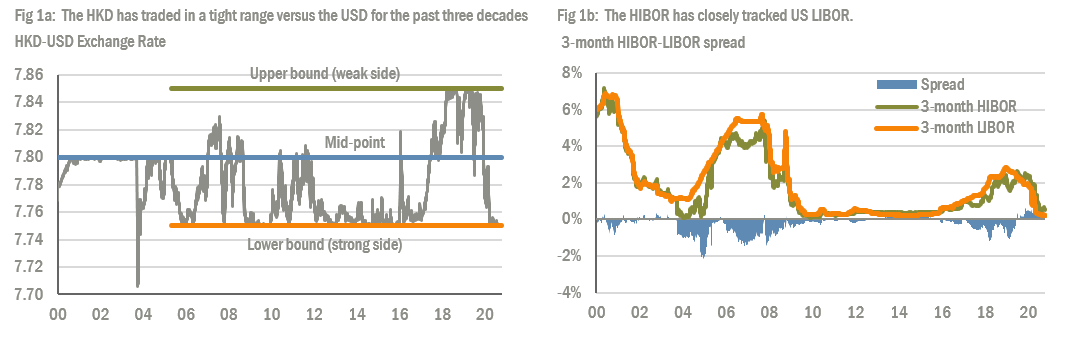

The LERS was designed to end a period of foreign exchange volatility by pegging HKD to USD. Its “convertibility zone” allows HKD to float freely between the upper and lower bound at HKD7.85 and HKD7.75 respectively (Fig 1a).

Under this regime, the Hong Kong Monetary Authority (HKMA) is committed to buy HKD (versus USD) whenever excess capital outflows push the exchange rate to its upper (weak side) bound and vice versa. These interventions will trigger an increase or decrease in the Aggregate Balance, which in turn pushes local interest rates lower or higher.

This mechanism negates the need for frequent HKMA intervention. Any HKD movement from the mid-point of the trading range will trigger an automatic stabilization mechanism with HIBOR diverging from USD LIBOR (Fig 1b), creating an interest rate arbitrage opportunity. Backed by substantial HKMA reserves, the peg has successfully weathered several financial crises and continues to guarantee the city’s financial stability.

Source: Bloomberg and J.P. Morgan Asset Management, as at 22nd October 2020

FUNDAMENTAL VERSUS TECHNICAL

With Hong Kong suffering from its worst ever recession – due to global trade tensions, domestic protests and Covid-19 outbreak – fundamentals would imply the HKD should be trading on the weak side of convertibility. However, a number of technical factors have propelled the currency to the strong side of convertibility.

1. The arbitrage opportunity

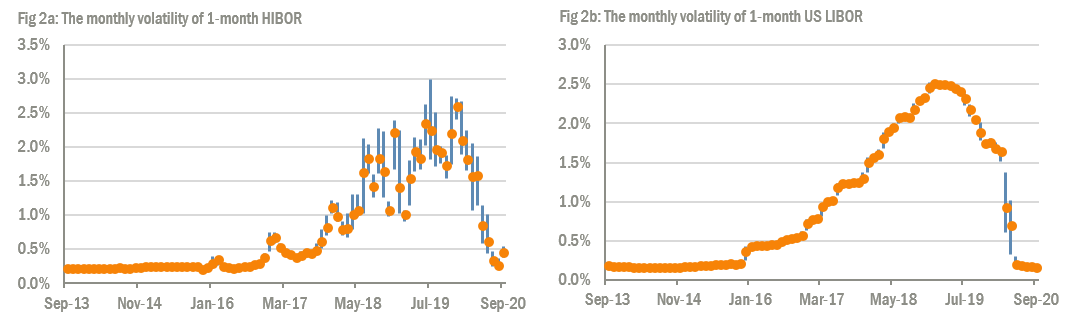

Since the Fed started to raise interest rates in 2016, HIBOR’s movements (Fig 2a) has been much more volatile than US LIBOR (Fig 2b). The HKMA was slower to replicate the Fed’s rapid rate hikes in 2017-18 and subsequent cuts in 2019-20. By early 2020, this helped push the HIBOR-LIBOR spread to a 20-year high, encouraging capital inflows. While the yield differential has subsequently declined, borrowing in USD to buy HKD remains profitable given the ultra-low interest rate environment in the US.

Source: Bloomberg and J.P. Morgan Asset Management, as at 22nd October 2020

2. The IPO hub

The volume of primary and secondary equity listings in Hong Kong has increased dramatically in recent years. Less onerous regulations and access to USD make Hong Kong remains attractive for onshore Chinese firms to access international capital markets. Meanwhile, many Chinese companies listed in the US via American Depositary Receipt are now seeking secondary listings in Hong Kong, due to their increasing likelihood of being delisted from the US exchanges.

3. The stock-link influence

The launch of the Shanghai and Shenzhen Stock Connect in 2014 and 2016, was a transformational development for China’s capital market. It deepens the integration between Hong Kong and mainland the stock markets, while further integrating China’s financial markets with the global financial system. International investors can now readily access the combined USD4.9bn market capitalization of Shanghai and Shenzhen via Hong Kong’s northbound trading link.

4. The China impact

Historically, Hong Kong’s economic cycle was closely aligned to the US and international markets – highlighting the benefits of the USD peg and closely correlated interest rates. With the growing importance of China, key drivers of the city’s growth have become more closely linked with the mainland. Ongoing RMB internationalization, combined with the benefits of Hong Kong’s financial and legal systems under the “one country – two systems” policy, have strengthened these connections and Hong Kong’s role as the gateway to China.

These factors have also provoked a significant increase in the volatility of HIBOR. They have partially negated the currency’s automatic interest rate stabilization mechanism, magnified interest rate uncertainty and generated unexpected bond price movements.

THE RECALCITRANT HKMA

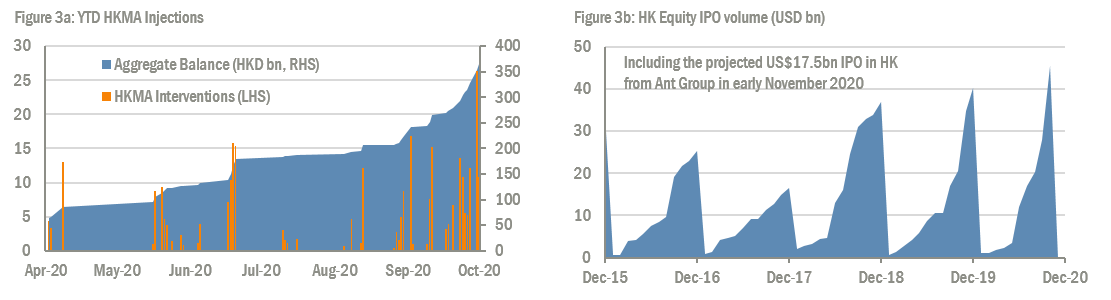

With the HKD firmly affixed to the strong side of convertibility, the previously recalcitrant HKMA has had to intervene in the foreign exchange markets on a record 73 occasions (Fig 3a), selling over HKD298bn (USD39bn) – the largest ever annual intervention – to protect the LERS. This has driven the Aggregate Balance to the highest level since January 2016 at HKD373bn (Fig 3b). With several additional mega-IPOs expected to list over the coming months, demand for HKD is expected to remain very strong – necessitating further HKMA intervention.

Source: Bloomberg and J.P. Morgan Asset Management, as at 22nd October 2020

CONCLUSION

As the technical factors rapidly pivot into longer term fundamental drivers of the HKD, the currency is likely to adhere to the strong side of the convertibility. While this is positive for HKD’s strength and stability, HIBOR has experienced increasing volatility due to the negative impact of large ebbs and flows of liquidity on the city’s small, local banking system. HKD cash investors will have to be increasingly vigilant – to the adverse consequences for bond prices and also the positive opportunities to lock in higher yields.