ECB raises rates once more, but future decisions look finely balanced

01/08/2023

Ian Crossman

In brief:

- At its monetary policy meeting on 27 July 2023, the European Central Bank (ECB) tightened monetary policy further, increasing key interest rates by 25 basis points (bps).

- The ECB moved away from an explicit hiking bias but left the door open to future rate increases, with ECB president Christine Lagarde commenting in the press conference that the September meeting could result in a pause or a hike.

- The ECB also announced that the remuneration of bank minimum reserves would be cut to zero.

ECB continues to tighten, but the outlook remains uncertain

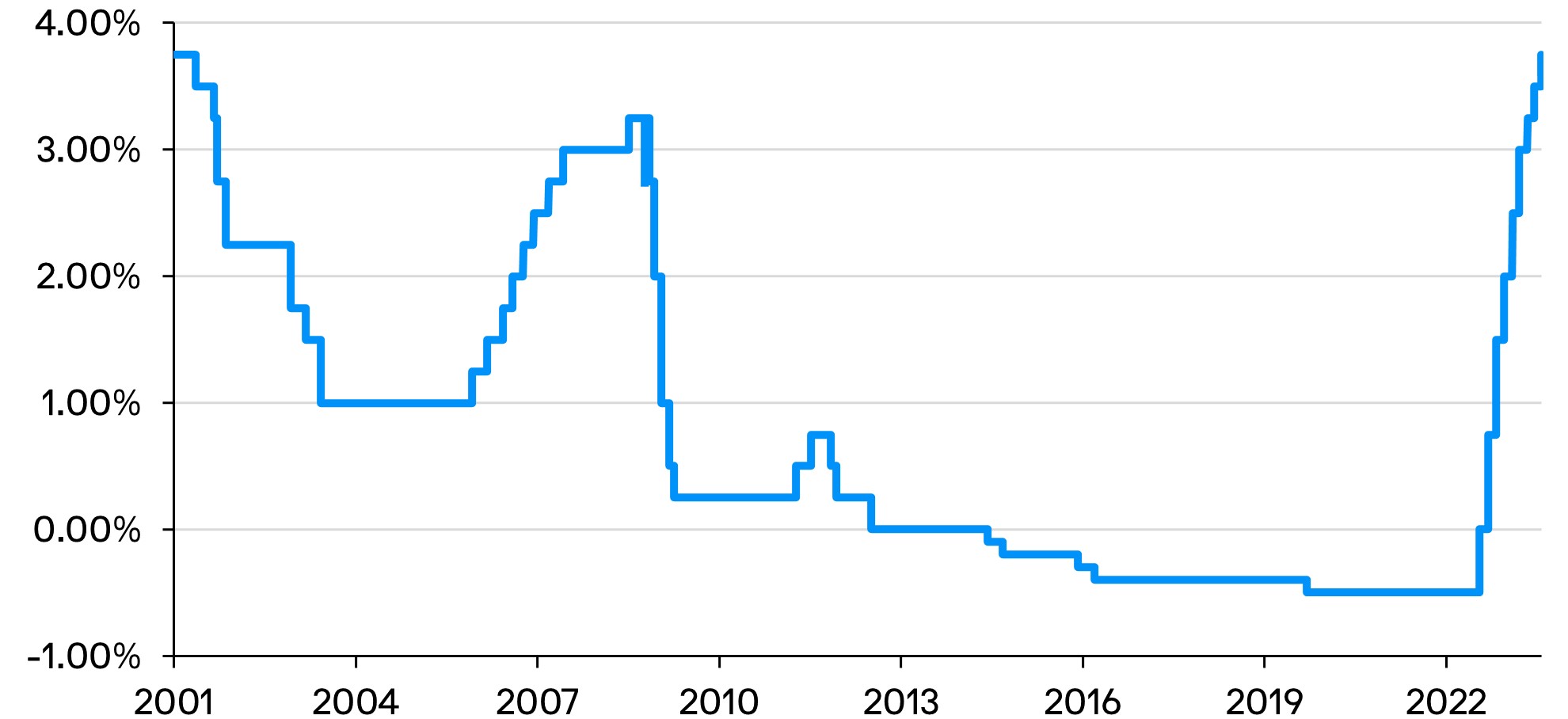

At the conclusion of its July 2023 monetary policy meeting, the ECB increased all three key interest rates by 25bps, bringing the refinancing rate to 4.25%, the marginal lending facility to 4.50% and the deposit facility rate to 3.75%. The increases were in line with market expectations and represent the ninth hike in the current cycle, taking cumulative rate hikes to 425bps since July 2022.

Exhibit 1: The ECB deposit rate equals its all-time high of 3.75%, last seen in Q1 2001

Source: Bloomberg, data as of 27 July 2023.

While progress has been made on inflation, ECB president Lagarde cautioned against declaring victory prematurely, repeating that inflation is “still expected to remain too high for too long” and that “underlying inflation remains high overall”. There was acknowledgment that prior rate increases are being passed through to the economy, which is a necessary factor to bring inflation back to target.

ECB to remain data dependent

ECB meetings will have a short summer recess and return towards the end of September. The interim period will see the release of two sets of inflation data and the final GDP figures for the second quarter of 2023, which will help inform the ECB Governing Council’s decision making, alongside the next round of quarterly growth and inflation forecasts. President Lagarde repeatedly mentioned during the press conference that the options between a further hike and a pause were finely balanced but did firmly rule out the prospect of a rate cut.

Credit conditions continue to tighten

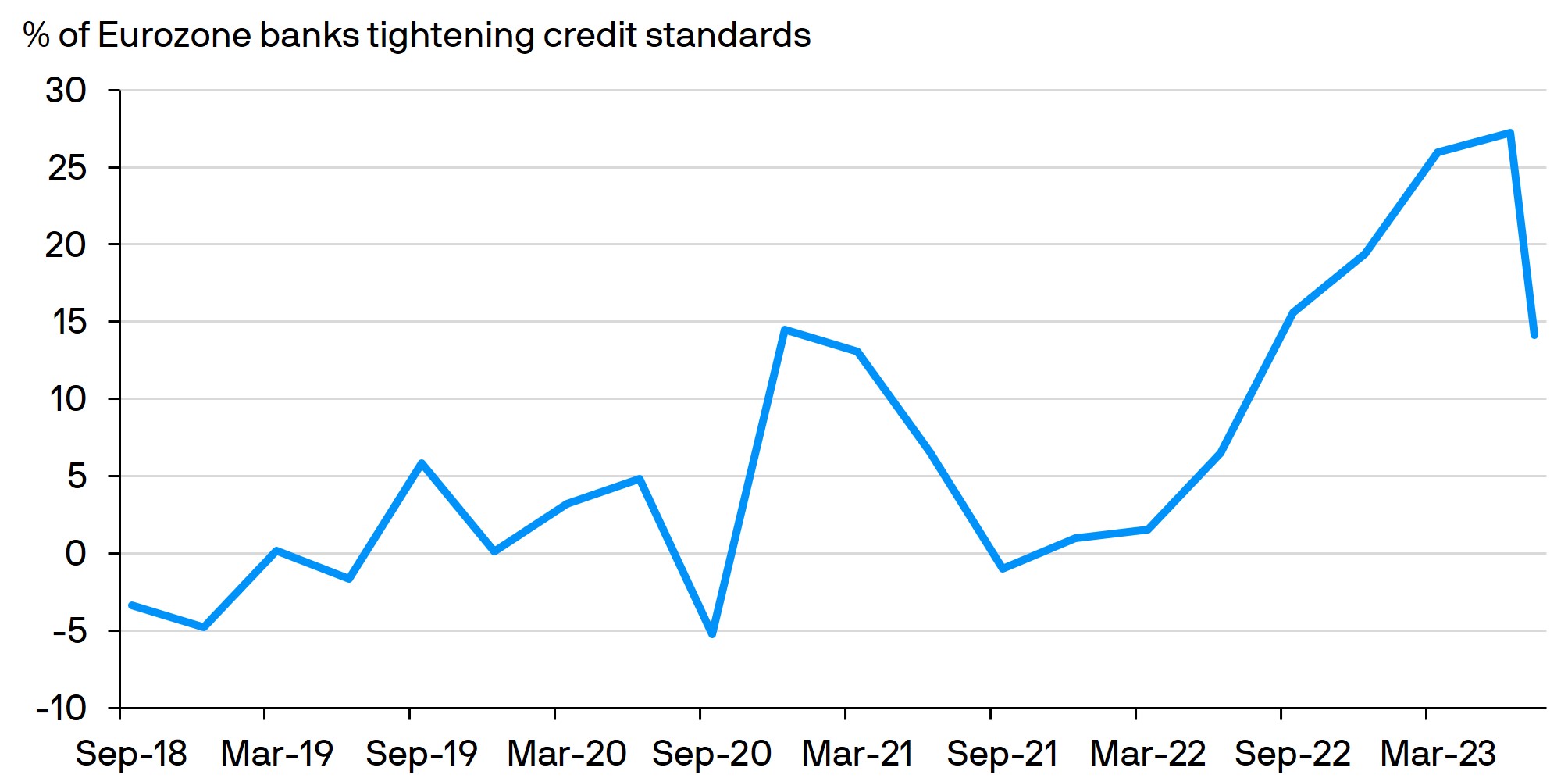

Earlier in the week, the ECB released its latest bank lending survey, which revealed a further tightening of credit standards for both consumers and business alike. Banks reduced property-related lending by 8% and general consumer lending by 18%, as higher policy rates deterred borrowers. A further moderate drop is expected in the third quarter, resulting in three consecutive quarters of tightened credit conditions. These developments, combined with the recent deterioration in forward-looking purchasing managers’ indices, raise question marks about the future trajectory for growth and could weigh against the need for further rate increases.

Exhibit 2: Eurozone banks report tighter credit conditions

Source: Bloomberg; data as of 28 July 2023.

ECB cuts remuneration of bank minimum reserves to zero

The remuneration paid to banks for their minimum reserves, which is currently in line with the deposit facility, will be cut to zero from 20 September. This is the second such reduction, with the remuneration having previously been reduced from the main refinancing operations rate in October 2022. The reductions aim to preserve the effectiveness of monetary policy and aid the full pass-through of interest rate decisions to money markets. The remuneration paid for excess reserves currently remains unchanged.

Implications for euro cash investors

The latest rate increase is good news for cash investors. J.P. Morgan Asset Management’s euro liquidity strategies are well positioned to benefit from higher rates, given the high levels of short-dated cash they carry. Deposit and repo rates should refix higher at the start of the new reserve period on 2 August, providing an initial boost to the strategies yield and increasing thereafter, due to the floating rate instruments held by the strategies. Higher reinvestment yields for term securities will also benefit the euro strategies over the coming weeks.

Conclusion

The outcome of the July ECB meeting was largely as expected. With the Governing Council now having a seven week recess before its next meeting, the market will be ever watchful on the key data releases to assess the likelihood of yet another rate hike, or a much anticipated pause by the ECB. The data dependency of the ECB remains key as the central bank weighs future data against the impact of previous monetary policy decisions that are yet to feed through to the wider economy. In this environment, we believe investors will be well served by our active approach to cash management that prioritises diversification and liquidity.

09me233107023028

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

NOT FOR RETAIL DISTRIBUTION: This communication has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yield are not a reliable indicator of current and future results. J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies at https://am.jpmorgan.com/global/privacy. This communication is issued by the following entities: In the United States, by J.P. Morgan Investment Management Inc. or J.P. Morgan Alternative Asset Management, Inc., both regulated by the Securities and Exchange Commission; in Latin America, for intended recipients’ use only, by local J.P. Morgan entities, as the case may be; in Canada, for institutional clients’ use only, by JPMorgan Asset Management (Canada) Inc., which is a registered Portfolio Manager and Exempt Market Dealer in all Canadian provinces and territories except the Yukon and is also registered as an Investment Fund Manager in British Columbia, Ontario, Quebec and Newfoundland and Labrador. In the United Kingdom, by JPMorgan Asset Management (UK) Limited, which is authorized and regulated by the Financial Conduct Authority; in other European jurisdictions, by JPMorgan Asset Management (Europe) S.à r.l. In Asia Pacific (“APAC”), by the following issuing entities and in the respective jurisdictions in which they are primarily regulated: JPMorgan Asset Management (Asia Pacific) Limited, or JPMorgan Funds (Asia) Limited, or JPMorgan Asset Management Real Assets (Asia) Limited, each of which is regulated by the Securities and Futures Commission of Hong Kong; JPMorgan Asset Management (Singapore) Limited (Co. Reg. No. 197601586K), this advertisement or publication has not been reviewed by the Monetary Authority of Singapore; JPMorgan Asset Management (Taiwan) Limited; JPMorgan Asset Management (Japan) Limited, which is a member of the Investment Trusts Association, Japan, the Japan Investment Advisers Association, Type II Financial Instruments Firms Association and the Japan Securities Dealers Association and is regulated by the Financial Services Agency (registration number “Kanto Local Finance Bureau (Financial Instruments Firm) No. 330”); in Australia, to wholesale clients only as defined in section 761A and 761G of the Corporations Act 2001 (Commonwealth), by JPMorgan Asset Management (Australia) Limited ABN 55143832080) (AFSL 376919). For U.S. only: If you are a person with a disability and need additional support in viewing the material, please call us at 1-800-343-1113 for assistance. Copyright 2023 JPMorgan Chase & Co. All rights reserved.